|

Related Topics |

|

We take a look at the performance of MulitChoice (MCG) shares since its listing debut on the JSE earlier in the year as well as announcements from the group that a few large local asset management firms owns more than 20% of MultiChoice's shares.

|

|

Background on MultiChoice

MULTICHOICE

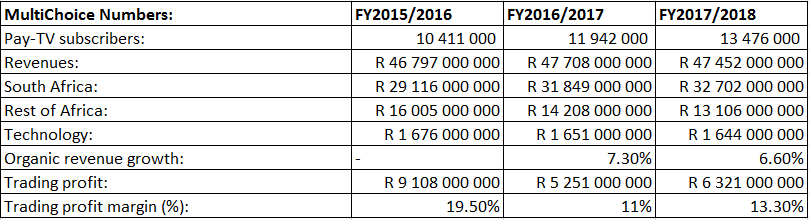

MultiChoice, its subsidiaries, affiliates and associates ("MultiChoice Group") is one of the leading video entertainment operators on the African continent, and one of the fastest growing pay-TV broadcast providers globally, entertaining 13.9 million households (as at 30 September 2018) across 50 countries. Its carefully curated local and international content is distributed across multiple platforms, including digital satellite and terrestrial television, as well as through OTT solutions. The MultiChoice Group is structured around the following three business segments: - South Africa, the MultiChoice Group's division that offers digital satellite television and subscription video-on-demand services to 7.2 million subscribers in South Africa (as at 30 September 2018). Connected Video, which forms part of the South Africa segment from a financial reporting standpoint, delivers online video entertainment services to subscribers; - Rest of Africa, the MultiChoice Group's division which offers digital satellite, online services and digital terrestrial television services to 6.7 million subscribers across Africa (as at 30 September 2018); and - Technology, which includes the MultiChoice Group's leading digital platform and application security division, Irdeto.

MultiChoice, its subsidiaries, affiliates and associates ("MultiChoice Group") is one of the leading video entertainment operators on the African continent, and one of the fastest growing pay-TV broadcast providers globally, entertaining 13.9 million households (as at 30 September 2018) across 50 countries. Its carefully curated local and international content is distributed across multiple platforms, including digital satellite and terrestrial television, as well as through OTT solutions. The MultiChoice Group is structured around the following three business segments: - South Africa, the MultiChoice Group's division that offers digital satellite television and subscription video-on-demand services to 7.2 million subscribers in South Africa (as at 30 September 2018). Connected Video, which forms part of the South Africa segment from a financial reporting standpoint, delivers online video entertainment services to subscribers; - Rest of Africa, the MultiChoice Group's division which offers digital satellite, online services and digital terrestrial television services to 6.7 million subscribers across Africa (as at 30 September 2018); and - Technology, which includes the MultiChoice Group's leading digital platform and application security division, Irdeto.

On 27 February 2019 we had the following to say regarding a potention valuation of MultiChoice shares by the market once it lists.

"So while MultiChoice has seen strong subscriber numbers growth over the last three years, infact 29.4%, while revenue over the same period only grew by 1.4%. Their trading profit margins are in decline too. But looking at the number of shares MultiChoice plans on issuing, their trading profits and placing a PE ratio of 15 on MultiChoice shares, it will give the company a valuation of R94.8 billion (which will make MultiChoice the 21st largest firm listed on the JSE) or around R211 a share

Note we do not think that MultiChoice will trade at a PE of 15. We merely used it as a benchmark PE ratio as it is close to the overall market average. We believe in the long run MultiChoice group will trade at a PE of around 8, due to the struggling segment they are operating in. Competition from online pay per view companies such as Netflix eating into their subscriber base. At a PE of 8 we see them trading at around R112 a share.

But dont be surprised if on listing the price surges as large funds tracking the Top 40 (and dont have a lot of exposure in NPN) needs to buy the share to have it in their funds. A gradual decline after the feeding frenzy mayhem of listing will then probably set in and MCG we predict will be trading at a PE of around 7/8 a few months after listing."

So where are MCG shares trading at right now after a few months of trading on the Johannesburg Stock Exchange? The screenshot below, taken from Sharenet shows that its been a pretty positive period for the group since it's listing on the JSE.

