|

Related Topics |

|

We take a look at the latest interim year financial results for coal mining giant, Exxaro resources for the period ending June 2019. And good news for shareholders is the fact that Exxaro is paying a massive interim dividend as well as a big fat special dividend to shareholders.

|

|

About Exxaro (EXX)

In November 2006, Kumba Resources Limited unbundled and Kumba’s coal and other assets merged with Eyesizwe Coal to create Exxaro Resources Limited. We have since grown to become one of the largest and foremost black-empowered coal and heavy mineral companies in South Africa, with other business interests around the world in Europe, the United States of America, and Australia. Our asset portfolio includes coal operations and investments in iron ore, pigment manufacturing, renewable energy (wind), and residual base metals.

In the last decade, Exxaro has established itself as an organisation that is respected by its peers for its innovation, ethics, and integrity. We’ve achieved this by acknowledging that we exist in a greater context. We are here to power better lives today and tomorrow, in South Africa and beyond.

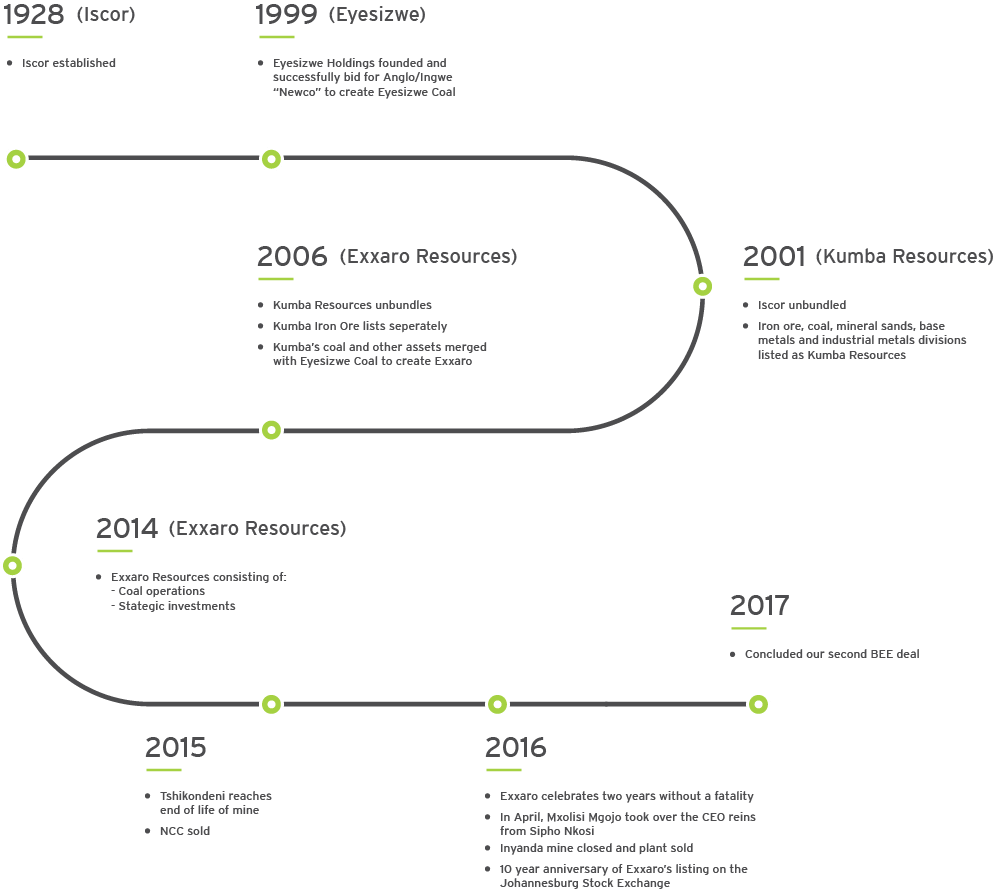

The image below shows the evolution and current company profile of Exxaro Resources

In the last decade, Exxaro has established itself as an organisation that is respected by its peers for its innovation, ethics, and integrity. We’ve achieved this by acknowledging that we exist in a greater context. We are here to power better lives today and tomorrow, in South Africa and beyond.

