|

International Monetary Fund (IMF) World economic outlook April 2019

Date: 10 May 2019 Category: Economics and Financial Markets |

Related Topics |

|

In our continued efforts to give our readers a broad number of views, opinions and information, we provide readers with details of the IMF's world economic outlook as published in April 2019. Note South Africa is seen as an Emerging Market economy so if the report references emerging markets, South Africa would fall within this category.

|

|

IMF World Economic Outlook: April 2019

This article will contain graphics, views and opinions as found in the IMF World Economic Outlook document published during April 2019. So lets take a look.

A Weakening Expansion

After strong growth in 2017 and early 2018, global economic activity slowed notably in the second half of last year, reflecting a confluence of factors affecting major economies. China’s growth declined following a combination of needed regulatory tightening to rein in shadow banking and an increase in trade tensions with the United States. The euro area economy lost more momentum than expected as consumer and business confidence weakened and car production in Germany was disrupted by the introduction of new emission standards; investment dropped in Italy as sovereign spreads widened; and external demand, especially from emerging Asia, softened.

Elsewhere, natural disasters hurt activity in Japan. Trade tensions increasingly took a toll on business confidence and, so, financial market sentiment worsened, with financial conditions tightening for vulnerable emerging markets in the spring of 2018 and then in advanced economies later in the year, weighing on global demand. Conditions have eased in 2019 as the US Federal Reserve signaled a more accommodative monetary policy stance and markets became more optimistic about a US–China trade deal, but they remain slightly more restrictive than in the fall.

A Weakening Expansion

After strong growth in 2017 and early 2018, global economic activity slowed notably in the second half of last year, reflecting a confluence of factors affecting major economies. China’s growth declined following a combination of needed regulatory tightening to rein in shadow banking and an increase in trade tensions with the United States. The euro area economy lost more momentum than expected as consumer and business confidence weakened and car production in Germany was disrupted by the introduction of new emission standards; investment dropped in Italy as sovereign spreads widened; and external demand, especially from emerging Asia, softened.

Elsewhere, natural disasters hurt activity in Japan. Trade tensions increasingly took a toll on business confidence and, so, financial market sentiment worsened, with financial conditions tightening for vulnerable emerging markets in the spring of 2018 and then in advanced economies later in the year, weighing on global demand. Conditions have eased in 2019 as the US Federal Reserve signaled a more accommodative monetary policy stance and markets became more optimistic about a US–China trade deal, but they remain slightly more restrictive than in the fall.

Global Growth Is Set to Moderate in the Near Term, Then Pick Up Modestly

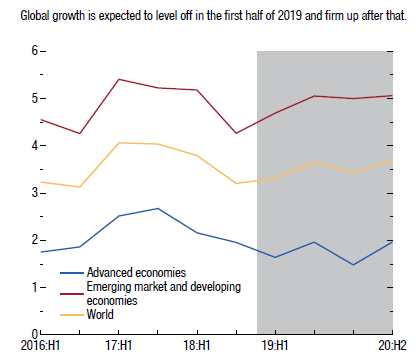

As a result of these developments, global growth is now projected to slow from 3.6 percent in 2018 to 3.3 percent in 2019, before returning to 3.6 percent in 2020. Growth for 2018 was revised down by 0.1 percentage point relative to the October 2018 World Economic Outlook (WEO), reflecting weakness in the second half of the year, and the forecasts for 2019 and 2020 are now marked down by 0.4 percentage point and 0.1 percentage point, respectively. The current forecast envisages that global growth will level off in the first half of 2019 and firm up after that (see image above)

The projected pickup in the second half of 2019 is predicated on an ongoing buildup of policy stimulus in China, recent improvements in global financial market sentiment, the waning of some temporary drags on growth in the euro area, and a gradual stabilization of conditions in stressed emerging market economies, including Argentina and Turkey. Improved momentum for emerging market and developing economies is projected to continue into 2020, primarily reflecting developments in economies currently experiencing macroeconomic distress—a forecast subject to notable

uncertainty. By contrast, activity in advanced economies is projected to continue to slow gradually as the impact of US fiscal stimulus fades and growth tends toward the modest potential for the group. Beyond 2020, global growth is set to plateau at about 3.6 percent over the medium term, sustained by the increase in the relative size of economies, such as those of China and India, which are projected to have robust growth by comparison to slower-growing advanced and emerging market economies (even though Chinese growth will eventually moderate). As noted in previous WEO reports, tepid labor produc-tivity growth and slowing expansion of the labor force amid population aging will drag advanced economy growth lower over the projection horizon.

