|

Related Topics |

|

We take a look at the latest update from Exxaro before they enter their closing period before reporting financial results, and it seems weaker demand at ESKOM will affect their coal production numbers

|

|

About Exxaro (EXX)

In November 2006, Kumba Resources Limited unbundled and Kumba’s coal and other assets merged with Eyesizwe Coal to create Exxaro Resources Limited. We have since grown to become one of the largest and foremost black-empowered coal and heavy mineral companies in South Africa, with other business interests around the world in Europe, the United States of America, and Australia. Our asset portfolio includes coal operations and investments in iron ore, pigment manufacturing, renewable energy (wind), and residual base metals.

In the last decade, Exxaro has established itself as an organisation that is respected by its peers for its innovation, ethics, and integrity. We’ve achieved this by acknowledging that we exist in a greater context. We are here to power better lives today and tomorrow, in South Africa and beyond.

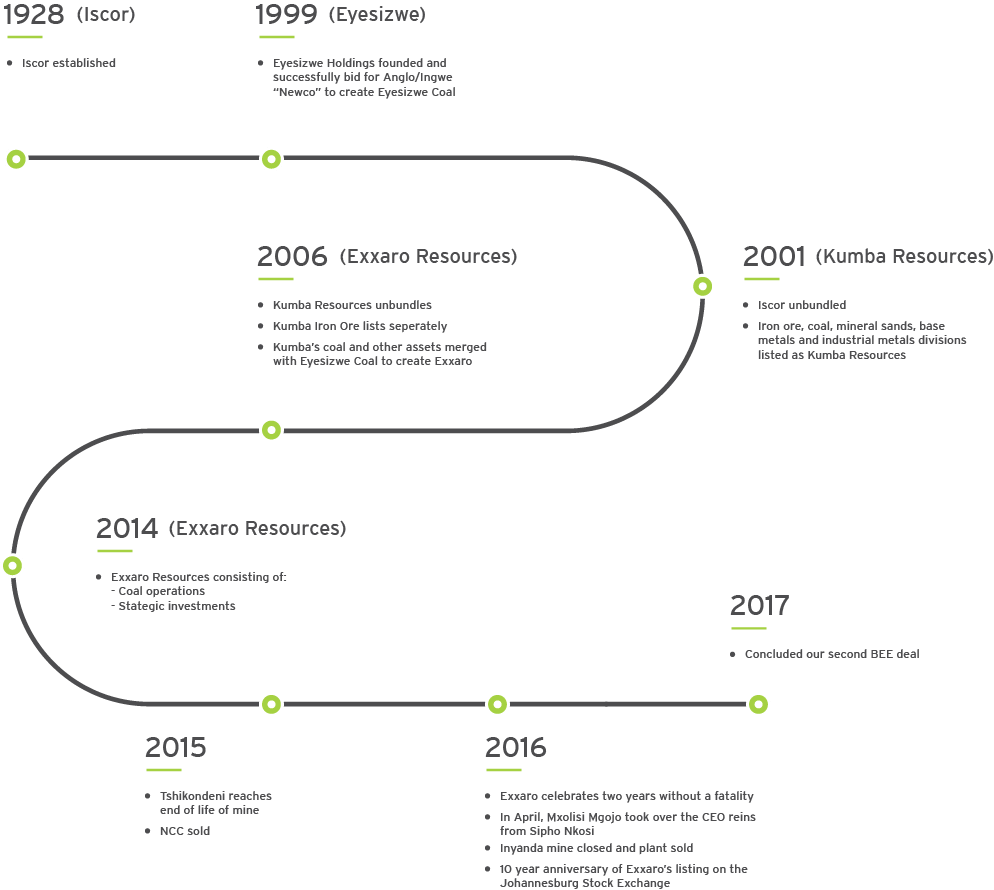

The image below shows the evolution and current company profile of Exxaro Resources

In the last decade, Exxaro has established itself as an organisation that is respected by its peers for its innovation, ethics, and integrity. We’ve achieved this by acknowledging that we exist in a greater context. We are here to power better lives today and tomorrow, in South Africa and beyond.