The image below shows the evolution and current company profile of Exxaro Resources

The evolution of Exxaro

Financial Results Overview

Firstly we take a look at the financial highlights as stated by EXX's management

Group financial performance

Group financial performance

- Revenue of R12 billion, down 2%

- Net operating profit of R2.4 billion, down 24%

- AEPS of 2 589 cents, up 104%

- HEPS of 1 730 cents, up 42%

- Interim dividend of 864 cents per share, up 334 cents per share

- Special dividend of 897 cents per share

Advertisement (and yes South Africans can buy from Amazon as they ship to SA)

Now for the numbers we are interested in:

- Revenue: R11.961 billion (down 2% from R12.260 in the prior period)

- Operating expenses: R9.584 billion (up 4.9% from R9.134 billion in the prior period)

- Profit for the period: R6.444 billion (up 100% from R3.218 billion in the prior year)

- Net profit margin: 53.8%

- Diluted Headline earnings per share: R19.69 (up 55.2% from R12.68 in the prior period)

- PE ratio: 6.75

- Interim dividend declared for period: R8.64 (up 63% on prior year)

- Special dividend: R8.97 a share

- Dividend yield (including special dividend and assuming same end year dividend): 19.7%

- Inventories: R1.86 billion (up 25% from R1.485 billion in previous period)

- Cash generated from operating activities : R3.2 billion (down 18% compared to the prior year)

- Cash generated from operations per share: R8.9 per share

- Net asset value per share: R125.41 (up 16.1% from R108.03 in the prior year)

- So trading at about 1.06 times its stated net asset value.

- Cash on balance sheet: R4.29 billion (up 65% from R2.596 billion in the prior year)

- Cash on balance sheet per share: R11.78 or 8.9% of the current share price

Management commentary on the results

Good demand for sized product in the domestic market continued. As more domestic supply was available due to weak export prices, domestic pricing remained flat in real terms. The export sales prices came under severe pressure, trading at levels last seen in 2016. The lack of import demand from China continues to put pressure on Pacific coal prices. European stock levels are at record levels amidst very high levels of renewable energy generation and very low gas prices leading to coal-to-gas switching. India continues to import South African coal. However, the demand has switched to higher calorific value coal which is favourable to Exxaro’s strategy. The benchmark API4 RBCT export price averaged US$74 per tonne in 1H19 compared to US$97 per tonne in 1H18. Our export volumes increased by 9% from 3.9Mt in 1H18 to 4.3Mt in 1H19. The group realised an average export price of US$54 per tonne in 1H19 against US$79 in 1H18.

Production and sales volumes

Coal production volumes (excluding buy-ins and semi-coke) were down 1 411kt (-6%), thereby impacting sales volumes by -8%. The decrease can mainly be attributed to the divestment of NBC at end of October 2018, lower production at Matla as well as lower production at Grootegeluk due to the lower demand from Eskom for the Medupi Power Station.

Thermal coal

Commercial: Waterberg Production at Grootegeluk declined by 794kt (-6%) due to the lower demand from Eskom for the Medupi Power Station. This also resulted in a decrease in sales volumes of 686kt (-6%) and an increase in the strategic stock pile levels. Commercial: Mpumalanga The commercial Mpumalanga mines’ thermal coal production was 324kt (+6%) higher compared to 1H18 driven by:

– Higher production at Mafube of 731kt as Nooitgedacht ramps up

– Higher production at Leeuwpan of 208kt due to the change in production specifications resulting in higher yields and improved throughput

– Higher production at ECC of 165kt following the start-up of FZON and increased yield and product achieved at DCME by producing an Eskom product

– Belfast ramping up earlier than expected and producing 164kt.

