|

Related Topics |

|

We take a look at the financial results released by Kumba Iron Ore (KIO) this morning in which it announced bumper profits and a massive dividend payout. The bumper profits is largely due to sharp increases in iron ore prices, which shot up after a holding dam of Vale a large iron ore producer broke its wall and flooded a town which lead to Vale closing the mine for a period of time. This has limited supply which lead to strong price increases

|

|

About Kumba Iron Ore

Kumba is a mining group of companies focusing on the exploration, extraction, beneficiation, marketing and sale and shipping of iron ore. Kumba produces iron ore in South Africa at Sishen and Kolomela mines in the Northern Cape province. It is part of the AngloAmerican mining group.

Sishen mine, is near the town of Kathu in the Northern Cape Province. Sishen is our flagship operation and one of the largest open pit mines in the world – some 14km long. Sishen mine has sufficient reserves to sustain a 19-year life of mine. The bulk of our iron ore production comes from Sishen mine, with most of it being exported. We mine by opencast methods and then transport the ore to the beneficiation plant where it is crushed, screened and beneficiated. We beneficiate our products through dense media separation and jig technology. The jig plant at Sishen mine is the largest of its type in the world. At Sishen we produce iron ore products which meet different specifications, according to our customers’ needs.

Kolomela mine, is near Postmasburg in the Northern Cape Province. Kolomela is our newest mining operation, having been completed at the end of 2011. Its name means ‘to dig deeper’ or ‘to persevere’. Kolomela has a life of mine of 25 years. Our team members at Kolomela mine have done an excellent job of ramping up the mine and sustaining its production over the last few years. Our Kolomela lump iron ore is in demand because of its excellent physical strength and high iron content.

Sishen mine, is near the town of Kathu in the Northern Cape Province. Sishen is our flagship operation and one of the largest open pit mines in the world – some 14km long. Sishen mine has sufficient reserves to sustain a 19-year life of mine. The bulk of our iron ore production comes from Sishen mine, with most of it being exported. We mine by opencast methods and then transport the ore to the beneficiation plant where it is crushed, screened and beneficiated. We beneficiate our products through dense media separation and jig technology. The jig plant at Sishen mine is the largest of its type in the world. At Sishen we produce iron ore products which meet different specifications, according to our customers’ needs.

Kolomela mine, is near Postmasburg in the Northern Cape Province. Kolomela is our newest mining operation, having been completed at the end of 2011. Its name means ‘to dig deeper’ or ‘to persevere’. Kolomela has a life of mine of 25 years. Our team members at Kolomela mine have done an excellent job of ramping up the mine and sustaining its production over the last few years. Our Kolomela lump iron ore is in demand because of its excellent physical strength and high iron content.

Trading Statement

Below the extracts from the financial results released by Kumbo Iron Ore today

EXTRACTS FROM THE REVIEWED INTERIM RESULTS FOR THE PERIOD ENDED 30 JUNE 2019 AND INTERIM CASH DIVIDEND DECLARATION

- Fatality free since May 2016 - EBITDA margin up 22 percentage points to 58%

- Strong balance sheet with net cash of R18.8 billion - Average realised export price up 57% to US$108/tonne

- Headline earnings up 239% to R10.1 billion or R31.51 per share

- Interim cash dividend of R30.79 per share

OVERVIEW

Themba Mkhwanazi, Chief Executive of Kumba Iron Ore, said, “Kumba delivered an exceptional financial performance in the first half of 2019 by focusing on safe, responsible and efficient production, while achieving optimal value for our premium quality products. Most importantly, we marked three years of fatality-free mining by combining local excellence and global expertise to transform productivity and safety at Sishen and Kolomela. Our “value over volume” strategy has met customer demand and delivered a more than threefold increase in EBITDA to R20.1 billion. With a very strong opening cash position and attributable free cash flow of R12.7 billion, the Board has declared an interim cash dividend of R9.9 billion or R30.79 per share. This represents a payout ratio of 98% of headline earnings, above our target range of 50% to 75% of headline earnings. By integrating our sales and operational strategy, we achieved a 57% increase in our average realised FOB iron ore price. This reflects the strengthening of iron ore prices and quality premia, as well as the marketing and beneficiating capability of our team, which ensured that our premium product portfolio remains competitive and that we continue to create customer value. We are progressing at a pace towards our margin enhancement target of US$10/tonne.

