|

Related Topics |

|

We take a look at the latest full year financial results for coal mining giant, Exxaro resources for the period ending December 2018.

|

|

About Exxaro (EXX)

In November 2006, Kumba Resources Limited unbundled and Kumba’s coal and other assets merged with Eyesizwe Coal to create Exxaro Resources Limited. We have since grown to become one of the largest and foremost black-empowered coal and heavy mineral companies in South Africa, with other business interests around the world in Europe, the United States of America, and Australia. Our asset portfolio includes coal operations and investments in iron ore, pigment manufacturing, renewable energy (wind), and residual base metals.

In the last decade, Exxaro has established itself as an organisation that is respected by its peers for its innovation, ethics, and integrity. We’ve achieved this by acknowledging that we exist in a greater context. We are here to power better lives today and tomorrow, in South Africa and beyond.

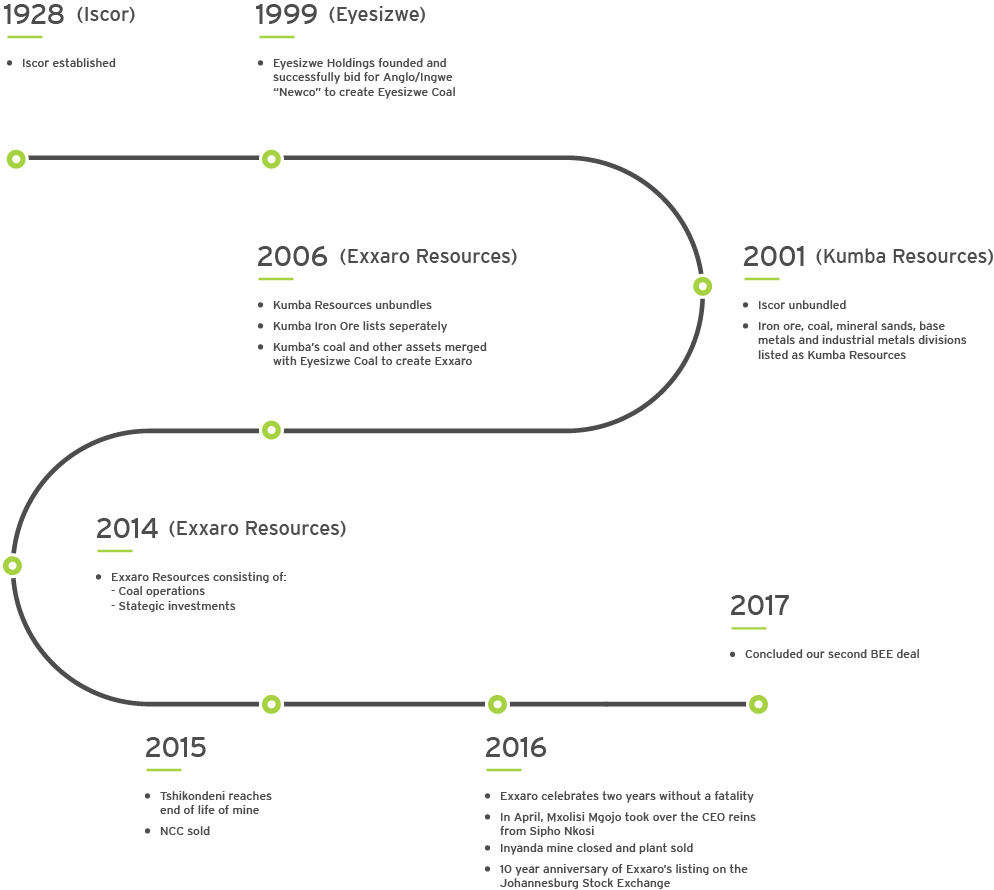

The image below shows the evolution and current company profile of Exxaro Resources

In the last decade, Exxaro has established itself as an organisation that is respected by its peers for its innovation, ethics, and integrity. We’ve achieved this by acknowledging that we exist in a greater context. We are here to power better lives today and tomorrow, in South Africa and beyond.