The image below shows the evolution and current company profile of Exxaro Resources

The evolution of Exxaro

Pre closing period update from Exxaro finance director

Dear stakeholder,

This is an overview of the group’s expected business performance for the period, encompassing strategic, operational and financial information. Unless otherwise indicated, all comparisons are against the six-month period ended 31 December 2018 (2H18). Zero Harm remains Exxaro’s key business objective. In the period we maintained a year-to-date lost-time injury frequency rate (LTIFR) of 0.12 (FY18: 0.12), still above our target of 0.11. We have done better in previous years and remain confident that we will improve on this through ongoing safety initiatives. We are pleased to report zero (0) fatalities for a period of 27 consecutive months as at 31 May 2019 and zero (0) “High Potential Incidents” (HPI’s) so far during 1H19 (1H18: 5HPI’s). Towards the end of 1H19 the US-China trade tension continued to escalate and weighed on global market sentiment. Commodity markets recorded mixed results over the period under review. In respect of Exxaro’s key commodities for 1H19, the API4 coal export price index is expected to average US$75 (2H18: US$99) per tonne, free on board (FOB), and the iron ore fines price US$90 (2H18: US$69) per dry metric tonne, cost and freight (CFR) China.

Total coal production volumes are expected to decrease by 5% (excluding buy-ins), mainly driven by reduced demand from Eskom at Medupi power station, directly resulting in 4% lower coal sales volumes. Commercially, the impact of the reduced Medupi volumes is mitigated due to the contractual agreement in place. While we expect to achieve higher export volumes, it is reasonable to assume that a weaker US$ sales price per tonne will be realised, in line with the weaker API4 coal export price index, cushioned somewhat by a weaker rand/dollar exchange rate. We are pleased with the outcome of our capital allocation programme and will maintain a disciplined approach, particularly in delivering on the sustaining and growth capex programmes while maintaining a strong balance sheet. We are aware that many of our contractors are experiencing financial difficulties and are intensifying engagement with these contractors to minimise any impact on completing our projects.

Coal capital expenditure for FY19 is expected to be 9% lower than guided in March 2019, primarily due to Thabametsi and GG6 delays, partially offset by Belfast early production. As we proceed with our portfolio optimisation efforts, we will adhere to our capital allocation framework previously communicated. We are particularly proud to announce that we have improved our B-BBEE recognition status from a level 5 for FY17 to a level 2 for FY18. This milestone is testament to Exxaro’s unwavering commitment to transformation by achieving this milestone two years ahead of schedule. It is with great pleasure that we announce that Exxaro will move back into the Top 40 index as part of the JSE’s Quarterly and June 2019 index review. The review changes were effective from the start of business on Monday, 24 June 2019.

Exxaro ranked at position 32 on the review cut date, based on net market cap and as such will be an automatic addition to the Top 40 index with a weighting of approximately 0.70%. We will provide a detailed account of our 1H19 business performance and an outlook on the subsequent six months to year-end (2H19), when we announce our financial results on 22 August 2019. Yours sincerely Riaan Koppeschaar Finance Director

This is an overview of the group’s expected business performance for the period, encompassing strategic, operational and financial information. Unless otherwise indicated, all comparisons are against the six-month period ended 31 December 2018 (2H18). Zero Harm remains Exxaro’s key business objective. In the period we maintained a year-to-date lost-time injury frequency rate (LTIFR) of 0.12 (FY18: 0.12), still above our target of 0.11. We have done better in previous years and remain confident that we will improve on this through ongoing safety initiatives. We are pleased to report zero (0) fatalities for a period of 27 consecutive months as at 31 May 2019 and zero (0) “High Potential Incidents” (HPI’s) so far during 1H19 (1H18: 5HPI’s). Towards the end of 1H19 the US-China trade tension continued to escalate and weighed on global market sentiment. Commodity markets recorded mixed results over the period under review. In respect of Exxaro’s key commodities for 1H19, the API4 coal export price index is expected to average US$75 (2H18: US$99) per tonne, free on board (FOB), and the iron ore fines price US$90 (2H18: US$69) per dry metric tonne, cost and freight (CFR) China.