Growth across emerging market and developing economies is projected to stabilize slightly below 5 percent, though with variations by region and country. The baseline outlook for emerging Asia remains favorable, with China’s growth projected to slow gradually toward sustainable levels and convergence in frontier economies toward higher income levels. For other regions, the outlook is complicated by a combination of structural bottlenecks, slower advanced economy growth and, in some cases, high debt and tighter financial conditions. These factors, alongside subdued commodity prices and civil strife or conflict in some cases, contribute to subdued medium-term prospects for Latin America; the Middle East, North

Africa, and Pakistan region; and parts of sub-Saharan Africa. In particular, convergence prospects are bleak for some 41 emerging market and developing economies, accounting for close to 10 percent of global GDP in purchasing-power-parity terms and with total population close to 1 billion, where per capita incomes are projected to fall further behind those in advanced economies over the next five years.

Risks Are Tilted to the Downside

While global growth could surprise favorably if trade differences are resolved quickly so that business confidence rebounds and investor sentiment strengthens further, the balance of risks to the outlook remains on the downside. A further escalation of trade tensions and the associated increases in policy uncertainty could further weaken growth. The potential remains for sharp deterioration in market sentiment, which would imply portfolio reallocations away from risk assets, wider spreads over safe haven securities, and generally tighter financial conditions, especially for vulnerable economies.

Possible triggers for such an episode include a no-deal Brexit withdrawal of the United Kingdom from the European Union; persistently weak economic data pointing to a protracted global growth slowdown; and prolonged fiscal uncertainty and elevated yields in Italy—particularly if coupled with a deeper recession—with possible adverse spillovers for other euro area economies. A rapid reassessment by markets of the monetary policy stance in the United States could also tighten global financial conditions. Over the medium term, climate change and political discord in the context of rising inequality are key risks that could lower global potential output, with particularly severe implications for some vulnerable countries.

Policy Priorities

Amid waning global growth momentum and limited policy space to combat downturns, avoiding policy missteps that could harm economic activity needs to be the main priority. Macroeconomic and financial policy should aim to prevent further deceleration where output could fall below potential and facilitate a soft landing where policy support needs to be withdrawn.

At the national level, this requires monetary policy to ensure that inflation remains on track toward the central bank’s target (or if it is close to target, that it stabilizes there) and that inflation expectations remain anchored. It requires fiscal policy to manage tradeoffs between supporting demand and making sure that public debt stays on a sustainable path. Where fiscal consolidation is needed and monetary policy is constrained, its pace should be calibrated to secure stability while avoiding harming near-term growth and depleting programs that protect the vulnerable. If the current slowdown turns out to be more severe and protracted than expected in the baseline, macroeconomic policies should become more accommodative, particularly where output remains below potential and financial stability is not at risk.

Across all economies, the imperative is to take actions that boost potential output growth, improve inclusiveness, and strengthen resilience. At the multilateral level, the main priority is for countries to resolve trade disagreements cooperatively, without raising distortionary barriers that would further destabilize a slowing global economy.

As a result of these developments, global growth is now projected to slow from 3.6 percent in 2018 to 3.3 percent in 2019, before returning to 3.6 percent in 2020. Growth for 2018 was revised down by 0.1 percentage point relative to the October 2018 World Economic Outlook (WEO), reflecting weakness in the second half of the year, and the forecasts for 2019 and 2020 are now marked down by 0.4 percentage point and 0.1 percentage point, respectively. The current forecast envisages that global growth will level off in the first half of 2019 and firm up after that (see image above)

The projected pickup in the second half of 2019 is predicated on an ongoing buildup of policy stimulus in China, recent improvements in global financial market sentiment, the waning of some temporary drags on growth in the euro area, and a gradual stabilization of conditions in stressed emerging market economies, including Argentina and Turkey. Improved momentum for emerging market and developing economies is projected to continue into 2020, primarily reflecting developments in economies currently experiencing macroeconomic distress—a forecast subject to notable

uncertainty. By contrast, activity in advanced economies is projected to continue to slow gradually as the impact of US fiscal stimulus fades and growth tends toward the modest potential for the group. Beyond 2020, global growth is set to plateau at about 3.6 percent over the medium term, sustained by the increase in the relative size of economies, such as those of China and India, which are projected to have robust growth by comparison to slower-growing advanced and emerging market economies (even though Chinese growth will eventually moderate). As noted in previous WEO reports, tepid labor produc-tivity growth and slowing expansion of the labor force amid population aging will drag advanced economy growth lower over the projection horizon.