The increase was partly offset by no volume from NBC (-945kt) as a result of our divestment in 2H18. The commercial Mpumalanga mines’ thermal coal sales were down 309kt (-14%), mainly due to our divestment of NBC (-994kt) in 2H18. The decrease was partly offset by higher sales at Leeuwpan of 437kt (+45%) and ECC of 284kt (+82%) due to a change in market from export to Eskom in 1H19. Exports commercial Export sales increased by 343kt (+9%) as a result of more coal being available from Mafube, ECC, Grootegeluk and Belfast. This was partly offset by lower buy-ins and Leeuwpan supplying coal to Eskom. Tied Coal production and sales from Matla mine were down 929t (-26%), mainly due to the shortwall start-up delay at Mine 2 where 569kt was lost, the shortwall stop at Mine 3 and other production challenges.

Metallurgical coal

Grootegeluk’s metallurgical coal production was in line with the comparative period. Sales volumes were slightly lower by 34kt (-6%) mainly due to the unavailability of trains to dispatch coal to the domestic market.

Ferrous business

Equity-accounted investment

The increase in core equity-accounted income from SIOC of R1 943 million to R2 727 million in 1H19, is primarily driven by the effect of the higher iron-ore prices realised and a weaker exchange rate.

Titanium dioxide

Equity-accounted investment

Core equity-accounted income from Tronox SA and UK operations decreased by R113 million to R111 million compared to 1H18. The decrease is mainly as a result of the cessation of applying the equity method to Tronox UK, which was classified as a non-current asset held-for-sale on 30 November 2018.

Energy business Equity-accounted investment Cennergi, a 50% joint venture with Tata Power, recorded core equity-accounted losses of R13 million for 1H19 (1H18: core equity-accounted income of R20 million). The results were negatively impacted by hedge ineffectiveness due to forecast interest rates being lower than the fixed interest rate. Cash flow generation remains positive and in addition to the R58 million dividend received in 2H18, Exxaro received a further dividend of R73 million in 1H19. The two windfarm projects are running at slightly lower than planned capacity due to lower than expected wind speeds, which was offset by better than contracted equipment availability. Electricity generation approximated planned numbers for the first six months, which exceeded expectations, considering that two turbines were destroyed in separate fire incidents. The claims for physical damage and loss of business are in progress. Replacement turbines are scheduled for delivery and installation during this 3Q19, with commissioning planned for 4Q19.

Outlook

Increasing geopolitical risks and aggressive trade policies are anticipated to weigh on global economic activity during 2H19. In terms of the global coal market, we do not see a recovery from the current pricing and demand balance. China will continue to influence the supply/demand balance in the Pacific with related price volatility. With the oversupply of coal in the Atlantic Basin, coupled with gas price forecasts remaining low, the market remains bearish for the remainder of the year. We therefore expect the API4 price index to remain under pressure.

The weak South African growth outcome has raised the risk of a sovereign rating downgrade towards the end of 2H19. The rand/dollar exchange rate is expected to remain volatile. We expect domestic coal demand and pricing to remain stable for the remainder of the year. The Medupi Power Station offtake from Grootegeluk is expected to remain as per the offtake plan for the remainder of 2019. We welcome government’s commitments in the short term towards Eskom; however, much more structural and sustainable reforms are required to inject the confidence required that will build the economy and create the employment opportunities so desperately required. As we roll out the integrated operations centres (IOCs) at all our operations, in terms of our digitalisation plan, the increased visualisation of the mining value chain will highlight inefficiencies that will be addressed through improved decision-making relating to safety, productivity and cost performance. During 2H19, the performance of our SIOC investment will be well supported by the momentum from 1H19, a tight iron ore market, strong fines price with above average lump premium and continued stable demand for higher-grade products. However, an expected recovery in seaborne supply, with moderation of Chinese demand may dampen current market enthusiasm. Exxaro’s stake in Tronox Holdings plc has been reduced to approximately 14.7 million shares, representing about 10% of the total outstanding shares at 30 June 2019.

