|

Related Topics |

|

We take a look at a report from United Nations Conference on Trade and Development (UNCTAD) covering developing countries debt during the time of Covid-19, when government and firms require cash to stimulute growth and get through tough economic times.

|

|

Introduction

The Covid-19 shock is posing unprecedented challenges to advanced country governments. As most have come to recognize, the economic crisis entailed by the pandemic is unique in that it combines a deep supply shock - arising from wide-ranging and prolonged lockdowns of entire economies – with consequent demand shocks – arising from a collapse in corporate investment plans, retrenchment of household spending, rapidly increasing unemployment and patchy social welfare systems reduced to their bare bones after decades of rentier capitalism – as well as radical uncertainty and heightened fragility in financial markets. As a consequence, policy makers have focused on the provision of massive stabilisation packages, designed to flatten both, the contagion curve of the pandemic as well as the curve of economic meltdown and financial panic, through a raft of cash transfers, credit lines and guarantees from governments to households and firms. Doing so depends on the ability of governments to borrow from their central banks – or for central banks to revert to their original role as bankers to their governments – on the required scale, a concept often referred to as ‘fiscal space’. How to deal with this necessary accumulation of government debt in response to the crisis, and in particular, how to avoid the mistake of turning to austerity to make adjustments once the crisis has passed, is already beginning to tax the minds of policymakers in the advanced economies.

If the challenges are huge in advanced economies, they are enormously more daunting in developing economies. While advanced country governments struggle to revamp administrative and regulatory frameworks and to break ideological taboos, developing countries cannot easily flatten the contagion curve by closing down their largely informal economies without facing the prospect of more people dying from starvation than from the Covid-19 illness. Moreover, even the most advanced high-income developing countries with relatively deep financial and banking systems do not have anywhere near the fiscal space that advanced economies can, in principle, unlock. The vast majority of developing countries are heavily reliant on access to the ‘hard currencies’ of advanced countries – earned primarily through commodity and service exports, such as food, oil and tourism, and received through remittances from their diasporas as well as from access to concessional and market-based borrowing –to pay for imports and to meet external debt obligations. Their central banks cannot act as lenders of last resort to their governments at the required scale without risking catastrophic depreciations of their local against hard currencies, and therefore also steep increases in the value of their foreign-currency denominated debt as well as unleashing, potentially, destructive inflationary pressures. This situation is all the more critical where developing countries already face high debt burdens.

The Covid-19 shock has put a glaring spotlight on the difficulties arising from high and rising developing country indebtedness since it is set to turn what was already a dire situation into serial sovereign defaults across the developing world. It has, therefore, turbo charged the need to move from discussion to action on debt matters in developing countries. Following a brief discussion of current debt vulnerabilities in developing countries, this update of UNCTAD’s Trade and Development Report 2019 lays out a series of steps that the international community will need to take if there is to be any hope of salvaging the Agenda 2030 and moving to a more resilient and sustainable future for all countries.

Covid-19 hits developing economies at a time when they had already been struggling with unsustainable debt burdens for many years.

If the challenges are huge in advanced economies, they are enormously more daunting in developing economies. While advanced country governments struggle to revamp administrative and regulatory frameworks and to break ideological taboos, developing countries cannot easily flatten the contagion curve by closing down their largely informal economies without facing the prospect of more people dying from starvation than from the Covid-19 illness. Moreover, even the most advanced high-income developing countries with relatively deep financial and banking systems do not have anywhere near the fiscal space that advanced economies can, in principle, unlock. The vast majority of developing countries are heavily reliant on access to the ‘hard currencies’ of advanced countries – earned primarily through commodity and service exports, such as food, oil and tourism, and received through remittances from their diasporas as well as from access to concessional and market-based borrowing –to pay for imports and to meet external debt obligations. Their central banks cannot act as lenders of last resort to their governments at the required scale without risking catastrophic depreciations of their local against hard currencies, and therefore also steep increases in the value of their foreign-currency denominated debt as well as unleashing, potentially, destructive inflationary pressures. This situation is all the more critical where developing countries already face high debt burdens.

The Covid-19 shock has put a glaring spotlight on the difficulties arising from high and rising developing country indebtedness since it is set to turn what was already a dire situation into serial sovereign defaults across the developing world. It has, therefore, turbo charged the need to move from discussion to action on debt matters in developing countries. Following a brief discussion of current debt vulnerabilities in developing countries, this update of UNCTAD’s Trade and Development Report 2019 lays out a series of steps that the international community will need to take if there is to be any hope of salvaging the Agenda 2030 and moving to a more resilient and sustainable future for all countries.

Covid-19 hits developing economies at a time when they had already been struggling with unsustainable debt burdens for many years.