Total coal production volumes are expected to decrease by 5% (excluding buy-ins), mainly driven by reduced demand from Eskom at Medupi power station, directly resulting in 4% lower coal sales volumes. Commercially, the impact of the reduced Medupi volumes is mitigated due to the contractual agreement in place. While we expect to achieve higher export volumes, it is reasonable to assume that a weaker US$ sales price per tonne will be realised, in line with the weaker API4 coal export price index, cushioned somewhat by a weaker rand/dollar exchange rate. We are pleased with the outcome of our capital allocation programme and will maintain a disciplined approach, particularly in delivering on the sustaining and growth capex programmes while maintaining a strong balance sheet. We are aware that many of our contractors are experiencing financial difficulties and are intensifying engagement with these contractors to minimise any impact on completing our projects.

Coal capital expenditure for FY19 is expected to be 9% lower than guided in March 2019, primarily due to Thabametsi and GG6 delays, partially offset by Belfast early production. As we proceed with our portfolio optimisation efforts, we will adhere to our capital allocation framework previously communicated. We are particularly proud to announce that we have improved our B-BBEE recognition status from a level 5 for FY17 to a level 2 for FY18. This milestone is testament to Exxaro’s unwavering commitment to transformation by achieving this milestone two years ahead of schedule. It is with great pleasure that we announce that Exxaro will move back into the Top 40 index as part of the JSE’s Quarterly and June 2019 index review. The review changes were effective from the start of business on Monday, 24 June 2019.

Exxaro ranked at position 32 on the review cut date, based on net market cap and as such will be an automatic addition to the Top 40 index with a weighting of approximately 0.70%. We will provide a detailed account of our 1H19 business performance and an outlook on the subsequent six months to year-end (2H19), when we announce our financial results on 22 August 2019. Yours sincerely Riaan Koppeschaar Finance Director

Macro economic environment according to Exxaro

GLOBAL ECONOMY AND COMMODITY PRICES

The slowing and stabilisation of global economic growth was evident during the early part of 1H19, before increased geopolitical risks altered the global economic prospects. As a result, global real GDP for 2019 is expected to slow down to 2.8%, compared to 3.2% in 2018. There is an increasing possibility that the Chinese government will ramp up stimulus more aggressively to counter the impact of tariffs on the economy and remain supportive for steel-intensive sectors such as infrastructure, which will be positive for metallurgical coal demand. Chinese steel production has risen considerably during 1H19, and with high iron ore prices and margins well below the 2018 levels, have resulted in steelmakers maintaining low iron ore inventories. Additionally, supply disruptions mainly because of events in Northern Brazil and Western Australia, have kept the global iron ore market balance very tight. The titanium dioxide (TiO2) pigment demand strengthened in most regions, with inventory levels starting to decline for many producers. The period under review was characterized by the reversion of destocking to normalised order patterns. In addition, the TiO2 feedstock market fundamentals remained stable. The brent crude oil price moderated towards the end of 1H19. Concerns about global economic activity, exacerbated by the threat of trade wars and rising tension in the Middle East oil routes, continue to weigh on the global oil market.

OPERATIONAL PERFORMANCE

COAL: MARKETS

Good demand for sized product in the domestic market continued. As more domestic supply was available due to weak export prices, domestic pricing remained flat in real terms. The export sales prices came under severe pressure, trading at levels last seen in 2016. The lack of import demand from China continues to put pressure on Pacific coal prices. European stock levels are at record levels amidst very high levels of renewable energy generation and very low gas prices leading to coal-to-gas switching. India continues to draw South African coal, however, the demand has switched to higher calorific value coal.

