|

Related Topics |

|

We take a look at the latest monetary policy statement released by the South African Reserve Bank (SARB) in which they announced they are reducing the REPO rate by a further 25 basis point and revising down the economic growth rate of South Africa even more due to the Covid-19 pandemic.

|

|

The monetary policy committee statement released by the SARB

Since the May meeting of the Monetary Policy Committee (MPC), the Covid-19 pandemic continues to spread globally, with wide-ranging and deep social and economic effects. Current forecasts from the IMF show global Gross Domestic Product (GDP) contracting by about 4.9% this year. 1 The deepest contractions are expected in the second quarter of 2020, with gradual recoveries in the third and fourth quarters of the year. The strength of the global economic recovery will depend in part on the control of new virus outbreaks, the extent of supply and demand losses, and expectations of future growth in investment and productivity. The crisis has caused extreme volatility in financial asset prices with sharp and deep market sell-offs followed by a partial recovery. Investor appetite has generally improved, reflected in a weaker USD and stronger capital flows to emerging markets. The general environment continues to reflect pronounced levels of risk aversion, however, due to uncertainty about future global economic prospects. Policy responses to the crisis have generally been robust. This week the European Union agreed to a large, targeted stimulus package primarily to support investment. Other monetary and fiscal authorities continue to provide accommodation and support. Emerging and developing economies are generally constrained by less policy space, currency risk, and tight global financial conditions. The International Financial Institutions (IFIs) continue to make available extraordinary levels of emergency financial support to respond to the pandemic. 2 The Covid-19 outbreak has major health, social and economic impacts, presenting challenges in forecasting domestic and global economic activity. The compilation of accurate economic statistics will also remain severely challenged. Our second quarter estimate for output has been revised lower. The Bank currently expects GDP in 2020 to contract by 7.3%, compared to the 7.0% contraction forecast in May. Even as the lockdown is relaxed in coming months, for the year as a whole, investment, exports and imports are expected to decline sharply. Job losses are also expected to rise further.

Easing of the lockdown has supported growth in recent weeks and high frequency activity indicators show a pickup in spending from extremely low levels. However, getting back to pre-pandemic activity levels will take time. GDP is expected to grow by 3.7% in 2021 and by 2.8% in 2022.3 South Africa’s terms of trade and commodity export prices remain high. While oil prices are generally low, they have increased since the May meeting. The Brent crude oil price is expected to average about $40 per barrel in 2020, rising to $45 per barrel in 2021 and $50 per barrel in 2022. Exceptionally accommodative policies and the relaxation of lockdowns in many advanced economies have supported a partial recovery in global financial markets. However, financing conditions for emerging markets remain uncertain, contributing to currency weakness. The rand has depreciated by 15.2% against the USD since January and appreciated by 8.8% since the May meeting of the MPC. The implied starting point for the rand forecast is R17.93 to the US dollar, compared with R18.40 at the time of the previous meeting. Resident investors have increased purchases of long-term bonds, helping to ease yields in recent weeks. However, the yield curve is exceptionally steep, reflecting credit risk associated with high public borrowing needs.4 The Bank’s headline consumer price inflation forecast averages 3.4% in 2020 and is marginally lower than previously forecast at 4.3% in 2021 and 2022. The forecast for core inflation is lower at 3.3% in 2020, and remains broadly stable at 3.9% in 2021, and 4.1% in 2022. The overall risks to the inflation outlook at this time appear to be balanced. Global producer price and food inflation appear to have bottomed out.

Local food price inflation is expected to stay contained. Risks to inflation from currency depreciation are expected to be muted while pass-through remains low. However, electricity and other administered prices continue to be a concern. Upside risks to inflation could also emerge from heightened fiscal risks and sharp reductions in the supply of goods and services. Expectations of future inflation continued to soften for this year but are broadly stable around the mid-point of the target band for 2021. Market-based expectations for short and medium-term inflation have eased slightly, while long-term inflation expectations are higher. 5 Despite sustained higher levels of country financing risk, the Committee notes that the economic contraction and slow recovery will keep inflation well below the midpoint of the target range for this year. Barring risks outlined earlier, inflation is expected to be well contained over the medium-term, remaining close to the midpoint in 2021 and 2022.