Growth across emerging market and developing economies is projected to stabilize slightly below 5 percent, though with variations by region and country. The baseline outlook for emerging Asia remains favorable, with China’s growth projected to slow gradually toward sustainable levels and convergence in frontier economies toward higher income levels. For other regions, the outlook is complicated by a combination of structural bottlenecks, slower advanced economy growth and, in some cases, high debt and tighter financial conditions. These factors, alongside subdued commodity prices and civil strife or conflict in some cases, contribute to subdued medium-term prospects for Latin America; the Middle East, North

Africa, and Pakistan region; and parts of sub-Saharan Africa. In particular, convergence prospects are bleak for some 41 emerging market and developing economies, accounting for close to 10 percent of global GDP in purchasing-power-parity terms and with total population close to 1 billion, where per capita incomes are projected to fall further behind those in advanced economies over the next five years.

Risks Are Tilted to the Downside

While global growth could surprise favorably if trade differences are resolved quickly so that business confidence rebounds and investor sentiment strengthens further, the balance of risks to the outlook remains on the downside. A further escalation of trade tensions and the associated increases in policy uncertainty could further weaken growth. The potential remains for sharp deterioration in market sentiment, which would imply portfolio reallocations away from risk assets, wider spreads over safe haven securities, and generally tighter financial conditions, especially for vulnerable economies.

Possible triggers for such an episode include a no-deal Brexit withdrawal of the United Kingdom from the European Union; persistently weak economic data pointing to a protracted global growth slowdown; and prolonged fiscal uncertainty and elevated yields in Italy—particularly if coupled with a deeper recession—with possible adverse spillovers for other euro area economies. A rapid reassessment by markets of the monetary policy stance in the United States could also tighten global financial conditions. Over the medium term, climate change and political discord in the context of rising inequality are key risks that could lower global potential output, with particularly severe implications for some vulnerable countries.

Policy Priorities

Amid waning global growth momentum and limited policy space to combat downturns, avoiding policy missteps that could harm economic activity needs to be the main priority. Macroeconomic and financial policy should aim to prevent further deceleration where output could fall below potential and facilitate a soft landing where policy support needs to be withdrawn.

At the national level, this requires monetary policy to ensure that inflation remains on track toward the central bank’s target (or if it is close to target, that it stabilizes there) and that inflation expectations remain anchored. It requires fiscal policy to manage tradeoffs between supporting demand and making sure that public debt stays on a sustainable path. Where fiscal consolidation is needed and monetary policy is constrained, its pace should be calibrated to secure stability while avoiding harming near-term growth and depleting programs that protect the vulnerable. If the current slowdown turns out to be more severe and protracted than expected in the baseline, macroeconomic policies should become more accommodative, particularly where output remains below potential and financial stability is not at risk.

Across all economies, the imperative is to take actions that boost potential output growth, improve inclusiveness, and strengthen resilience. At the multilateral level, the main priority is for countries to resolve trade disagreements cooperatively, without raising distortionary barriers that would further destabilize a slowing global economy.

Global inflation

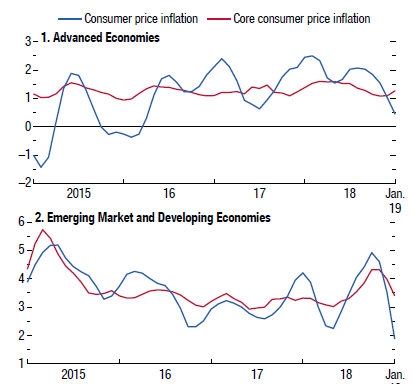

Consumer price inflation remained muted across advanced economies, given the drop in commodity prices. For some emerging market economies, currency depreciations have passed through to higher domestic prices, partially offsetting downward pressure from lower commodity prices. the image below shows consumer price inflation and core consumer price inflation in advanced economies as well as emerging markets and developing economies. As the image shows while advanced economies have lower levels of inflation than emerging markets and developing economies, inflation moderated sharply for advanced, emerging and developing economies towards the end of 2018 as well as early 2019.

A Precarious Recovery in Emerging Market and Developing Economies

Global growth in 2019 is also weighed down by the emerging market and developing economy group, where growth is expected to tick down to 4.4 percent in 2019 (from 4.5 percent in 2018), 0.3 percentage point lower than in the October 2018 WEO. The decline in growth relative to 2018 reflects lower growth in China and the recession in Turkey, with an important carryover from weaker activity in late 2018, as well as a deepening contraction in Iran.

