|

Related Topics |

|

We take a look at a number of graphics and charts published by the South African Reserve Bank (SARB) in their monetary policy review document. It makes for interesting reading and points to SARB expecting higher interest rates in the next two years.

|

|

So SARB predicting higher interest rates in the next two years?

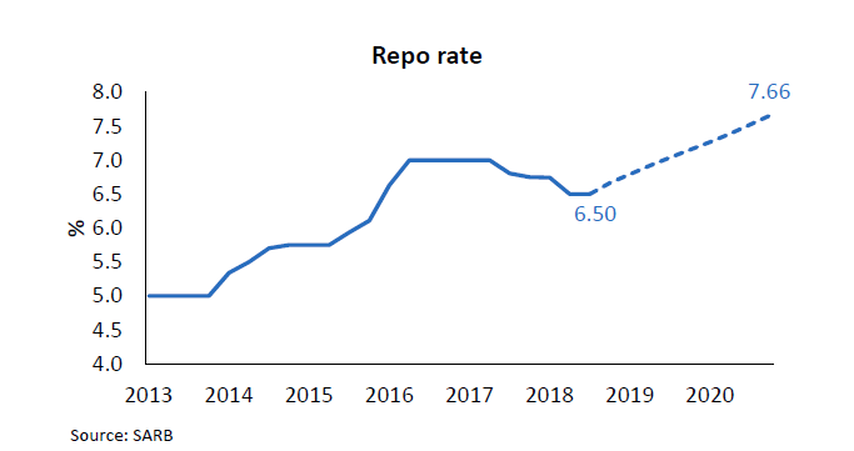

We would be very cautious in believing any of the forecasts that comes from the South African Reserve Bank. Over the years they have been hopelessly out of form with predicting the inflation rate, as their regular MPC updated inflation forecasts show. Constant revisions up and down are made as the latest information becomes available. Usually their two year forecasts of where inflation is expected to be is far off from where it actually ends up being. So SARB's forecasting should be taken with a pinch of salt. But in saying that the image below shows the SARB's prediction of the REPO rate for the next couple of years. The REPO rate is the rate at which banks borrow from the Reserve Bank. They then add another 350 basis points to the REPO rate and call this the "Prime" lending rate. Prime lending rate is given to those consumers with outstanding credit scores and can easily finance requested debt.

South African Reserve Bank (SARB) REPO rate forecast past 2020

The current REPO rate is sitting at 6.5%, with SARB predicting it will average 7.66% by the end of 2021 it looks like. That is a 17.9% increase in the REPO rate over the next two to three years. South Africans should be very worried about this, as the cost of their outstanding debt is likely to go up by a very similar percentage. So assuming a home loan of R1 000 000, was granted at Prime of 10.5% and paid off over 240 months, the consumer would pay about R9 650 a month on the bond. Should the SARB raise the REPO rate and it settles at 7.66% as predicted by SARB, that same mortgage bond will now cost R10 430 a month. An increase of R780 a month. Now add a few cars, or a investment property into the mix, or a more expensive property into the equation and its clear to see that South Africans will come under immense financial pressure should interest rates reach the levels predicted by the South African Reserve Bank. So why is SARB predicting higher interest rates. Well it stems from the fact that they expect inflation to be at higher levels than what they want it to be. SARB's target rate for inflation is between 3% and 6%. So lets say their ideal inflation rate is 4.5%.

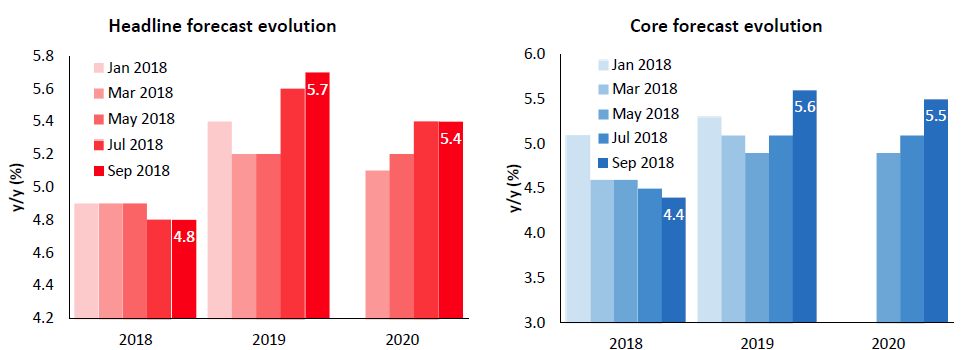

The image below shows SARB forecast for headline inflation (the official inflation rate of South Africa) as well as a "Core" inflation rate. This is an inflation rate in which volatile items such as fuel and electricity prices are excluded from the inflation numbers to give a better picture of the underlying nature of inflation.

The image below shows SARB forecast for headline inflation (the official inflation rate of South Africa) as well as a "Core" inflation rate. This is an inflation rate in which volatile items such as fuel and electricity prices are excluded from the inflation numbers to give a better picture of the underlying nature of inflation.