We remain committed to monetising our remaining stake in Tronox Holdings plc over time and in the best possible manner, taking into account prevailing market conditions. In respect of the Moranbah South hard coking coal project, Exxaro, together with Anglo Coal, is in the process of reassessing the potential development plan for the project. Our response to climate change requires much more definitive and structural changes to our business model. We are feeling the impact of increasing societal demand for proactive response and action to climate change:

– Firstly, through enquiry from shareholders about our climate risk response

– Secondly, we are experiencing higher insurance premiums in the renewal of our insurance policies and will be incurring increased costs resulting from the recently introduced Carbon Tax Bill

– Lastly, the continuing delay in the granting of an operating licence for the Thabametsi Coal IPP, impacting on the development of the Thabametsi coal mine.

Therefore, the impact of climate change on our business is systemic and requires a response that will ensure a sustainable Exxaro in a carbon constrained environment. The migration to a lower carbon environment has to be JUST and conscious to potentially negative impacts on our stakeholders, especially the poor and needy in South Africa. We will present to you, in due course, our climate response strategy, including our progress with incorporating the recommendations from the FSB’s Taskteam on Climate-related Financial Disclosures (TCFD) which highlight climate change transitional and physical risks confronting our business and the related financial impacts of these risks.

Production and sales volumes

Coal production volumes (excluding buy-ins and semi-coke) were down 1 411kt (-6%), thereby impacting sales volumes by -8%. The decrease can mainly be attributed to the divestment of NBC at end of October 2018, lower production at Matla as well as lower production at Grootegeluk due to the lower demand from Eskom for the Medupi Power Station.

Thermal coal

Commercial: Waterberg Production at Grootegeluk declined by 794kt (-6%) due to the lower demand from Eskom for the Medupi Power Station. This also resulted in a decrease in sales volumes of 686kt (-6%) and an increase in the strategic stock pile levels. Commercial: Mpumalanga The commercial Mpumalanga mines’ thermal coal production was 324kt (+6%) higher compared to 1H18 driven by:

– Higher production at Mafube of 731kt as Nooitgedacht ramps up

– Higher production at Leeuwpan of 208kt due to the change in production specifications resulting in higher yields and improved throughput

– Higher production at ECC of 165kt following the start-up of FZON and increased yield and product achieved at DCME by producing an Eskom product

– Belfast ramping up earlier than expected and producing 164kt.

The increase was partly offset by no volume from NBC (-945kt) as a result of our divestment in 2H18. The commercial Mpumalanga mines’ thermal coal sales were down 309kt (-14%), mainly due to our divestment of NBC (-994kt) in 2H18. The decrease was partly offset by higher sales at Leeuwpan of 437kt (+45%) and ECC of 284kt (+82%) due to a change in market from export to Eskom in 1H19. Exports commercial Export sales increased by 343kt (+9%) as a result of more coal being available from Mafube, ECC, Grootegeluk and Belfast. This was partly offset by lower buy-ins and Leeuwpan supplying coal to Eskom. Tied Coal production and sales from Matla mine were down 929t (-26%), mainly due to the shortwall start-up delay at Mine 2 where 569kt was lost, the shortwall stop at Mine 3 and other production challenges.

Metallurgical coal

Grootegeluk’s metallurgical coal production was in line with the comparative period. Sales volumes were slightly lower by 34kt (-6%) mainly due to the unavailability of trains to dispatch coal to the domestic market.

Ferrous business

Equity-accounted investment

The increase in core equity-accounted income from SIOC of R1 943 million to R2 727 million in 1H19, is primarily driven by the effect of the higher iron-ore prices realised and a weaker exchange rate.