"So while MultiChoice has seen strong subscriber numbers growth over the last three years, infact 29.4%, while revenue over the same period only grew by 1.4%. Their trading profit margins are in decline too. But looking at the number of shares MultiChoice plans on issuing, their trading profits and placing a PE ratio of 15 on MultiChoice shares, it will give the company a valuation of R94.8 billion (which will make MultiChoice the 21st largest firm listed on the JSE) or around R211 a share

Note we do not think that MultiChoice will trade at a PE of 15. We merely used it as a benchmark PE ratio as it is close to the overall market average. We believe in the long run MultiChoice group will trade at a PE of around 8, due to the struggling segment they are operating in. Competition from online pay per view companies such as Netflix eating into their subscriber base. At a PE of 8 we see them trading at around R112 a share.

But dont be surprised if on listing the price surges as large funds tracking the Top 40 (and dont have a lot of exposure in NPN) needs to buy the share to have it in their funds. A gradual decline after the feeding frenzy mayhem of listing will then probably set in and MCG we predict will be trading at a PE of around 7/8 a few months after listing."

So where are MCG shares trading at right now after a few months of trading on the Johannesburg Stock Exchange? The screenshot below, taken from Sharenet shows that its been a pretty positive period for the group since it's listing on the JSE.

The summary below shows the performance of MultiChoice (MCG) shares over various time periods since its listing at the end of February 2019.

- 1 week: 1.11%

- 1 month: 7.71%

- Month to date (MTD): 9.48%

- Year to date (YTD): 25.88%

MultiChoice (MCG) warns of loss for the full year of around R8 a share

Earlier in the month MCG released the following trading update in which it warned investors that it will be making around R8 loss per share in their financial results it will be releasing.

Trading statement

Shareholders are advised that the MultiChoice group ("the group") is finalising its consolidated annual financial statements for the twelve months ended 31 March 2019 ("current period"). Core headline earnings per share and trading profit Shareholders are reminded that the board considers core headline earnings per share and trading profit as the two most appropriate indicators of the operating performance of the group, as they adjust for non-recurring and non- operational items.

Compared to the group´s results for the twelve months ended 31 March 2018 ("prior year") included within the pre- listing statement, the group expects core headline earnings per share for the current period to be between 8% (30 ZAR cents) and 12% (45 ZAR cents) higher than the prior year´s reported 374 ZAR cents.

Trading profit is expected to be between 9% (R0.6bn) and 13% (R0.8bn) higher than the prior year´s reported R6,3bn. On an organic basis (i.e. reflecting results on a constant currency basis, excluding any M&A) trading profit is expected to be between 24% (R1.5bn) and 30% (R1.9bn) higher than the prior year’s reported R6,3bn. The improved financial performance expected for the current period is mainly driven by solid subscriber growth and a reduction in losses in the Rest of Africa segment. As explained in the pre-listing statement, core headline earnings per share and organic trading profit constitute pro forma financial information in terms of the JSE Listings Requirements.

The pro forma financial information is the responsibility of the group's directors, has been prepared for illustrative purposes only, and may not fairly present the group’s financial position, changes in equity, cash flows or results of operations. Core headline earnings is calculated by adjusting headline earnings for the following items, net of tax and non-controlling interests: a) amortisation of intangible assets arising from business combinations; b) accounting adjustments stemming from IFRS 3: Business Combinations; c) equity-settled share-based payment compensation; d) unrealised foreign currency gains/losses; e) certain fair-value adjustments under IFRS; and f) non-recurring current and deferred taxation impacts. Organic trading profit is calculated by excluding foreign currency movements and changes in the composition of the group. Loss per share and headline loss per share Compared to the prior year, the group expects loss per share for the current period to be between 673 ZAR cents and 739 ZAR cents lower than the prior year´s reported earnings per share of 332 ZAR cents.

Headline loss per share for the current period is expected to be between 724 ZAR cents and 800 ZAR cents lower than the prior year´s reported headline earnings per share of 410 ZAR cents. The key reasons for the movements above are set out below:

a) As disclosed in annex 7 of the pre-listing statement, the group had to account for the impact of allocating for no consideration a 5% stake in MultiChoice South Africa Holdings (Pty) Ltd to Phuthuma Nathi Investments 1 and Phuthuma Nathi Investments 2 as part of the unbundling process. As a result, loss per share and headline loss per share were impacted significantly by the once-off equity-settled share-based compensation charge recognised on what was an effective disposal of 5% of the group´s interest in MultiChoice South Africa Holdings (Pty) Ltd. While the impact of this transaction is removed from core headline earnings per share and trading profit, it is included in both loss per share and headline loss per share. This is expected to reduce earnings per share and headline earnings per share by 438 ZAR cents.

b) Furthermore, the impact of the depreciation of SA Rand against the US dollar has led to an increase in unrealised foreign exchange losses on translation of the group’s US dollar denominated transponder lease liabilities. This is expected to reduce earnings per share and headline earnings per share by 263 ZAR cents.