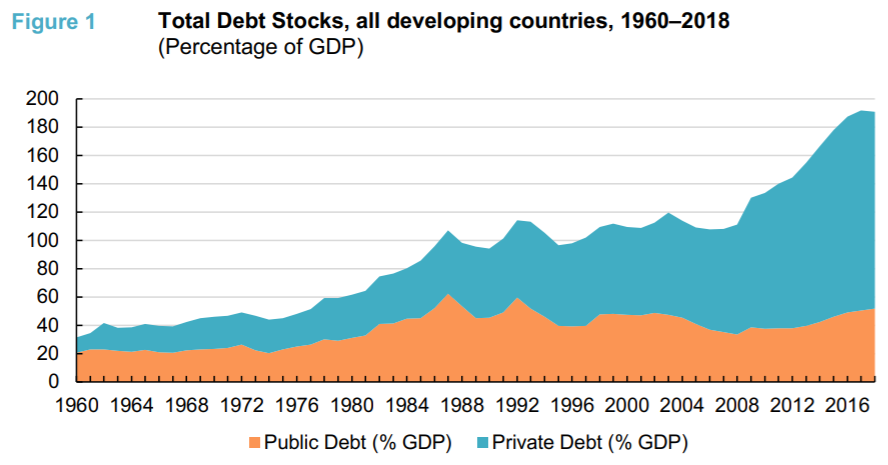

As Figure 1 shows, at end-20183 the total debt stocks of developing countries – external and domestic, private and public – stood at 191 per cent (or almost double) their combined GDP, the highest level on record. A developing country debt crisis, already under way prior to the Covid-19 shock, had many facets , but two are worthwhile putting upfront in the context of ongoing debates about debt relief for the developing world in the aftermath of the Covid-19 shock. First, the unfolding debt crisis was not limited to the poorest of developing countries but affected developing economies of all income categories. Second, it has, by and large, not been caused by economic mismanagement at home, but by economic and financial mismanagement at the global level. Over the past decade, developing countries have witnessed a rapid and often premature integration into heavily underregulated international financial markets, including the so-called shadow-banking sectors, estimated to be in control of around half of the world’s financial assets.

In this context, developing countries became highly vulnerable to massive but volatile flows of highrisk yet relatively cheap short-term private credit, on offer from financial speculators in search of higher yields on their investments than available to them in the near-zero interest monetary policy environment of their advanced home countries. This ‘push factor’, and the volatility of private capital inflows in combination with wide open capital accounts, has affected developing countries whether or not they had so-called strong economic fundamentals, such as relatively low public debt, small budget deficits, low inflation rates and high reserve holdings.

An essential ‘pull factor’ leading developing countries to borrow at high risk in international financial markets was their dwindling access to concessional multilateral finance and a shift of Official Development Assistance (ODA) away from central budget support towards wider goals, such as climate change mitigation, migration management, good governance and post-conflict support, oftentimes determined by donor interests. As a result, developing countries have seen a rapid build-up in private sector indebtedness, in particular since the Global Financial Crisis of 2008-09, accounting for 139 per cent of their combined GDP at end-2018 (see Figure 1).

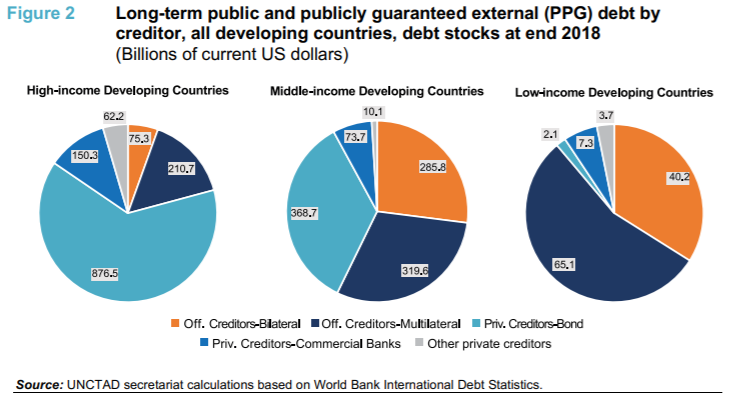

This trend has been most pronounced in high-income developing countries with relatively deeper domestic financial and banking sectors but has also and substantively affected middle- and low-income developing economies. It represents the largest contingent liability on public balance sheet in the event of a full-blown debt and financial crisis, not least in the shape of fledgling public-private partnerships, widely promoted throughout the developing world, but that may now quickly unravel in the wake of ‘sudden stops’ to their refinancing due to the Covid-19 crisis. The fragility of developing country debt positions prior to the Covid-19 crisis was further increased by concomitant changes to the ownership and currency-denomination of their private and public debt. Thus, domestic bond markets were increasingly penetrated by non-resident investors and sovereign external debt held to a much larger extent than in previous episodes of developing country debt distress by private rather than official creditors, in particular in high- and middle-income developing economies (see Figure 2)

In this context, developing countries became highly vulnerable to massive but volatile flows of highrisk yet relatively cheap short-term private credit, on offer from financial speculators in search of higher yields on their investments than available to them in the near-zero interest monetary policy environment of their advanced home countries. This ‘push factor’, and the volatility of private capital inflows in combination with wide open capital accounts, has affected developing countries whether or not they had so-called strong economic fundamentals, such as relatively low public debt, small budget deficits, low inflation rates and high reserve holdings.