Titanium dioxide

Equity-accounted investment

Core equity-accounted income from Tronox SA and UK operations decreased by R113 million to R111 million compared to 1H18. The decrease is mainly as a result of the cessation of applying the equity method to Tronox UK, which was classified as a non-current asset held-for-sale on 30 November 2018.

Energy business Equity-accounted investment Cennergi, a 50% joint venture with Tata Power, recorded core equity-accounted losses of R13 million for 1H19 (1H18: core equity-accounted income of R20 million). The results were negatively impacted by hedge ineffectiveness due to forecast interest rates being lower than the fixed interest rate. Cash flow generation remains positive and in addition to the R58 million dividend received in 2H18, Exxaro received a further dividend of R73 million in 1H19. The two windfarm projects are running at slightly lower than planned capacity due to lower than expected wind speeds, which was offset by better than contracted equipment availability. Electricity generation approximated planned numbers for the first six months, which exceeded expectations, considering that two turbines were destroyed in separate fire incidents. The claims for physical damage and loss of business are in progress. Replacement turbines are scheduled for delivery and installation during this 3Q19, with commissioning planned for 4Q19.

Outlook

Increasing geopolitical risks and aggressive trade policies are anticipated to weigh on global economic activity during 2H19. In terms of the global coal market, we do not see a recovery from the current pricing and demand balance. China will continue to influence the supply/demand balance in the Pacific with related price volatility. With the oversupply of coal in the Atlantic Basin, coupled with gas price forecasts remaining low, the market remains bearish for the remainder of the year. We therefore expect the API4 price index to remain under pressure.

The weak South African growth outcome has raised the risk of a sovereign rating downgrade towards the end of 2H19. The rand/dollar exchange rate is expected to remain volatile. We expect domestic coal demand and pricing to remain stable for the remainder of the year. The Medupi Power Station offtake from Grootegeluk is expected to remain as per the offtake plan for the remainder of 2019. We welcome government’s commitments in the short term towards Eskom; however, much more structural and sustainable reforms are required to inject the confidence required that will build the economy and create the employment opportunities so desperately required. As we roll out the integrated operations centres (IOCs) at all our operations, in terms of our digitalisation plan, the increased visualisation of the mining value chain will highlight inefficiencies that will be addressed through improved decision-making relating to safety, productivity and cost performance. During 2H19, the performance of our SIOC investment will be well supported by the momentum from 1H19, a tight iron ore market, strong fines price with above average lump premium and continued stable demand for higher-grade products. However, an expected recovery in seaborne supply, with moderation of Chinese demand may dampen current market enthusiasm. Exxaro’s stake in Tronox Holdings plc has been reduced to approximately 14.7 million shares, representing about 10% of the total outstanding shares at 30 June 2019.

We remain committed to monetising our remaining stake in Tronox Holdings plc over time and in the best possible manner, taking into account prevailing market conditions. In respect of the Moranbah South hard coking coal project, Exxaro, together with Anglo Coal, is in the process of reassessing the potential development plan for the project. Our response to climate change requires much more definitive and structural changes to our business model. We are feeling the impact of increasing societal demand for proactive response and action to climate change:

– Firstly, through enquiry from shareholders about our climate risk response

– Secondly, we are experiencing higher insurance premiums in the renewal of our insurance policies and will be incurring increased costs resulting from the recently introduced Carbon Tax Bill

– Lastly, the continuing delay in the granting of an operating licence for the Thabametsi Coal IPP, impacting on the development of the Thabametsi coal mine.

Therefore, the impact of climate change on our business is systemic and requires a response that will ensure a sustainable Exxaro in a carbon constrained environment. The migration to a lower carbon environment has to be JUST and conscious to potentially negative impacts on our stakeholders, especially the poor and needy in South Africa. We will present to you, in due course, our climate response strategy, including our progress with incorporating the recommendations from the FSB’s Taskteam on Climate-related Financial Disclosures (TCFD) which highlight climate change transitional and physical risks confronting our business and the related financial impacts of these risks.