The image below shows the evolution and current company profile of Exxaro Resources

The evolution of Exxaro

Financial Results Overview

Firstly we take a look at the financial highlights as stated by EXX's management

Group financial performance

Coal operational performance

Now for the numbers we are interested in:

Group financial performance

- Revenue R25.5 billion, up 12%

- Core EBITDA R7.3 billion, up 1%

- Core headline earnings of R21.59 per share, up 7%

- Cash generated from operations R7.0 billion, up 3%

- Final cash dividend of R5.55 per share, total dividend of R10.85 per share, up 55%

Coal operational performance

- Record production volumes of 47.8Mt

- Record sales volumes of 45.2Mt

- Record export volumes of 8.0Mt

Now for the numbers we are interested in:

- Revenue: R25.491 billion (up 12% from R22.81 in the prior period)

- Operating expenses: R19.79 billion (up % from R17.59 billion in the prior period)

- Profit for the period: R7.062 billion (up % from R6.032 billion in the prior year)

- Net profit margin: 27.7%

- Diluted Headline earnings per share: R21.56 (up 25.1% from R17.24 in the prior period)

- PE ratio: 7.3

- Dividend declared for period: R10.85 (up 55% on prior year)

- Dividend yield: 6.8%

- Cash generated from operating activities : R7 billion (up 2.4% from R6.83 billion in the prior year)

- Cash generated from operations per share: R19.51 per share

- Net asset value per share: R114.70 (up 4.5% from R109.74 in the prior year)

- So trading at about 1.38 times its stated net asset value.

- Cash on balance sheet: R2 billion (down - 70% from R6.65 billion in the prior year)

- Cash on balance sheet per share: R5.58 or 3.5% of the current share price

Management commentary on the results

Group revenue rose 12% to R25 491 million (FY17: R22 813 million), mainly due to higher coal selling prices and

higher Eskom commercial volumes at Grootegeluk, based on demand from Medupi power station, partially offset by

a lower quality product mix. The average price per tonne achieved on exports was US$77 (FY17: US$69). The average

spot exchange rate realised was marginally stronger at R13.24 to the US dollar (FY17: R13.30).

Trading conditions in the domestic market were strong in FY18, resulting in all premium product being sold at stable prices. Our supply to Eskom increased in line with contractual commitments while all other markets remained stable.

The international export market recorded strong demand for most of 2018. India increased its demand for South African lower-grade material up to 3Q18, when the market became oversupplied with coal from Indonesia and Australia after the ban on coal imports by China. Demand from South Korea slowed in 2018 as South African coal could not compete with Colombian material, but new opportunities came from Japan after Exxaro shipped a trial cargo to a power plant and received a new order for 2019. In Pakistan, new coal-fired power plants were commissioned in 2018, increasing annual coal demand to 6Mtpa from the traditional 4Mtpa.

We made further inroads into the Pakistan market, supplying both the power plant and cement industries. China has recently relaxed the ban on coal imports. However, there is still a strong indication that it will continue to protect its domestic market by limiting coal imports. If China imposes a further ban on imports, this will have a negative impact on coal pricing, especially into India. In addition to favourable domestic and international trading conditions, we realised year-on-year operational excellence improvements and successfully implemented two key initiatives, namely visualisation of our mining value chain and the integrated operations centre at some of our major mines, focused on eliminating systemic waste.

OUTLOOK

We expect sustainable improvement in the physical operating results for the coal business by embedding our business optimisation and operational excellence initiatives across all operations, and unlocking value through data analytics and value-chain integration. We are proud to report that we are on track and within budget to deliver value on our coal capital projects, spending more that R20 billion over the next five years to increase sales volumes from 45Mtpa in FY18 to more that 60Mtpa by FY23. The Belfast and Leeuwpan Lifex projects are ahead of schedule, while the GG6 expansion and Grootgeluk rapid loan out station projects are impacted by community and labour related activities in the Lephalale area. We continue to engage with contractors faced with labour unrest and corporate uncertainty.