Further details will be provided in the consolidated provisional annual results, due to be released on SENS on 18 June 2019. The financial information on which this trading statement is based has not been reviewed and reported on by the Company´s external auditor.

End SENS

But looking at the share price performance of the group it seems that MCG shareholders took the news of the loss per share in their stride as the stock is still continuing its upwards trend. Part of the reason for this is probably the fact that MCG has a few large shareholders in it for the long run. One that comes to mind is Coronation Asset Management, which owns over 5% of MultiChoice's shares.

Below the SENS released by MultiChoice on 29 April 2019 in which it informed the markets that Coronation owns more than 5% of their issued shares.

Start SENS

In accordance with section 122(3)(b) of the Companies Act, 71 of 2008 ("the Act"), and section 3.83(b) of the JSE Limited Listings Requirements ("Listings Requirements"), holders of ordinary shares in the Company are advised that the Company has received a formal notification in terms of Section 122(1) of the Act from Coronation Asset Management (Pty) Ltd that the clients of Coronation Group ("Coronation") have, in aggregate, acquired an interest in the ordinary shares of the Company, such that the total interest in the ordinary shares of the Company held by Coronation clients now amounts to 5.30% of the total issued ordinary shares of the Company.

End SENS

So Coronation is a pretty big shareholder in MultiChoice. But a SENS announcement the day before the release of the SENS above highlighted two even bigger shareholders in MultiChoice. The SENS on 28 April 2019 informed the markets that Allan Gray Fund Managers owns more than 10% of the group's shares, and Prudential Asset Management owns more than 5.3% of the group's shares. See the SENS below

Start SENS

In accordance with section 122(3)(b) of the Companies Act, 71 of 2008 ("the Act"), and section 3.83(b) of the JSE Limited Listings Requirements ("Listings Requirements"), holders of ordinary shares in the Company are advised that the Company has received formal notifications in terms of Section 122(1) of the Act that the clients of:

1. Prudential Investment Managers (South Africa) (Pty) Ltd ("Prudential") have, in aggregate, acquired an interest in the ordinary shares of the Company, such that the total interest in the ordinary shares of the Company held by Prudential's clients now amounts to 5.37% of the total issued ordinary shares of the Company;

and

2. Allan Gray (Pty) Ltd ("Allan Gray") have, in aggregate, acquired an interest in the ordinary shares of the Company, such that the total interest in the ordinary shares of the Company held by Allan Gray's clients now amounts to 10.0774% of the total issued ordinary shares of the Company.

End SENS

So why would small time investors panic and sell their MCG shares when they say see big well known asset managers such as Allan Gray, Prudential and Coronation holding over 20% of MultiChoice's shares listed? If they see value in their shares then surely small retail investors can assume their is value to be had in holding their shares. Why else would large asset managers acquire such large percentages of MultiChoice shares?

Trading statement

Shareholders are advised that the MultiChoice group ("the group") is finalising its consolidated annual financial statements for the twelve months ended 31 March 2019 ("current period"). Core headline earnings per share and trading profit Shareholders are reminded that the board considers core headline earnings per share and trading profit as the two most appropriate indicators of the operating performance of the group, as they adjust for non-recurring and non- operational items.

Compared to the group´s results for the twelve months ended 31 March 2018 ("prior year") included within the pre- listing statement, the group expects core headline earnings per share for the current period to be between 8% (30 ZAR cents) and 12% (45 ZAR cents) higher than the prior year´s reported 374 ZAR cents.

Trading profit is expected to be between 9% (R0.6bn) and 13% (R0.8bn) higher than the prior year´s reported R6,3bn. On an organic basis (i.e. reflecting results on a constant currency basis, excluding any M&A) trading profit is expected to be between 24% (R1.5bn) and 30% (R1.9bn) higher than the prior year’s reported R6,3bn. The improved financial performance expected for the current period is mainly driven by solid subscriber growth and a reduction in losses in the Rest of Africa segment. As explained in the pre-listing statement, core headline earnings per share and organic trading profit constitute pro forma financial information in terms of the JSE Listings Requirements.