Our operational efficiency increased to 67%, which, together with our focus on cost optimisation, delivered savings of R460 million, underpinning our EBITDA margin of 58% and our break-even price of US$32/tonne. Operationally, Kumba experienced a challenging first half which saw production volumes decreasing by 11% to 20.1 Mt largely due to unscheduled plant maintenance in Q1 2019. We have made good progress in Q2 2019 with production increasing by 12% to 10.5 Mt from the first quarter. We remain cautious and production guidance for the year was revised down to 42 Mt to 43 Mt. Pleasingly, our logistical performance has improved significantly, supporting growth in export sales of 2% and our full year sales guidance which remains at 43 Mt to 44 Mt. For the second half of the year we aim to improve our safety performance, increase production volumes and deliver on our full year R700 million cost-savings target while continuing to achieve optimal market premia. Our strategy to extend the life of our mines to over 20 years remains on track, thus providing a more sustainable future for our communities which depend on us. Our commitment to disciplined capital allocation and sustainable shareholder returns, together with our flexible and resilient balance sheet, ensures that we remain well-positioned to deliver sustainable returns.”

OPERATIONAL PERFORMANCE

Kumba experienced operational challenges in the first half, largely due to unscheduled maintenance. Total tonnes mined decreased marginally by 2% to 138 Mt (H1 2018: 140.4 Mt), while total production volumes reduced by 11% to 20.1 Mt (1H1 2018: 22.5 Mt). Good progress was made in Q2 2019, with production increasing by 12% to 10.5 Mt from the first quarter. Sishen's tonnes mined and production volumes decreased to 99.6 Mt (H1 2018: 105.1 Mt) and 13.8 Mt (H1 2018: 15.3 Mt), respectively with waste movement at 82.8 Mt (H1 2018: 86.6 Mt). At Kolomela, mining productivity continued to improve as demonstrated by the increase in total tonnes mined by 9% to 38.4 Mt, (H1 2018: 35.3 Mt), with waste stripping up 17% as planned to 30.9 Mt (H1 2018: 26.4 Mt). Total production decreased by 12% to 6.3 Mt (H1 2018: 7.2 Mt) due to the infrastructure upgrade of the dense media separation plant. Significant improvement in the logistical performance contributed to the 2% growth in export sales to 19.9 Mt (H1 2018: 19.5 Mt). Total sales volumes increased marginally to 21.4 Mt (H1 2018: 21.2 Mt).

REVENUE AND EARNINGS BEFORE INTEREST, TAX, DEPRECIATION AND AMORTISATION (EBITDA)

Total revenue increased by 77% to R34.5 billion (H1 2018: R19.5 billion), largely driven by a 57% increase in the average realised FOB iron ore price to US$108 tonne (H1 2018: US$69/tonne) and the Rand weakening by 16% on average against the US Dollar (H1 2019: R14.20/US$1 compared to H1 2018: R12.30/US$1), while total sales volumes were broadly flat at 21.4 Mt (H1 2018: 21.2 Mt). Unit cash costs at Sishen mine increased by 20% to R370/tonne (FY 2018: R290/tonne), largely attributable to lower production volumes and the utilisation of high-grade work-in-progress (WIP) stock. Kolomela mine incurred unit cash costs of R255/tonne (FY 2018: R249/tonne) as cost savings helped to partially offset cost escalation and lower production volumes. Kumba achieved an average cash break-even price of US$32/tonne (62%Fe CFR China), an improvement of US$14/tonne compared to the first half of 2018. EBITDA of R20.1 billion (H1 2018: R7 billion) reflects an increase of 189% driven by a 35% gain through higher market premia and increased sales, a 46% higher average Platts62 iron ore price and a 16% weaker currency. This increase was partly offset by higher operating expenses resulting from an increase in royalties, inflation and a net freight loss incurred on shipping operations. Overall, the EBITDA margin improved to 58% (H1 2018: 36%). Kumba achieved a net profit of R13.2 billion (H1 2018: R3.9 billion).