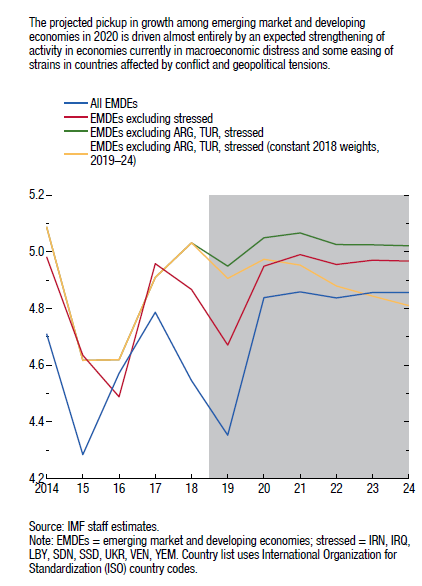

Conditions are projected to improve during 2019 as stimulus measures sustain activity in China and recession strains gradually ease in economies such as Argentina and Turkey. In 2020, growth is projected to rise to 4.8 percent, driven almost entirely by an expected strengthening of activity in these economies on the back of policy adjustment and some easing of strains in countries affected by conflict and geopolitical tensions.

For the latter group of countries in particular, the forecast is subject to very significant uncertainty. With declining growth in advanced economies, the projected pickup in global growth in 2020 is entirely predicated on this projected improvement for the emerging market and developing economy group. The image below also highlights the role played by the increasing weight of fast-growing economies, such as China and India, in supporting aggregate growth for emerging markets and developing economies as well as world growth.

Conditions are projected to improve during 2019 as stimulus measures sustain activity in China and recession strains gradually ease in economies such as Argentina and Turkey. In 2020, growth is projected to rise to 4.8 percent, driven almost entirely by an expected strengthening of activity in these economies on the back of policy adjustment and some easing of strains in countries affected by conflict and geopolitical tensions.

For the latter group of countries in particular, the forecast is subject to very significant uncertainty. With declining growth in advanced economies, the projected pickup in global growth in 2020 is entirely predicated on this projected improvement for the emerging market and developing economy group. The image below also highlights the role played by the increasing weight of fast-growing economies, such as China and India, in supporting aggregate growth for emerging markets and developing economies as well as world growth.

Near-term prospects for emerging market and developing economies continue to be shaped by the interaction between country-specific fundamentals and a challenging external environment marked by the slowdown in advanced economies; trade tensions; expected gradual tightening of financial conditions consistent with some further removal of monetary policy accommodation in the United States; and, for commodity exporters, a generally subdued outlook for commodity prices (including oil prices, which are projected to remain below their 2018 average throughout the forecast horizon).

Growth in emerging and developing Asia is expected to dip to 6.3 percent in 2019 and 2020 (from 6.4 percent in 2018), with a marginal downward revision for 2020 relative to the October WEO. Economic growth in China, despite fiscal stimulus and no further increase in tariffs from the United States relative to those in force as of September 2018, is projected to slow on an annualized basis in 2019 and 2020. This reflects weaker underlying

growth in 2018, especially in the second half, and the impact of lingering trade tensions with the United States. The projection for 2019 is slightly stronger than in the October 2018 WEO, reflecting the revised assumption on United States tariffs on Chinese exports, as described in Box 1.2, while the projection for 2020 is slightly weaker, as the underlying momentum in activity is more subdued. In India, growth is projected to pick up to 7.3 percent in 2019 and 7.5 percent in 2020, supported by the continued recovery of investment and robust consumption amid a more expansionary stance of monetary policy and some expected impetus from fiscal policy.

Nevertheless, reflecting the recent revision to the national account statistics that indicated somewhat softer underlying momentum, growth forecasts have been revised downward compared with the October 2018 WEO by 0.1 percentage point for 2019 and 0.2 percentage point for 2020, respectively.

Activity in emerging and developing Europe in 2019 is expected to weaken more than previously anticipated, despite generally buoyant and higher-than-expected growth in several central and eastern European countries, before recovering in 2020. The sizable revision for the region is mostly due to a substantial projected contraction in Turkey in 2019, where the weakness in demand—following tighter external financing conditions and needed policy tightening—is expected to continue in early 2019 before a recovery takes hold in the second half of the year.