Easing of the lockdown has supported growth in recent weeks and high frequency activity indicators show a pickup in spending from extremely low levels. However, getting back to pre-pandemic activity levels will take time. GDP is expected to grow by 3.7% in 2021 and by 2.8% in 2022.3 South Africa’s terms of trade and commodity export prices remain high. While oil prices are generally low, they have increased since the May meeting. The Brent crude oil price is expected to average about $40 per barrel in 2020, rising to $45 per barrel in 2021 and $50 per barrel in 2022. Exceptionally accommodative policies and the relaxation of lockdowns in many advanced economies have supported a partial recovery in global financial markets. However, financing conditions for emerging markets remain uncertain, contributing to currency weakness. The rand has depreciated by 15.2% against the USD since January and appreciated by 8.8% since the May meeting of the MPC. The implied starting point for the rand forecast is R17.93 to the US dollar, compared with R18.40 at the time of the previous meeting. Resident investors have increased purchases of long-term bonds, helping to ease yields in recent weeks. However, the yield curve is exceptionally steep, reflecting credit risk associated with high public borrowing needs.4 The Bank’s headline consumer price inflation forecast averages 3.4% in 2020 and is marginally lower than previously forecast at 4.3% in 2021 and 2022. The forecast for core inflation is lower at 3.3% in 2020, and remains broadly stable at 3.9% in 2021, and 4.1% in 2022. The overall risks to the inflation outlook at this time appear to be balanced. Global producer price and food inflation appear to have bottomed out.

Local food price inflation is expected to stay contained. Risks to inflation from currency depreciation are expected to be muted while pass-through remains low. However, electricity and other administered prices continue to be a concern. Upside risks to inflation could also emerge from heightened fiscal risks and sharp reductions in the supply of goods and services. Expectations of future inflation continued to soften for this year but are broadly stable around the mid-point of the target band for 2021. Market-based expectations for short and medium-term inflation have eased slightly, while long-term inflation expectations are higher. 5 Despite sustained higher levels of country financing risk, the Committee notes that the economic contraction and slow recovery will keep inflation well below the midpoint of the target range for this year. Barring risks outlined earlier, inflation is expected to be well contained over the medium-term, remaining close to the midpoint in 2021 and 2022.

Against this backdrop, the MPC decided to cut the repo rate by 25 basis points, taking it to 3.50% per annum, with effect from 24 July 2020. Three members preferred a cut of 25 basis points and two preferred to keep rates on hold. The implied path of policy rates over the forecast period generated by the Quarterly Projection Model indicates one repo rate cut of 25 basis points in the fourth quarter of 2020, remaining unchanged in the first quarter of 2021. Monetary policy can ease financial conditions and improve the resilience of households and firms to the economic implications of Covid-19. In addition to continued easing of interest rates, the SARB has relaxed regulatory requirements on banks and has taken important steps to ensure adequate liquidity in domestic markets. These actions are intended to free up more capital for lending by financial institutions to households and firms. As indicated previously, monetary policy cannot on its own improve the potential growth rate of the economy or reduce fiscal risks. These should be addressed by implementing prudent macroeconomic policies and structural reforms that lower costs generally, and increase investment opportunities, potential growth and job creation. Such steps will enhance the effectiveness of monetary policy and its transmission to the broader economy. Global economic and financial conditions are expected to remain volatile for the foreseeable future. In this highly uncertain environment, future decisions will continue to be data dependent and sensitive to the balance of risks to the outlook. The MPC will seek to look through temporary price shocks and focus on second round effects. As usual, the repo rate projection from the QPM remains a broad policy guide, changing from meeting to meeting in response to new data and risks.

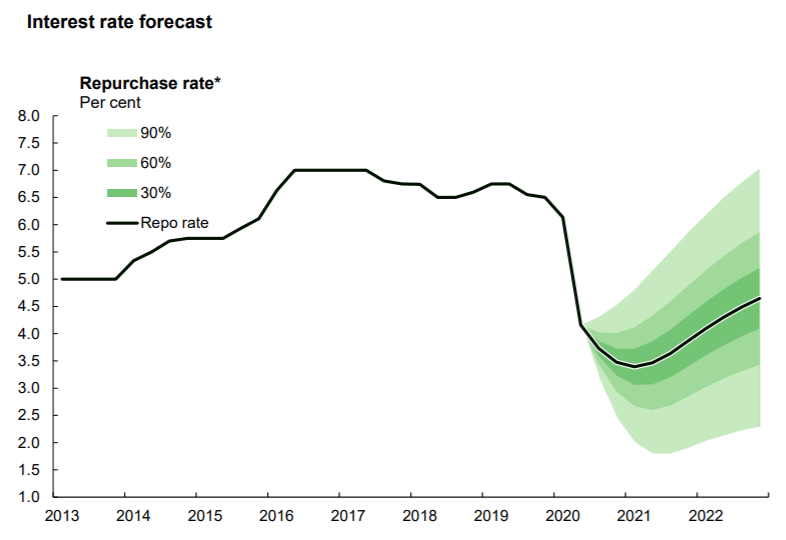

REPO fan chart

The fan chart below shows the South African Reserve Bank (SARB) projection of where they see the Repurchase rate being over the last 2 years. According to this projection the REPO wont be at its lowest level for too long as its predicting the REPO rate back up at least 100 basis points from its current level.

REPO fan chart published by the South African Reserve Bank (SARB)