COAL: LOGISTICS AND INFRASTRUCTURE

Transnet Freight Rail (TFR) railed 30.51Mt to RBCT from January 2019 to May 2019 equivalent to an annualised rail tempo of 70.24Mtpa. TFR’s North-West Corridor expansion project has remained on schedule, with an increased focus on operational readiness, managed by a joint forum together with Exxaro. This will lead to improved operational performance in anticipation of the planned tonnage ramp-up, resulting in a 20% increase in the average weekly export trains dispatched from Grootegeluk, from 4 trains per week in 2018 to 4.8 trains per week for January 2019 to May 2019.

FERROUS OTHER: SISHEN IRON ORE COMPANY PROPRIETARY LIMITED (SIOC)

Guidance on SIOC’s equity-accounted contribution will be provided when we have reasonable certainty on its 1H19 financial results. ENERGY: CENNERGI PROPRIETARY LIMITED (CENNERGI) The Tsitsikamma Community Wind Farm (TCWF) suffered 2 separate fire incidents, destroying two turbines. The investigations are near final and replacement turbines are scheduled to be delivered in 3Q19, with commissioning to be completed early in 4Q19. Good energy generation numbers for the year to date have more than offset the generation loss due to the two fire incidents. CAPITAL ALLOCATION Exxaro’s focus remains on implementing our extensive portfolio of growth and sustaining capital within time and budget, despite financial challenges facing many of our project contractors. During 1Q19 Exxaro was forced to terminate its contract with Group Five, who was responsible for the silo, small-coal plant and balance of the plant infrastructure as part of the GG6 expansion project.

The slowing and stabilisation of global economic growth was evident during the early part of 1H19, before increased geopolitical risks altered the global economic prospects. As a result, global real GDP for 2019 is expected to slow down to 2.8%, compared to 3.2% in 2018. There is an increasing possibility that the Chinese government will ramp up stimulus more aggressively to counter the impact of tariffs on the economy and remain supportive for steel-intensive sectors such as infrastructure, which will be positive for metallurgical coal demand. Chinese steel production has risen considerably during 1H19, and with high iron ore prices and margins well below the 2018 levels, have resulted in steelmakers maintaining low iron ore inventories. Additionally, supply disruptions mainly because of events in Northern Brazil and Western Australia, have kept the global iron ore market balance very tight. The titanium dioxide (TiO2) pigment demand strengthened in most regions, with inventory levels starting to decline for many producers. The period under review was characterized by the reversion of destocking to normalised order patterns. In addition, the TiO2 feedstock market fundamentals remained stable. The brent crude oil price moderated towards the end of 1H19. Concerns about global economic activity, exacerbated by the threat of trade wars and rising tension in the Middle East oil routes, continue to weigh on the global oil market.

OPERATIONAL PERFORMANCE

COAL: MARKETS

Good demand for sized product in the domestic market continued. As more domestic supply was available due to weak export prices, domestic pricing remained flat in real terms. The export sales prices came under severe pressure, trading at levels last seen in 2016. The lack of import demand from China continues to put pressure on Pacific coal prices. European stock levels are at record levels amidst very high levels of renewable energy generation and very low gas prices leading to coal-to-gas switching. India continues to draw South African coal, however, the demand has switched to higher calorific value coal.

COAL: LOGISTICS AND INFRASTRUCTURE

Transnet Freight Rail (TFR) railed 30.51Mt to RBCT from January 2019 to May 2019 equivalent to an annualised rail tempo of 70.24Mtpa. TFR’s North-West Corridor expansion project has remained on schedule, with an increased focus on operational readiness, managed by a joint forum together with Exxaro. This will lead to improved operational performance in anticipation of the planned tonnage ramp-up, resulting in a 20% increase in the average weekly export trains dispatched from Grootegeluk, from 4 trains per week in 2018 to 4.8 trains per week for January 2019 to May 2019.