South African Reserve Bank Headline and Core inflation forecasts up to 2020

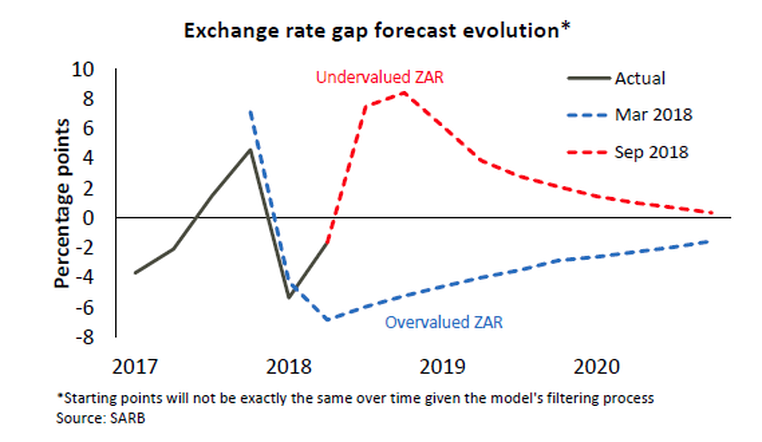

So the predicted headline inflation rate for 2018 is sitting at 4.8% for 2018, rising in 2019 to 5.7% and then declining a bit again in 2020 to 5.4%. While these rates are well within the 3% to 6% inflation target of the bank, it is a way off from the "mid point" level of 4.5%, which we believe is the bank's ideal inflation rate. So why the increase in the forecasted inflation for 2019 and 2020? The SARB believes that the weakening exchange rate will add inflationary pressures to local inflation as imported goods become more expensive, pushing up the prices of goods sold locally. The graphic below shows what SARB believes to be the exchange rate gap and its potential impact in 2019 before tapering off towards 2020.

Exchange Rate Gap as estimated by the South African Reserve Bank (SARB)

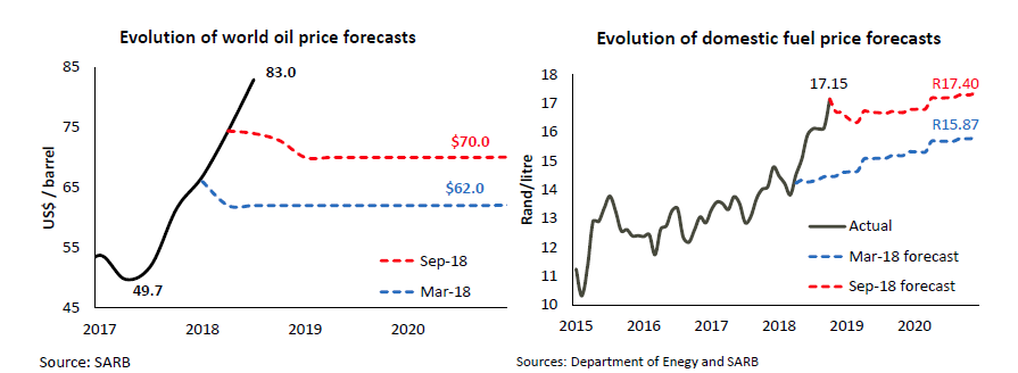

While there might be some merit to the exchange rate weakening leading to higher import prices and thus higher local inflation, we believe the higher world oil prices combined with a weaker exchange rate is the biggest cause for concern regarding local inflation. As this lead to higher fuel prices, which leads to higher input costs for farmers, producers, manufacturers, transporters, and eventually prices consumers pay for goods that were produced, manufactured and transported to retail outlets. The image below shows the evolution of South African fuel prices over the last couple of years, and just how much SARB's forecast of domestic fuel prices changed from March 2018 to September 2018, due to strong oil prices and the weak exchange rate.

South African Reserve Bank (SARB) forecast of world oil prices and South African fuel prices

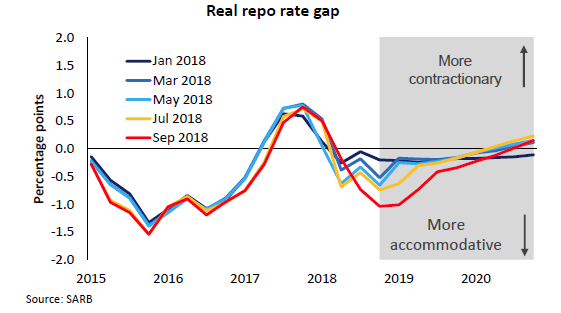

What is interesting to note about the image above is the fact that the SARB is predicting an average oil price of $70 a barrel over the next 3 years. So imagine of oil prices blow out above $100 again, SARB's inflation expectations will shoot through the roof and interest rates would end up a lot higher than the 7.66% predicted as shown in one of the earlier images. Our advice for South Africans would therefore be to be very careful in taking on any new debt, especially to finance nice to haves such as cars. Rather stick to taking on debt to buy assets such as houses. And lastly we show an image from the SARB in which they show that over the last couple of months there has been a clear change in the stance of the South African Reserve Bank from a more accommodative monetary policy to a more contractionary policy

The above is the opposite of what South Africa's economy needs right now. Just showing once again that South Africa's monetary fiscal policy mix is working against one another and limits the potential growth South Africa's economy can and must reach (at this point to reduce massive levels of unemployment. South Africans will be under severe pressure over the next couple of years, and with consumers making up a large part of South Africa's economic growth over the last couple of years, we have little hope of consumers driving economic growth over the next couple of years, as higher fuel prices, higher inflation and higher interest rates starts to take hold of ordinary South Africans wallet. Our advice, reduce debt, reduce unneccesary spending and start saving more to get through the tough times ahead.