CASH FLOW

Cash flow generated from operations increased to R19.2 billion (H1 2018: R6.9 billion) which resulted in the group ending the period with a net cash position of R18.8 billion (H1 2018: R11.7 billion; H2 2018: R11.7 billion) after allowing for capital expenditure of R2.2 billion and the final 2018 cash dividend payment of R6.6 billion.

INTERIM CASH DIVIDEND DECLARED

In line with our capital allocation framework, the Board has declared an interim cash dividend per share of R30.79.

OUTLOOK

Looking ahead, we will continue to build on the momentum gained in the first six months of the year. Kumba's strategic objectives are clear - we are targeting a US$10/tonne margin enhancement and a 20-year life of asset. This will allow us to maximise value and shareholder returns while maintaining financial discipline. To date in 2019, we have extended our fatality-free safety performance track record, delivered strong financial results and will be paying R13 billion of cash to our shareholders in dividends. Our aim in the second half, is to further improve on our safety performance, increase production volumes and deliver on our cost-savings target of R700 million, in addition to continuing to achieve maximum market premia. We are working hard to further progress our resource development plan and the feasibility study on our UHDMS technology, which will add to the life of Sishen mine is 80% complete.

At Kolomela, we are unlocking the 85 Mt of resources under study and drilling activities are on schedule. Due to the operational challenges experienced over the first few months of the year, our full year total production guidance has been revised to 42 Mt to 43 Mt from 43 Mt to 44 Mt. Full year guidance for sales remained constant at 43 Mt to 44 Mt as we continue to optimise our integrated sales and operations planning. Sishen's production guidance has been revised to between 29 Mt and 30 Mt, while waste guidance remains unchanged at 170 Mt to 180 Mt. Due to the infrastructure upgrade of the DMS plant, we have revised Kolomela's production guidance to ~13 Mt, while waste guidance of 55 Mt to 60 Mt was maintained as previously guided. In line with the revised production guidance at Sishen, the full year unit cash cost guidance of the mine was increased to between R325/tonne and R335/tonne. Kolomela's unit cash cost guidance was revised down to between R255/tonne and R265/tonne.

Our capital expenditure for 2019, including deferred stripping, was revised slightly higher to R4.9 billion to R5.1 billion, from the previous range of R4.6 billion to R4.8 billion, due to an increase in deferred stripping and capital spares aimed at improving the performance and efficiency of our primary equipment and production plants.

EXTRACTS FROM THE REVIEWED INTERIM RESULTS FOR THE PERIOD ENDED 30 JUNE 2019 AND INTERIM CASH DIVIDEND DECLARATION

- Fatality free since May 2016 - EBITDA margin up 22 percentage points to 58%

- Strong balance sheet with net cash of R18.8 billion - Average realised export price up 57% to US$108/tonne

- Headline earnings up 239% to R10.1 billion or R31.51 per share

- Interim cash dividend of R30.79 per share

OVERVIEW

Themba Mkhwanazi, Chief Executive of Kumba Iron Ore, said, “Kumba delivered an exceptional financial performance in the first half of 2019 by focusing on safe, responsible and efficient production, while achieving optimal value for our premium quality products. Most importantly, we marked three years of fatality-free mining by combining local excellence and global expertise to transform productivity and safety at Sishen and Kolomela. Our “value over volume” strategy has met customer demand and delivered a more than threefold increase in EBITDA to R20.1 billion. With a very strong opening cash position and attributable free cash flow of R12.7 billion, the Board has declared an interim cash dividend of R9.9 billion or R30.79 per share. This represents a payout ratio of 98% of headline earnings, above our target range of 50% to 75% of headline earnings. By integrating our sales and operational strategy, we achieved a 57% increase in our average realised FOB iron ore price. This reflects the strengthening of iron ore prices and quality premia, as well as the marketing and beneficiating capability of our team, which ensured that our premium product portfolio remains competitive and that we continue to create customer value. We are progressing at a pace towards our margin enhancement target of US$10/tonne.