FERROUS OTHER: SISHEN IRON ORE COMPANY PROPRIETARY LIMITED (SIOC)

Guidance on SIOC’s equity-accounted contribution will be provided when we have reasonable certainty on its 1H19 financial results. ENERGY: CENNERGI PROPRIETARY LIMITED (CENNERGI) The Tsitsikamma Community Wind Farm (TCWF) suffered 2 separate fire incidents, destroying two turbines. The investigations are near final and replacement turbines are scheduled to be delivered in 3Q19, with commissioning to be completed early in 4Q19. Good energy generation numbers for the year to date have more than offset the generation loss due to the two fire incidents. CAPITAL ALLOCATION Exxaro’s focus remains on implementing our extensive portfolio of growth and sustaining capital within time and budget, despite financial challenges facing many of our project contractors. During 1Q19 Exxaro was forced to terminate its contract with Group Five, who was responsible for the silo, small-coal plant and balance of the plant infrastructure as part of the GG6 expansion project.

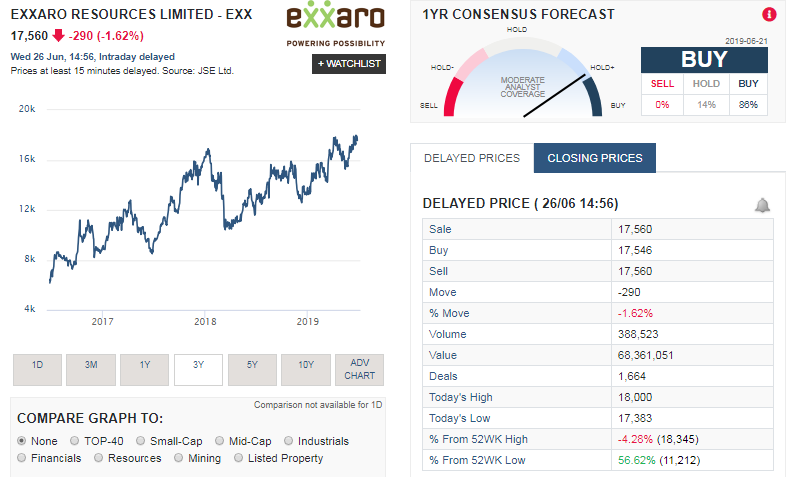

Share Price Performance of Exxaro (EXX)

The screenshot below, taken from Sharenet shows the share price history of Exxaro for the last three years as well as the share price performance over various time periods

The summary below shows the performance of Exxaro's share price over various time periods:

So its pretty clear that the share price performance of EXX over the last three years has rewarded investors handsomely. The last month alone it returned more to investors than what investors could hope to earn in a year from a savings deposit.

- 1 week: 3.69%

- 1 month: 10.66%

- Year to date (YTD): 29.47%

- 1 year: 52.15%

- 3 year: 176.74%

- 5 year: 27.51%

So its pretty clear that the share price performance of EXX over the last three years has rewarded investors handsomely. The last month alone it returned more to investors than what investors could hope to earn in a year from a savings deposit.

Exxaro (EXX) shares valuation as at 15 March 2019

So what are Exxaro shares worth based on their bumper set of financial results? We are a litte concerned about the fact that they are stating they cannot compete against product supplied by certain countries such as Colombia. The worry is the oversupply of coal to big coal users. All this will do is force down international coal prices which will eat into the currently very health profit margins of Exxaro.

All things considered, including their low PE ratio, strong dividend yield, their massive global footprint in terms of where they can sell their product we value the group's share at R203 a share. That will place the group on a PE ratio of 9.4 and a dividend yield of 5.34%, neither of which is demanding at that price. We therefore feel Exxaro shares at their current price offers good value for investors.

All things considered, including their low PE ratio, strong dividend yield, their massive global footprint in terms of where they can sell their product we value the group's share at R203 a share. That will place the group on a PE ratio of 9.4 and a dividend yield of 5.34%, neither of which is demanding at that price. We therefore feel Exxaro shares at their current price offers good value for investors.