The pro forma financial information is the responsibility of the group's directors, has been prepared for illustrative purposes only, and may not fairly present the group’s financial position, changes in equity, cash flows or results of operations. Core headline earnings is calculated by adjusting headline earnings for the following items, net of tax and non-controlling interests: a) amortisation of intangible assets arising from business combinations; b) accounting adjustments stemming from IFRS 3: Business Combinations; c) equity-settled share-based payment compensation; d) unrealised foreign currency gains/losses; e) certain fair-value adjustments under IFRS; and f) non-recurring current and deferred taxation impacts. Organic trading profit is calculated by excluding foreign currency movements and changes in the composition of the group. Loss per share and headline loss per share Compared to the prior year, the group expects loss per share for the current period to be between 673 ZAR cents and 739 ZAR cents lower than the prior year´s reported earnings per share of 332 ZAR cents.

Headline loss per share for the current period is expected to be between 724 ZAR cents and 800 ZAR cents lower than the prior year´s reported headline earnings per share of 410 ZAR cents. The key reasons for the movements above are set out below:

a) As disclosed in annex 7 of the pre-listing statement, the group had to account for the impact of allocating for no consideration a 5% stake in MultiChoice South Africa Holdings (Pty) Ltd to Phuthuma Nathi Investments 1 and Phuthuma Nathi Investments 2 as part of the unbundling process. As a result, loss per share and headline loss per share were impacted significantly by the once-off equity-settled share-based compensation charge recognised on what was an effective disposal of 5% of the group´s interest in MultiChoice South Africa Holdings (Pty) Ltd. While the impact of this transaction is removed from core headline earnings per share and trading profit, it is included in both loss per share and headline loss per share. This is expected to reduce earnings per share and headline earnings per share by 438 ZAR cents.

b) Furthermore, the impact of the depreciation of SA Rand against the US dollar has led to an increase in unrealised foreign exchange losses on translation of the group’s US dollar denominated transponder lease liabilities. This is expected to reduce earnings per share and headline earnings per share by 263 ZAR cents.

Further details will be provided in the consolidated provisional annual results, due to be released on SENS on 18 June 2019. The financial information on which this trading statement is based has not been reviewed and reported on by the Company´s external auditor.

End SENS

But looking at the share price performance of the group it seems that MCG shareholders took the news of the loss per share in their stride as the stock is still continuing its upwards trend. Part of the reason for this is probably the fact that MCG has a few large shareholders in it for the long run. One that comes to mind is Coronation Asset Management, which owns over 5% of MultiChoice's shares.

Below the SENS released by MultiChoice on 29 April 2019 in which it informed the markets that Coronation owns more than 5% of their issued shares.

Start SENS

In accordance with section 122(3)(b) of the Companies Act, 71 of 2008 ("the Act"), and section 3.83(b) of the JSE Limited Listings Requirements ("Listings Requirements"), holders of ordinary shares in the Company are advised that the Company has received a formal notification in terms of Section 122(1) of the Act from Coronation Asset Management (Pty) Ltd that the clients of Coronation Group ("Coronation") have, in aggregate, acquired an interest in the ordinary shares of the Company, such that the total interest in the ordinary shares of the Company held by Coronation clients now amounts to 5.30% of the total issued ordinary shares of the Company.

End SENS

So Coronation is a pretty big shareholder in MultiChoice. But a SENS announcement the day before the release of the SENS above highlighted two even bigger shareholders in MultiChoice. The SENS on 28 April 2019 informed the markets that Allan Gray Fund Managers owns more than 10% of the group's shares, and Prudential Asset Management owns more than 5.3% of the group's shares. See the SENS below

Start SENS

In accordance with section 122(3)(b) of the Companies Act, 71 of 2008 ("the Act"), and section 3.83(b) of the JSE Limited Listings Requirements ("Listings Requirements"), holders of ordinary shares in the Company are advised that the Company has received formal notifications in terms of Section 122(1) of the Act that the clients of:

1. Prudential Investment Managers (South Africa) (Pty) Ltd ("Prudential") have, in aggregate, acquired an interest in the ordinary shares of the Company, such that the total interest in the ordinary shares of the Company held by Prudential's clients now amounts to 5.37% of the total issued ordinary shares of the Company;

and

2. Allan Gray (Pty) Ltd ("Allan Gray") have, in aggregate, acquired an interest in the ordinary shares of the Company, such that the total interest in the ordinary shares of the Company held by Allan Gray's clients now amounts to 10.0774% of the total issued ordinary shares of the Company.

End SENS

So why would small time investors panic and sell their MCG shares when they say see big well known asset managers such as Allan Gray, Prudential and Coronation holding over 20% of MultiChoice's shares listed? If they see value in their shares then surely small retail investors can assume their is value to be had in holding their shares. Why else would large asset managers acquire such large percentages of MultiChoice shares?