Our operational efficiency increased to 67%, which, together with our focus on cost optimisation, delivered savings of R460 million, underpinning our EBITDA margin of 58% and our break-even price of US$32/tonne. Operationally, Kumba experienced a challenging first half which saw production volumes decreasing by 11% to 20.1 Mt largely due to unscheduled plant maintenance in Q1 2019. We have made good progress in Q2 2019 with production increasing by 12% to 10.5 Mt from the first quarter. We remain cautious and production guidance for the year was revised down to 42 Mt to 43 Mt. Pleasingly, our logistical performance has improved significantly, supporting growth in export sales of 2% and our full year sales guidance which remains at 43 Mt to 44 Mt. For the second half of the year we aim to improve our safety performance, increase production volumes and deliver on our full year R700 million cost-savings target while continuing to achieve optimal market premia. Our strategy to extend the life of our mines to over 20 years remains on track, thus providing a more sustainable future for our communities which depend on us. Our commitment to disciplined capital allocation and sustainable shareholder returns, together with our flexible and resilient balance sheet, ensures that we remain well-positioned to deliver sustainable returns.”

OPERATIONAL PERFORMANCE

Kumba experienced operational challenges in the first half, largely due to unscheduled maintenance. Total tonnes mined decreased marginally by 2% to 138 Mt (H1 2018: 140.4 Mt), while total production volumes reduced by 11% to 20.1 Mt (1H1 2018: 22.5 Mt). Good progress was made in Q2 2019, with production increasing by 12% to 10.5 Mt from the first quarter. Sishen's tonnes mined and production volumes decreased to 99.6 Mt (H1 2018: 105.1 Mt) and 13.8 Mt (H1 2018: 15.3 Mt), respectively with waste movement at 82.8 Mt (H1 2018: 86.6 Mt). At Kolomela, mining productivity continued to improve as demonstrated by the increase in total tonnes mined by 9% to 38.4 Mt, (H1 2018: 35.3 Mt), with waste stripping up 17% as planned to 30.9 Mt (H1 2018: 26.4 Mt). Total production decreased by 12% to 6.3 Mt (H1 2018: 7.2 Mt) due to the infrastructure upgrade of the dense media separation plant. Significant improvement in the logistical performance contributed to the 2% growth in export sales to 19.9 Mt (H1 2018: 19.5 Mt). Total sales volumes increased marginally to 21.4 Mt (H1 2018: 21.2 Mt).

REVENUE AND EARNINGS BEFORE INTEREST, TAX, DEPRECIATION AND AMORTISATION (EBITDA)

Total revenue increased by 77% to R34.5 billion (H1 2018: R19.5 billion), largely driven by a 57% increase in the average realised FOB iron ore price to US$108 tonne (H1 2018: US$69/tonne) and the Rand weakening by 16% on average against the US Dollar (H1 2019: R14.20/US$1 compared to H1 2018: R12.30/US$1), while total sales volumes were broadly flat at 21.4 Mt (H1 2018: 21.2 Mt). Unit cash costs at Sishen mine increased by 20% to R370/tonne (FY 2018: R290/tonne), largely attributable to lower production volumes and the utilisation of high-grade work-in-progress (WIP) stock. Kolomela mine incurred unit cash costs of R255/tonne (FY 2018: R249/tonne) as cost savings helped to partially offset cost escalation and lower production volumes. Kumba achieved an average cash break-even price of US$32/tonne (62%Fe CFR China), an improvement of US$14/tonne compared to the first half of 2018. EBITDA of R20.1 billion (H1 2018: R7 billion) reflects an increase of 189% driven by a 35% gain through higher market premia and increased sales, a 46% higher average Platts62 iron ore price and a 16% weaker currency. This increase was partly offset by higher operating expenses resulting from an increase in royalties, inflation and a net freight loss incurred on shipping operations. Overall, the EBITDA margin improved to 58% (H1 2018: 36%). Kumba achieved a net profit of R13.2 billion (H1 2018: R3.9 billion).