In Latin America, growth is projected to recover over the next two years, to 1.4 percent in 2019 and 2.4 percent in 2020. In Brazil, growth is projected to strengthen from 1.1 percent in 2018 to 2.1 percent in 2019 and 2.5 percent in 2020. In Mexico, growth is now forecast to remain below 2 percent in 2019–20, a markdown close to 1 percentage point for both years relative to October. These changes, in part, reflect shifts in perceptions about policy direction under new administrations in both countries. Argentina’s economy is projected to contract in the first half of 2019 as domestic demand slows with tighter policies to reduce imbalances, returning to growth in the second half of the year as real disposable income recovers and agricultural production rebounds after last year’s drought. Venezuela’s economy is expected to contract by one-fourth in 2019, and a further 10 percent in 2020—a greater collapse than projected in the October 2018 WEO and one that generates a sizable drag on projected growth for the region and for the emerging market and developing economy group in both years

Growth in the Middle East, North Africa, Afghanistan, and Pakistan region is expected to decline to 1.5 percent in 2019, before recovering to about 3.2 percent in 2020. The outlook for the region is weighed down by multiple factors, including slower oil GDP growth in Saudi Arabia; ongoing macroeconomic adjustment challenges in Pakistan; US sanctions in Iran; and civil tensions and conflict across several other economies, including Iraq, Syria, and Yemen, where recovery from the collapse associated with the war is now expected to be slower than previously anticipated.

In sub-Saharan Africa, growth is expected to pick up to 3.5 percent in 2019 and 3.7 percent in 2020 (from 3.0 percent in 2018). The projection is 0.3 percentage point and 0.2 percentage point lower for 2019 and 2020, respectively, than in the October 2018 WEO, reflecting downward revisions for Angola and Nigeria with the softening of oil prices.

Growth in South Africa is expected to marginally improve from 0.8 percent in 2018 to 1.2 percent in 2019 and 1.5 percent in 2020, a 0.2 percentage point downward revision for both years relative to the October projections. The projected recovery reflects modestly reduced but continued policy uncertainty in the South African economy after the May 2019 elections.

Activity in the Commonwealth of Independent States is projected to expand about 2¼ percent in 2019–20, slightly lower than projected in the October 2018 WEO, as weaker oil prices weigh on Russia’s growth prospects.

Modest Outlook for Medium-Term Growth

Beyond 2020, global growth is set to plateau at 3.6 percent over the medium term. For the advanced economy group, growth is projected to moderate further over the medium term as the underlying structural headwinds to potential output (namely, continued weak productivity growth and slowing laborforce growth) increasingly assert influence on the path of output as the cyclical forces discussed above fadeaway. Growth for the emerging market and developing economy group is expected to broadly stabilize at its2020 level for the outer years of the forecast horizon, but with important offsetting regional differences.

Specifically, for advanced economies, growth is projected to slow to 1.6 percent by 2022 and remain at that level thereafter. The productivity slowdown that set in before the 2008–09 global financial crisis (Adler and others 2017) is projected to abate somewhat, with a slight pickup in productivity expected over the medium term. Despite the apparent proliferation of digitalization and automation, their cumulative impact on productivity is expected to be modest over the forecast horizon—likely benefiting consumer welfare to a larger extent than labor productivity

Other developments potentially have less favorable implications for productivity. These include the retreat from global economic integration (projections for global trade volume growth have been marked down following the tariff increases of 2018).The modest uptick expected in productivity is likely only partially to counteract the drag on potential output growth anticipated from slower labor force growth as the population ages. This is particularly relevant for Japan and southern Europe.

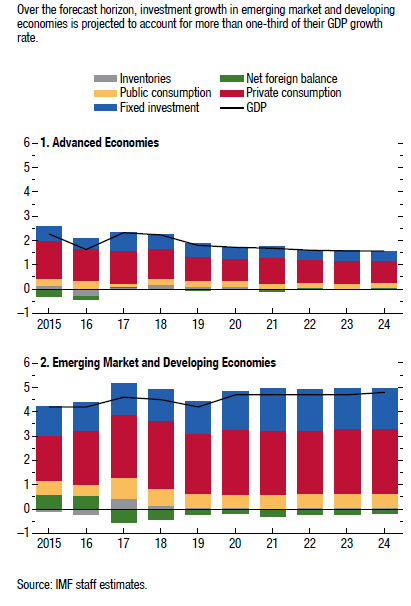

For emerging market and developing economies, growth is projected to stabilize at about 4.8 percent over the medium term. The combination of higher growth than in advanced economies and the group’s rising weight in global GDP translates into a significant increase in emerging market and developing economies’ share of global growth, from 76 percent in 2019 to about 85 percent in 2024. The medium-term growth forecast incorporates continued strong investment growth in emerging market and developing economies, accounting for more than one-third of their GDP growth rate during the projection horizon (see image below) .