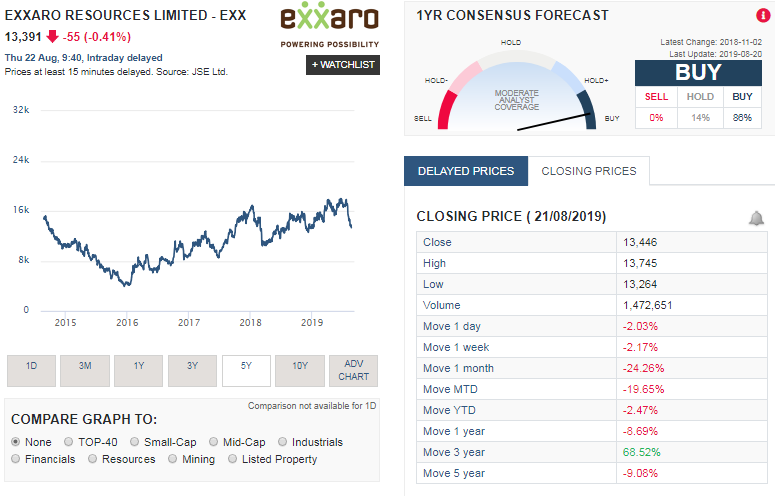

Share Price Performance of Exxaro (EXX)

The screenshot below, taken from Sharenet shows the share price history of Exxaro for the last five years as well as the share price performance over various time periods

The summary below shows the performance of Exxaro's share price over various time periods:

So its pretty clear that the share price performance of EXX over the last three years has rewarded investors handsomely. However the performance over longer and shorter periods has been negative with EXX taking its shareholders on a wild ride as the share price swings up and down.

- 1 week: -2.17%

- 1 month: -24.26%

- Year to date (YTD): -2.47%

- 1 year: -8.69%

- 3 years: 68.52%

- 5 years: -9.08%

So its pretty clear that the share price performance of EXX over the last three years has rewarded investors handsomely. However the performance over longer and shorter periods has been negative with EXX taking its shareholders on a wild ride as the share price swings up and down.

Exxaro (EXX) shares valuation

During on 15 March 2019 valuation of Exxaro's shares we said we valued the group at R203 a share. The question is whether we still value them at this level after their latest interim results and the massive special dividend the group declared? All things considered especially looking at their improved cash on balance sheet position the strong dividend and interim dividend paid, the cash generated per share we value the group's shares at R189 a share (a few Rands lower than our previous valuation to account for declining revenues and the build up of inventories).

A few concerns for us is the decline in their revenues and the concerns raised in the past by Exxaro that they cannot compete against cheaper products as supplied by countries like Colombia. Another worry is the sharp increase in Exxaro's inventories. Are they building up stock piles as they cannot offset their products at the price they need to or is the market being flooded by cheaper supplies from countries such as Colombia? So one has to be slightly concerned about the rise in their inventories

But all in all a solid set of results and investors will be rewarded handsomely with a strong dividend payout. Another reassuring number is the fact that its net asset value is sitting at R125 a share, and the group is trading at close to it, which if there is to be downside to Exx's shares it is unlikely to drop to far below their net asset value. So this provides investors with a buffer against any potential downside risk.

A few concerns for us is the decline in their revenues and the concerns raised in the past by Exxaro that they cannot compete against cheaper products as supplied by countries like Colombia. Another worry is the sharp increase in Exxaro's inventories. Are they building up stock piles as they cannot offset their products at the price they need to or is the market being flooded by cheaper supplies from countries such as Colombia? So one has to be slightly concerned about the rise in their inventories

But all in all a solid set of results and investors will be rewarded handsomely with a strong dividend payout. Another reassuring number is the fact that its net asset value is sitting at R125 a share, and the group is trading at close to it, which if there is to be downside to Exx's shares it is unlikely to drop to far below their net asset value. So this provides investors with a buffer against any potential downside risk.