CASH FLOW

Cash flow generated from operations increased to R19.2 billion (H1 2018: R6.9 billion) which resulted in the group ending the period with a net cash position of R18.8 billion (H1 2018: R11.7 billion; H2 2018: R11.7 billion) after allowing for capital expenditure of R2.2 billion and the final 2018 cash dividend payment of R6.6 billion.

INTERIM CASH DIVIDEND DECLARED

In line with our capital allocation framework, the Board has declared an interim cash dividend per share of R30.79.

OUTLOOK

Looking ahead, we will continue to build on the momentum gained in the first six months of the year. Kumba's strategic objectives are clear - we are targeting a US$10/tonne margin enhancement and a 20-year life of asset. This will allow us to maximise value and shareholder returns while maintaining financial discipline. To date in 2019, we have extended our fatality-free safety performance track record, delivered strong financial results and will be paying R13 billion of cash to our shareholders in dividends. Our aim in the second half, is to further improve on our safety performance, increase production volumes and deliver on our cost-savings target of R700 million, in addition to continuing to achieve maximum market premia. We are working hard to further progress our resource development plan and the feasibility study on our UHDMS technology, which will add to the life of Sishen mine is 80% complete.

At Kolomela, we are unlocking the 85 Mt of resources under study and drilling activities are on schedule. Due to the operational challenges experienced over the first few months of the year, our full year total production guidance has been revised to 42 Mt to 43 Mt from 43 Mt to 44 Mt. Full year guidance for sales remained constant at 43 Mt to 44 Mt as we continue to optimise our integrated sales and operations planning. Sishen's production guidance has been revised to between 29 Mt and 30 Mt, while waste guidance remains unchanged at 170 Mt to 180 Mt. Due to the infrastructure upgrade of the DMS plant, we have revised Kolomela's production guidance to ~13 Mt, while waste guidance of 55 Mt to 60 Mt was maintained as previously guided. In line with the revised production guidance at Sishen, the full year unit cash cost guidance of the mine was increased to between R325/tonne and R335/tonne. Kolomela's unit cash cost guidance was revised down to between R255/tonne and R265/tonne.

Our capital expenditure for 2019, including deferred stripping, was revised slightly higher to R4.9 billion to R5.1 billion, from the previous range of R4.6 billion to R4.8 billion, due to an increase in deferred stripping and capital spares aimed at improving the performance and efficiency of our primary equipment and production plants.