Growth in emerging and developing Asia is expected to dip to 6.3 percent in 2019 and 2020 (from 6.4 percent in 2018), with a marginal downward revision for 2020 relative to the October WEO. Economic growth in China, despite fiscal stimulus and no further increase in tariffs from the United States relative to those in force as of September 2018, is projected to slow on an annualized basis in 2019 and 2020. This reflects weaker underlying

growth in 2018, especially in the second half, and the impact of lingering trade tensions with the United States. The projection for 2019 is slightly stronger than in the October 2018 WEO, reflecting the revised assumption on United States tariffs on Chinese exports, as described in Box 1.2, while the projection for 2020 is slightly weaker, as the underlying momentum in activity is more subdued. In India, growth is projected to pick up to 7.3 percent in 2019 and 7.5 percent in 2020, supported by the continued recovery of investment and robust consumption amid a more expansionary stance of monetary policy and some expected impetus from fiscal policy.

Nevertheless, reflecting the recent revision to the national account statistics that indicated somewhat softer underlying momentum, growth forecasts have been revised downward compared with the October 2018 WEO by 0.1 percentage point for 2019 and 0.2 percentage point for 2020, respectively.

Activity in emerging and developing Europe in 2019 is expected to weaken more than previously anticipated, despite generally buoyant and higher-than-expected growth in several central and eastern European countries, before recovering in 2020. The sizable revision for the region is mostly due to a substantial projected contraction in Turkey in 2019, where the weakness in demand—following tighter external financing conditions and needed policy tightening—is expected to continue in early 2019 before a recovery takes hold in the second half of the year.

In Latin America, growth is projected to recover over the next two years, to 1.4 percent in 2019 and 2.4 percent in 2020. In Brazil, growth is projected to strengthen from 1.1 percent in 2018 to 2.1 percent in 2019 and 2.5 percent in 2020. In Mexico, growth is now forecast to remain below 2 percent in 2019–20, a markdown close to 1 percentage point for both years relative to October. These changes, in part, reflect shifts in perceptions about policy direction under new administrations in both countries. Argentina’s economy is projected to contract in the first half of 2019 as domestic demand slows with tighter policies to reduce imbalances, returning to growth in the second half of the year as real disposable income recovers and agricultural production rebounds after last year’s drought. Venezuela’s economy is expected to contract by one-fourth in 2019, and a further 10 percent in 2020—a greater collapse than projected in the October 2018 WEO and one that generates a sizable drag on projected growth for the region and for the emerging market and developing economy group in both years

Growth in the Middle East, North Africa, Afghanistan, and Pakistan region is expected to decline to 1.5 percent in 2019, before recovering to about 3.2 percent in 2020. The outlook for the region is weighed down by multiple factors, including slower oil GDP growth in Saudi Arabia; ongoing macroeconomic adjustment challenges in Pakistan; US sanctions in Iran; and civil tensions and conflict across several other economies, including Iraq, Syria, and Yemen, where recovery from the collapse associated with the war is now expected to be slower than previously anticipated.

In sub-Saharan Africa, growth is expected to pick up to 3.5 percent in 2019 and 3.7 percent in 2020 (from 3.0 percent in 2018). The projection is 0.3 percentage point and 0.2 percentage point lower for 2019 and 2020, respectively, than in the October 2018 WEO, reflecting downward revisions for Angola and Nigeria with the softening of oil prices.

Growth in South Africa is expected to marginally improve from 0.8 percent in 2018 to 1.2 percent in 2019 and 1.5 percent in 2020, a 0.2 percentage point downward revision for both years relative to the October projections. The projected recovery reflects modestly reduced but continued policy uncertainty in the South African economy after the May 2019 elections.

Activity in the Commonwealth of Independent States is projected to expand about 2¼ percent in 2019–20, slightly lower than projected in the October 2018 WEO, as weaker oil prices weigh on Russia’s growth prospects.

Modest Outlook for Medium-Term Growth

Beyond 2020, global growth is set to plateau at 3.6 percent over the medium term. For the advanced economy group, growth is projected to moderate further over the medium term as the underlying structural headwinds to potential output (namely, continued weak productivity growth and slowing laborforce growth) increasingly assert influence on the path of output as the cyclical forces discussed above fadeaway. Growth for the emerging market and developing economy group is expected to broadly stabilize at its2020 level for the outer years of the forecast horizon, but with important offsetting regional differences.