An essential ‘pull factor’ leading developing countries to borrow at high risk in international financial markets was their dwindling access to concessional multilateral finance and a shift of Official Development Assistance (ODA) away from central budget support towards wider goals, such as climate change mitigation, migration management, good governance and post-conflict support, oftentimes determined by donor interests. As a result, developing countries have seen a rapid build-up in private sector indebtedness, in particular since the Global Financial Crisis of 2008-09, accounting for 139 per cent of their combined GDP at end-2018 (see Figure 1).

This trend has been most pronounced in high-income developing countries with relatively deeper domestic financial and banking sectors but has also and substantively affected middle- and low-income developing economies. It represents the largest contingent liability on public balance sheet in the event of a full-blown debt and financial crisis, not least in the shape of fledgling public-private partnerships, widely promoted throughout the developing world, but that may now quickly unravel in the wake of ‘sudden stops’ to their refinancing due to the Covid-19 crisis. The fragility of developing country debt positions prior to the Covid-19 crisis was further increased by concomitant changes to the ownership and currency-denomination of their private and public debt. Thus, domestic bond markets were increasingly penetrated by non-resident investors and sovereign external debt held to a much larger extent than in previous episodes of developing country debt distress by private rather than official creditors, in particular in high- and middle-income developing economies (see Figure 2)

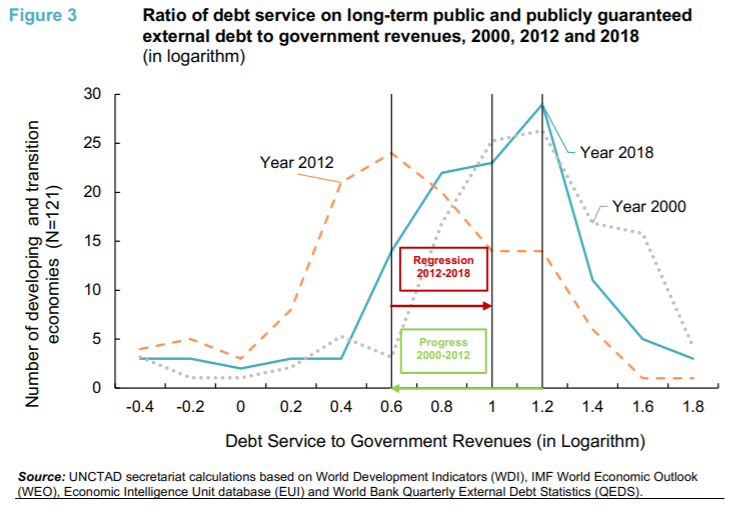

Figure 3 depicts the distribution of debt service burdens, as a share of government revenues, across developing countries in 2000, 2012 and 2018. While these had declined substantively between 2000 and 2012 (as indicated by the leftward shift of the distributions for 2000 to those for 2012 and by the fall in the distributions’ median value depicted by the green arrow), this progress has largely been reversed since then (as indicated by the rightward shift of the distributions for 2012 to those of 2018 and the by increase in these distributions’ median value depicted by the red arrow). Thus, servicing their external long-term public and publicly guaranteed debt cost developing country governments on average 6.5 per cent of their government revenues in 2012, but 10.3 per cent in 2018.

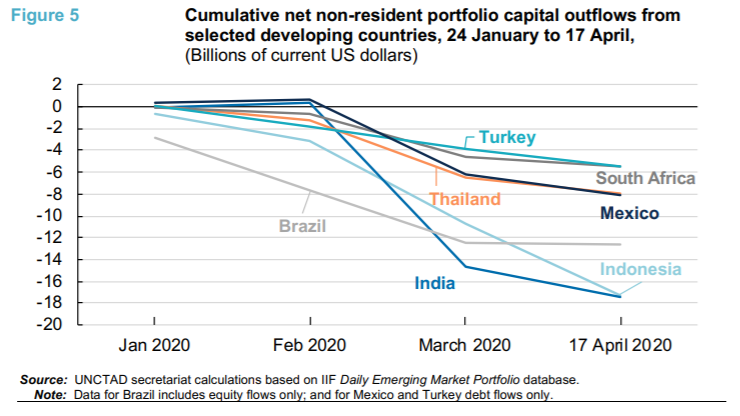

However, the situation is much more severe in many developing countries where more than a quarter of revenues are absorbed by debt servicing (Figure 4). This includes a number of oil exporters, facing a particularly difficult moment given the collapse in oil prices, as well as middle-income economies that have witnessed a sharp outflow of portfolio capital since the start of the crisis (Figure 5).