|

Related Topics |

|

We take a look at whether South Africa will be heading towards expansionary monetary policy towards the end of 2019 following the disappointing GDP numbers for the first quarter of 2019 in South Africa.

|

|

Will South Africa's monetary policy shift towards expansionary towards end of 2019

Considering South Africa's poor GDP numbers for the first quarter of 2019, and its relatively subdued inflation numbers, will the South African Reserve Bank (SARB) finally shift towards implementing expansionary monetary policy in order to assist economic growth in South Africa? We believe they should and we fall within the camp that believe the SARB monetary policy committee (MPC) has stared itself blind against inflation and inflation targeting and has been neglecting the other part of their mandate which covers balanced and sustainable growth.

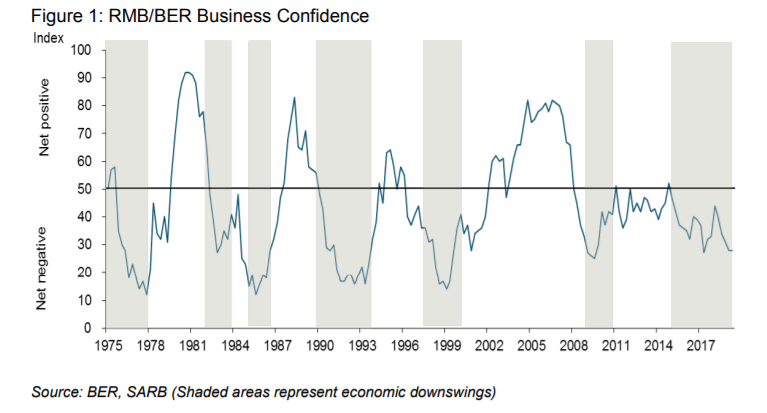

The RMB/BER Business Confidence Index (BCI) flatlined at a worryingly low 28 in the second quarter. More than seven out of ten respondents therefore remained unsatisfied with current business conditions. The last time sentiment was this gloomy was two years ago, and before that, during the global financial-crisis-induced 2009 recession.

RMB/BER business confidence index

South Africa's GDP declined by -3.2% in the first quarter of 2019 when compared to the fourth quarter of 2018, with 7 of the 10 biggest sectors in the economy showing declines. So it is not as if or two particular sectors dragged South Africa's economy down. The decline was relatively broad based. So action is required to get this economy kick started. Government is struggling to kick start if from a fiscal policy (government spending and taxes) point of view, as declining economic activity has lead to less taxes being collected, or tax collection growth slowing, so if government wants to increase spending it needs to borrow more. The problem for South Africa's fiscal policy is the fact that large scale corruption and state capture has seen valuable funds that should have been allocated towards infrastructure development projects funneled away into corrupt officials and companies bank accounts instead of being used for what it has been intended for. This has stunted economic development and growth in South Africa and foreigners (and foreign companies) dont want to invest in a country where there is low to no growth and massive policy uncertainty (think about land expropriation without compensation). So investments into South Africa's economy has basically grind to a halt thanks to the mismanagement of the economy over the last decade (largely under president Jacob Zuma).

Added to this government is looking to curb their excessive spending and their high wage bill, to the extent that they are offering civil servants over the age of 55 a way out of the public service by offering them early retirement without having their pension benefits being penalized. So it is clear that fiscal policy wont be expansionary (spending increasing substantially to boost investment and growth) anytime soon. So the only other avenue government can look towards for growth is monetary policy.

The South African Reserve Bank is independent and implements it mandate free from government inputs or interference. But their mandate is set by the National Treasury.

Added to this government is looking to curb their excessive spending and their high wage bill, to the extent that they are offering civil servants over the age of 55 a way out of the public service by offering them early retirement without having their pension benefits being penalized. So it is clear that fiscal policy wont be expansionary (spending increasing substantially to boost investment and growth) anytime soon. So the only other avenue government can look towards for growth is monetary policy.

The South African Reserve Bank is independent and implements it mandate free from government inputs or interference. But their mandate is set by the National Treasury.

So in recent months there has been a lot of noise regarding the South African Reserve Bank (SARB) and its mandate and whether inflation targeting is still the best mandate for South Africa. While there is a time and a place for inflation targeting and contractionary monetary policy (increasing interest rates) the world is evolving and so are financial markets and economies. And inflation targeting and raising interest rates when inflation increases due to events outside the control of consumers is ridiculous policy that only serves to harm economic growth and consumer spending. Inflation driven by say a weaker exchange rate, higher oil prices, droughts, supply shortages is known as cost push inflation. Basically inputs costs are pushing up retail costs, or retail/consumer inflation. Raising interest rates and taking away disposable income to address inflation caused by such factors is madness as its not consumers fault and its not driven by consumers behaviour. So all it does is curb consumer spending and economic growth and it doesn't address the cause of such inflation.

If inflation was caused by increased consumer spending and excess demand in the economy due to to much free cash being in consumers hands, then we can understand monetary policy being contractionary (increasing interest rates) to curb consumer spending and to ease inflation levels. The inflation that is caused by excess consumer spending and demand is known as demand pull inflation. South Africa's inflation has not been driven by demand pull factors in years as consumer demand has been weak for years, yet interest rates have been increasing in South Africa (the last increase being in November 2018), which was totally unnecessary.

We believe the penny has finally dropped at the SARB MPC and we predict an interest rate cut coming pretty soon, which should provide some much needed consumer relief to South Africans. The question is by how much will rates be cut. Some have been calling for rate cuts to the tune of 200bp (basically cutting rates from 6.75% to 4.75%). Our latest estimate of Taylor's rule for South Africa shows rates are at least 225bp to high. See this article for the latest on Taylor's rule in South Africa.

If inflation was caused by increased consumer spending and excess demand in the economy due to to much free cash being in consumers hands, then we can understand monetary policy being contractionary (increasing interest rates) to curb consumer spending and to ease inflation levels. The inflation that is caused by excess consumer spending and demand is known as demand pull inflation. South Africa's inflation has not been driven by demand pull factors in years as consumer demand has been weak for years, yet interest rates have been increasing in South Africa (the last increase being in November 2018), which was totally unnecessary.

We believe the penny has finally dropped at the SARB MPC and we predict an interest rate cut coming pretty soon, which should provide some much needed consumer relief to South Africans. The question is by how much will rates be cut. Some have been calling for rate cuts to the tune of 200bp (basically cutting rates from 6.75% to 4.75%). Our latest estimate of Taylor's rule for South Africa shows rates are at least 225bp to high. See this article for the latest on Taylor's rule in South Africa.