Specifically, for advanced economies, growth is projected to slow to 1.6 percent by 2022 and remain at that level thereafter. The productivity slowdown that set in before the 2008–09 global financial crisis (Adler and others 2017) is projected to abate somewhat, with a slight pickup in productivity expected over the medium term. Despite the apparent proliferation of digitalization and automation, their cumulative impact on productivity is expected to be modest over the forecast horizon—likely benefiting consumer welfare to a larger extent than labor productivity

Other developments potentially have less favorable implications for productivity. These include the retreat from global economic integration (projections for global trade volume growth have been marked down following the tariff increases of 2018).The modest uptick expected in productivity is likely only partially to counteract the drag on potential output growth anticipated from slower labor force growth as the population ages. This is particularly relevant for Japan and southern Europe.

For emerging market and developing economies, growth is projected to stabilize at about 4.8 percent over the medium term. The combination of higher growth than in advanced economies and the group’s rising weight in global GDP translates into a significant increase in emerging market and developing economies’ share of global growth, from 76 percent in 2019 to about 85 percent in 2024. The medium-term growth forecast incorporates continued strong investment growth in emerging market and developing economies, accounting for more than one-third of their GDP growth rate during the projection horizon (see image below) .

In turn, this robust investment path is predicated on a smooth trajectory for the drivers of capital spending; a gradual tightening in financial conditions (which is particularly relevant to the investment outlook in the emerging market and developing economy group, given the rapid buildup of leverage during years of low interest rates); quick resolution of trade disagreements and subsequent easing of trade tensions; and broader policy actions that help reduce uncertainty.

The medium-term growth forecast for emerging market and developing economies reflects important differences across regions. In emerging Asia, growth is expected to remain above 6 percent through the forecast horizon. Central to this smooth growth profile is a gradual slowdown in China to 5.5 percent by 2024 as internal rebalancing toward a private-consumption and services-based economy continues and regulatory tightening

slows the accumulation of debt and associated

vulnerabilities.

Growth in India is expected to stabilize at just under 7¾ percent over the medium term, based on continued implementation of structural reforms and easing of infrastructure bottlenecks. In Latin America, growth is projected to increase from 2.4 percent in 2020 to 2.8 percent over the

medium term. Financial stabilization and recovery in Argentina, where growth is projected to strengthen to about 3½ percent over the medium term, contributes to that region’s growth improvement. So is stable, though moderate, growth in Brazil and Mexico (in the range of 2¼–2¾ percent) as structural rigidities, subdued terms of trade, and fiscal imbalances (particularly for Brazil) weigh on the outlook.

Activity in emerging Europe is projected to pick up from the current post-global-financial-crisis low, with the region expected to grow just above 3 percent over the medium term. This improvement reflects primarily the forecast for Turkey, where activity is projected to gradually strengthen after the economy returns to positive annual growth in 2020. Over the medium term, Turkey’s growth is projected to pick up to 3.5 percent as domestic demand recovers from the current sharp contraction that is reducing macroeconomic and financial imbalances. For other economies in the region with robust growth rates in recent years, such as Poland and Romania, growth is expected to moderate to about 3 percent over the medium term, reflecting the fading of stimulus from EU investment funds and accommodative policies.

The outlook for the Commonwealth of Independent States is for growth to stabilize at 2.4 percent over the

medium term. This largely reflects sluggish growth in Russia of about 1½ percent over the medium term,

weighed down by the modest outlook for oil prices and structural headwinds.

Prospects vary across sub-Saharan Africa, reflecting the heterogeneity of the economies, associated with disparities in the level of development, exposure to weather shocks, and commodity dependence. For the region as a whole, growth is projected to increase from 3.7 percent in 2020 to about 4 percent in 2024 (although for close to two-fifths of economies, the average growth rate over the medium term is projected to exceed 5 percent). Growth prospects for commodity exporters are weighed down by the soft outlook for commodity prices, including for Nigeria and Angola, where growth is expected to reach about 2.6 percent and 3.9 percent, respectively, in the medium term.

In South Africa, growth is projected to stabilize at 1¾ percent over the medium term as structural bottlenecks continue to weigh on investment and productivity, and metal export prices are expected to remain subdued. Rising debt-service costs as financial conditions tighten globally and difficult adjustment processes to diversify production structures away from resource extraction are expected to weigh on growth in many economies across the region.

The medium-term outlook for the Middle East, North Africa, Afghanistan, and Pakistan region is largely shaped by the outlook for fuel prices, needed adjustment to correct macroeconomic imbalances in certain economies, and geopolitical tensions. Growth in Saudi Arabia is expected to stabilize at about 2¼–2½ percent over the medium term, as stronger non-oil growth is countered by the subdued outlook for oil prices and output. In Pakistan, in the absence of further adjustment policies, growth is projected to remain subdued at about 2.5 percent, with continued external and fiscal imbalances weighing on confidence. Elsewhere in the region, activity is weighed down by the expected impact of sanctions in Iran, civil strife in Syria and Yemen, and rising debt-service costs and tighter financial conditions in Lebanon. Convergence prospects are bleak for some emerging market and developing economies.