A stable domestic market is anticipated for 1H19, supported by healthy prices due to tight supply in premium quality sized coal. In Mpumalanga Eskom has, due to the termination of several coal supply agreements, requested industry participants for expressions of interest to supply coal on a short-term basis while it is looking to enter into longer-term contracts. This is positive for Exxaro as it provides more flexibility between various markets. We remain positive that the outcome of the national elections on 8 May 2019 will put South Africa on a renewed investment and economic growth path urgently needed to address the socioeconomic challenges the country is facing. Exxaro is fully supportive of the investment drive spearheaded by the Presidency.

The international market remains largely bearish owing to possible market oversupply, which hinges on China and its ban on coal imports. An increase in coal demand is expected in India, a market that is likely to remain our main export destination. Market conditions are expected to be supportive in 2019. We remain confident that through our well-diversified coal portfolio, we will continue to explore more opportunities in emerging markets where coal-fired power plants are being commissioned. In 1H19, the performance of our SIOC investment will be boosted by higher iron ore prices after supply disruptions in Brazil, a relative high global lump premium and a weak rand/US dollar exchange rate. Although global economic activity is edging down and market sentiment is challenging, commodity price support in 2H18 is expected to continue into 1H19. However, global policy tensions, especially on trade, remain the biggest threat to global growth. The rand/US dollar exchange rate is expected to remain volatile during the period.

Trading conditions in the domestic market were strong in FY18, resulting in all premium product being sold at stable prices. Our supply to Eskom increased in line with contractual commitments while all other markets remained stable.

The international export market recorded strong demand for most of 2018. India increased its demand for South African lower-grade material up to 3Q18, when the market became oversupplied with coal from Indonesia and Australia after the ban on coal imports by China. Demand from South Korea slowed in 2018 as South African coal could not compete with Colombian material, but new opportunities came from Japan after Exxaro shipped a trial cargo to a power plant and received a new order for 2019. In Pakistan, new coal-fired power plants were commissioned in 2018, increasing annual coal demand to 6Mtpa from the traditional 4Mtpa.

We made further inroads into the Pakistan market, supplying both the power plant and cement industries. China has recently relaxed the ban on coal imports. However, there is still a strong indication that it will continue to protect its domestic market by limiting coal imports. If China imposes a further ban on imports, this will have a negative impact on coal pricing, especially into India. In addition to favourable domestic and international trading conditions, we realised year-on-year operational excellence improvements and successfully implemented two key initiatives, namely visualisation of our mining value chain and the integrated operations centre at some of our major mines, focused on eliminating systemic waste.

OUTLOOK

We expect sustainable improvement in the physical operating results for the coal business by embedding our business optimisation and operational excellence initiatives across all operations, and unlocking value through data analytics and value-chain integration. We are proud to report that we are on track and within budget to deliver value on our coal capital projects, spending more that R20 billion over the next five years to increase sales volumes from 45Mtpa in FY18 to more that 60Mtpa by FY23. The Belfast and Leeuwpan Lifex projects are ahead of schedule, while the GG6 expansion and Grootgeluk rapid loan out station projects are impacted by community and labour related activities in the Lephalale area. We continue to engage with contractors faced with labour unrest and corporate uncertainty.

A stable domestic market is anticipated for 1H19, supported by healthy prices due to tight supply in premium quality sized coal. In Mpumalanga Eskom has, due to the termination of several coal supply agreements, requested industry participants for expressions of interest to supply coal on a short-term basis while it is looking to enter into longer-term contracts. This is positive for Exxaro as it provides more flexibility between various markets. We remain positive that the outcome of the national elections on 8 May 2019 will put South Africa on a renewed investment and economic growth path urgently needed to address the socioeconomic challenges the country is facing. Exxaro is fully supportive of the investment drive spearheaded by the Presidency.