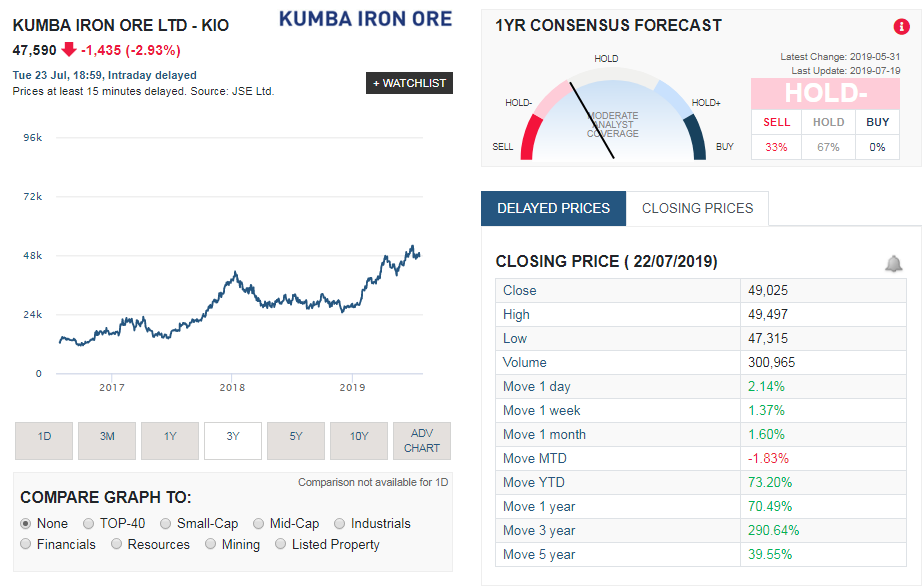

Kumba (KIO) share price performance

The screenshot of KIO taken from Sharenet below shows that KIO has rewarded shareholders over the short and medium term. The last time we covered Kumba Iron ore (on the 14th of May 2019) their price was R419.84. It is currently trading at R475.90. That is a price increase of 13.3% since the middle of May 2019

Below a summary of KIO's share price performance over various time periods:

Below a summary of KIO's share price performance over various time periods:

- Last Week: 1.37%

- Month to Date (MTD) : 1.6%

- Year to Date (YTD): 73.20%

- 1 year move: 70.49%

- 3 years move: 290.64%

- 5 years move: 39.55%

Kumbo Iron Ore Share Price performance in recent months benefited from Vale issues

Kumba Iron Ore share valuation

Below is what we wrote on 19 February 2019 regarding the valuation of Kumba and what we expected from this set of results.

Kumba (KIO) share valuation (as per our last update on KIO on 19 February 2019)

As we mentioned in the introduction, Kumbo Iron Ore shares surged since the start of the year after a tailing dam in Brazil belonging to Vale broke and the ensuing flooding killed almost 170 people lead to Vale suspending the production of Iron ore at the close by iron ore mines, which sent up iron ore prices on supply fears. But all of this happened in the new year and is not currently reflected in KIO's financial results, but it should have a positive impact on their next set of earnings. Based on this and KIO current financial results which places them on a PE ratio of less than 13 and a dividend yield of almost 8% with strong cash generation capacity and loads of cash on their balance sheet, we value the group at R446.68 a share. So we do believe there is value in the share and if the increase in iron ore prices due to the problems in Brazil for Vale filters through into Kumbo's earnings their next set of results will probably have bumper profits, in which investors can hope for a nice windfall dividend.

While our prediction of bumper profits and a windfall dividend payment has come true, we feel the valuation is still relevant as most numbers reported in this set of financial results is skewed to the upside due to the very strong increase in the price of iron ore prices in the last number of months from which Kumba has benefited greatly. We therefore caution against using the latest strong numbers for valuation purposes. We will therefore maintain the valuation provided in February 2019.

Kumba (KIO) share valuation (as per our last update on KIO on 19 February 2019)

As we mentioned in the introduction, Kumbo Iron Ore shares surged since the start of the year after a tailing dam in Brazil belonging to Vale broke and the ensuing flooding killed almost 170 people lead to Vale suspending the production of Iron ore at the close by iron ore mines, which sent up iron ore prices on supply fears. But all of this happened in the new year and is not currently reflected in KIO's financial results, but it should have a positive impact on their next set of earnings. Based on this and KIO current financial results which places them on a PE ratio of less than 13 and a dividend yield of almost 8% with strong cash generation capacity and loads of cash on their balance sheet, we value the group at R446.68 a share. So we do believe there is value in the share and if the increase in iron ore prices due to the problems in Brazil for Vale filters through into Kumbo's earnings their next set of results will probably have bumper profits, in which investors can hope for a nice windfall dividend.

While our prediction of bumper profits and a windfall dividend payment has come true, we feel the valuation is still relevant as most numbers reported in this set of financial results is skewed to the upside due to the very strong increase in the price of iron ore prices in the last number of months from which Kumba has benefited greatly. We therefore caution against using the latest strong numbers for valuation purposes. We will therefore maintain the valuation provided in February 2019.