Across sub-Saharan Africa and the Middle East, North Africa, Afghanistan, and Pakistan region, 41 economies, accounting for close to 10 percent of global GDP in purchasing-power-parity terms and close to 1 billion in population, are projected to grow by less than advanced economies in per capita terms over the next five years, implying that their income levels are set to fall further behind those economies

For more details we encourage readers to visit the IMF's website and download the full 216 page World Economic Outlook

The medium-term growth forecast for emerging market and developing economies reflects important differences across regions. In emerging Asia, growth is expected to remain above 6 percent through the forecast horizon. Central to this smooth growth profile is a gradual slowdown in China to 5.5 percent by 2024 as internal rebalancing toward a private-consumption and services-based economy continues and regulatory tightening

slows the accumulation of debt and associated

vulnerabilities.

Growth in India is expected to stabilize at just under 7¾ percent over the medium term, based on continued implementation of structural reforms and easing of infrastructure bottlenecks. In Latin America, growth is projected to increase from 2.4 percent in 2020 to 2.8 percent over the

medium term. Financial stabilization and recovery in Argentina, where growth is projected to strengthen to about 3½ percent over the medium term, contributes to that region’s growth improvement. So is stable, though moderate, growth in Brazil and Mexico (in the range of 2¼–2¾ percent) as structural rigidities, subdued terms of trade, and fiscal imbalances (particularly for Brazil) weigh on the outlook.

Activity in emerging Europe is projected to pick up from the current post-global-financial-crisis low, with the region expected to grow just above 3 percent over the medium term. This improvement reflects primarily the forecast for Turkey, where activity is projected to gradually strengthen after the economy returns to positive annual growth in 2020. Over the medium term, Turkey’s growth is projected to pick up to 3.5 percent as domestic demand recovers from the current sharp contraction that is reducing macroeconomic and financial imbalances. For other economies in the region with robust growth rates in recent years, such as Poland and Romania, growth is expected to moderate to about 3 percent over the medium term, reflecting the fading of stimulus from EU investment funds and accommodative policies.

The outlook for the Commonwealth of Independent States is for growth to stabilize at 2.4 percent over the

medium term. This largely reflects sluggish growth in Russia of about 1½ percent over the medium term,

weighed down by the modest outlook for oil prices and structural headwinds.

Prospects vary across sub-Saharan Africa, reflecting the heterogeneity of the economies, associated with disparities in the level of development, exposure to weather shocks, and commodity dependence. For the region as a whole, growth is projected to increase from 3.7 percent in 2020 to about 4 percent in 2024 (although for close to two-fifths of economies, the average growth rate over the medium term is projected to exceed 5 percent). Growth prospects for commodity exporters are weighed down by the soft outlook for commodity prices, including for Nigeria and Angola, where growth is expected to reach about 2.6 percent and 3.9 percent, respectively, in the medium term.

In South Africa, growth is projected to stabilize at 1¾ percent over the medium term as structural bottlenecks continue to weigh on investment and productivity, and metal export prices are expected to remain subdued. Rising debt-service costs as financial conditions tighten globally and difficult adjustment processes to diversify production structures away from resource extraction are expected to weigh on growth in many economies across the region.

The medium-term outlook for the Middle East, North Africa, Afghanistan, and Pakistan region is largely shaped by the outlook for fuel prices, needed adjustment to correct macroeconomic imbalances in certain economies, and geopolitical tensions. Growth in Saudi Arabia is expected to stabilize at about 2¼–2½ percent over the medium term, as stronger non-oil growth is countered by the subdued outlook for oil prices and output. In Pakistan, in the absence of further adjustment policies, growth is projected to remain subdued at about 2.5 percent, with continued external and fiscal imbalances weighing on confidence. Elsewhere in the region, activity is weighed down by the expected impact of sanctions in Iran, civil strife in Syria and Yemen, and rising debt-service costs and tighter financial conditions in Lebanon. Convergence prospects are bleak for some emerging market and developing economies.

Across sub-Saharan Africa and the Middle East, North Africa, Afghanistan, and Pakistan region, 41 economies, accounting for close to 10 percent of global GDP in purchasing-power-parity terms and close to 1 billion in population, are projected to grow by less than advanced economies in per capita terms over the next five years, implying that their income levels are set to fall further behind those economies

For more details we encourage readers to visit the IMF's website and download the full 216 page World Economic Outlook