The international market remains largely bearish owing to possible market oversupply, which hinges on China and its ban on coal imports. An increase in coal demand is expected in India, a market that is likely to remain our main export destination. Market conditions are expected to be supportive in 2019. We remain confident that through our well-diversified coal portfolio, we will continue to explore more opportunities in emerging markets where coal-fired power plants are being commissioned. In 1H19, the performance of our SIOC investment will be boosted by higher iron ore prices after supply disruptions in Brazil, a relative high global lump premium and a weak rand/US dollar exchange rate. Although global economic activity is edging down and market sentiment is challenging, commodity price support in 2H18 is expected to continue into 1H19. However, global policy tensions, especially on trade, remain the biggest threat to global growth. The rand/US dollar exchange rate is expected to remain volatile during the period.

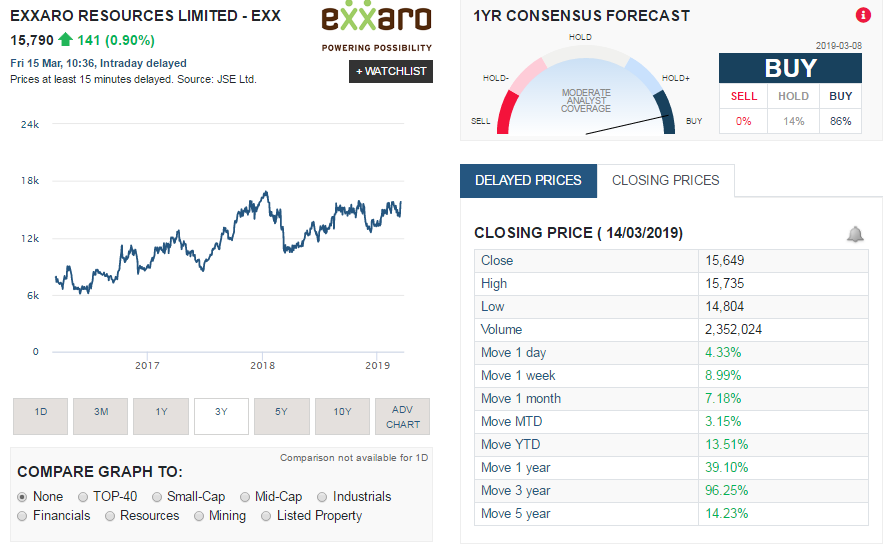

Share Price Performance of Exxaro (EXX)

The screenshot below, taken from Sharenet shows the share price history of Exxaro for the last three years as well as the share price performance over various time periods

The summary below shows the performance of Exxaro's share price over various time periods:

So its pretty clear that the share price performance of EXX over the last three years has rewarded investors handsomely. The last month alone it returned more to investors than what investors could hope to earn in a year from a savings deposit.

- 1 week: 8.99%

- 1 month: 7.18%

- Year to date (YTD): 13.51%

- 1 year: 39.10%

- 3 year: 96.25%

- 5 year: 14.23%

So its pretty clear that the share price performance of EXX over the last three years has rewarded investors handsomely. The last month alone it returned more to investors than what investors could hope to earn in a year from a savings deposit.

Exxaro (EXX) shares valuation

So what are Exxaro shares worth based on their bumper set of financial results? We are a litte concerned about the fact that they are stating they cannot compete against product supplied by certain countries such as Colombia. The worry is the oversupply of coal to big coal users. All this will do is force down international coal prices which will eat into the currently very health profit margins of Exxaro.

All things considered, including their low PE ratio, strong dividend yield, their massive global footprint in terms of where they can sell their product we value the group's share at R203 a share. That will place the group on a PE ratio of 9.4 and a dividend yield of 5.34%, neither of which is demanding at that price. We therefore feel Exxaro shares at their current price offers good value for investors.

All things considered, including their low PE ratio, strong dividend yield, their massive global footprint in terms of where they can sell their product we value the group's share at R203 a share. That will place the group on a PE ratio of 9.4 and a dividend yield of 5.34%, neither of which is demanding at that price. We therefore feel Exxaro shares at their current price offers good value for investors.