|

Related Topics |

|

We take a look at a report published by United Nations Conference on Trade and Development (UNCTAD) in which it raises concerns regarding the sustainability of rising and high debt levels of developing countries.

The text in the article below is obtained from UNCTAD's report called "Current challenges to developing country debt sustainability" |

|

Introduction

Ten years after the global financial crisis, UNCTAD estimates that the ratio of global debt to gross domestic product (GDP) was a third higher at the beginning of 2018 than at the start of the crisis in 2007/2008, and roughly four times global GDP1 . While rising indebtedness is a general and global phenomenon, it is the debt levels of developing countries that have highlighted future debt sustainability vulnerabilities. In this paper, it is argued that it is only in the context of the conditions and mechanisms created by the global financial system that the increasing indebtedness of developing countries can be understood.

While it is generally accepted that the provision of unprecedented levels of liquidity by advanced economies to counter weakness and instability in their economies following the global financial crisis of 2007–2008 sowed the seeds for the next crisis by making portfolio capital flows to developing countries more attractive; the global financial system that created the crisis remains in place and continues to exert its influence over debt sustainability in developing countries. Monetary expansion, accompanied by private sector deleveraging, weak aggregate demand and volatile financial conditions, did little to help boost private capital formation.

The bulk of the newly available credit remained unused or was channelled towards speculative markets. In particular, the lopsided policy response to inadequate demand in the advanced economies made asset markets in developed (and emerging) economies default destinations for international investors seeking higher yields. For some time, this trend encouraged credit expansion in developing countries, appreciated their currencies and propelled commodity prices above the levels justified by market fundamentals alone. These flows have led to increasing indebtedness of developing countries, most notably, emerging market economies, but also some of the poorest countries emerging successfully from the Heavily Indebted Poor Countries Debt Initiative and the Multilateral Debt Relief Initiative, designed to relieve them from unsustainable debt. In recent years, developing countries have faced renewed financial stress in a context of increased (and, in many cases, premature) connectivity to international financial markets. It could be argued that the constraints imposed by a world with policy parameters shaped by unregulated international financial markets are particularly binding on developing countries. This point of departure acknowledges that developing countries’ vulnerabilities are not due to their failure to organize themselves and to create policy space for themselves; they are largely influenced by global trends over which they have little control (Dymski, 2018).

The picture worldwide appears to be one of economic growth that continues to be reliant on debt. This situation is a result of four decades of financial globalization that have undone regulation designed to contain cross-border capital flows, with financial capital chasing existing assets that have little to do with productive investment or employment creation. The returns have increasingly flowed to fewer and fewer multinationals, rather than to households or to the State. Governments have become increasingly diminished in terms of capacity and control, while remaining responsible should debt sustainability become a problem.

While it is unrealistic to expect developing countries to meet their development needs – let alone achieve the Sustainable Development Goals – without recourse to external resources, unregulated capital inflows can lead to exchange rate appreciation, reducing the competitiveness of domestic industry and having a negative impact on export earnings. Flows contributing to high levels of indebtedness are associated with increased vulnerability and high precautionary reserve accumulation. These reserves represent forgone opportunities in terms of much-needed investment and social expenditure in developing countries. The inflows to developing countries over the past decade also represent a rise in the accumulation of private, non-financial, corporate debt. The rise in corporate debt in developing countries in the context of liquidity seeking high yields presents a number of complexities for debt sustainability – the productivity of the inflows is questionable – and, given that such debt is contracted at market rates, its serviceability is unknown. When conditions in advanced countries change, developing countries are likely to experience sudden capital reversals. In recent decades, some emerging economies, particularly those relying on primary exports or low-skill manufactures, have enjoyed export success. However, this success has, in many cases, come at the expense of economic diversification, a key to growth in the long term. Those economies whose export growth is commodity dependent are now beginning to experience severe price shocks, diminishing fiscal and foreign exchange earnings and slower growth; all of which continue to challenge their debt sustainability. At the international level, what developing countries require most to help with finance structural transformation is long-term access to foreign demand, and thus reliable export markets, to support their emergent domestic growth, and investment to repay external debt.

The challenge for the Governments of increasingly vulnerable economies is finding room to manoeuvre to manage debt sustainably, while ensuring growth-inducing expenditure to enhance development. In this report, it is argued that, within the global financial system, developing countries have a limited number of choices, and that, in the absence of sweeping reform of the global financial system, regional and interregional monetary and financial cooperation and reliance on directed development banking may be a good place to start. The report is divided into five sections. Section I provides the point of departure for understanding the debt sustainability challenges of developing countries. Section II examines the debt indicators for 145 developing and transitional countries on a regional basis. The data are limited in scope but provide a useful point of departure for forming a picture of debt at the regional level. More specific data for emerging markets as a subcategory of developing countries show increasing exposure of emerging markets to spillover debt from advanced countries.

Financialization has not delivered on its promises of growth and, in the context of persistent downward pressure on aggregate demand, income and employment, together with systemic financial fragility and recurrent instability, a new development agenda must be found. Section III introduces elements of a balanced growth strategy and section IV contains discussion of the financial elements that would facilitate such a strategy. In the absence of international commitment to reform the global financial system, second best approaches to pre-empt and circumvent its influence on developing countries must be found. A number of such approaches, including the development of regional and interregional monetary and financial cooperation and an invigorated role for development banks in local development, are discussed in section IV. Section V consists of a brief conclusion.

While it is generally accepted that the provision of unprecedented levels of liquidity by advanced economies to counter weakness and instability in their economies following the global financial crisis of 2007–2008 sowed the seeds for the next crisis by making portfolio capital flows to developing countries more attractive; the global financial system that created the crisis remains in place and continues to exert its influence over debt sustainability in developing countries. Monetary expansion, accompanied by private sector deleveraging, weak aggregate demand and volatile financial conditions, did little to help boost private capital formation.

The bulk of the newly available credit remained unused or was channelled towards speculative markets. In particular, the lopsided policy response to inadequate demand in the advanced economies made asset markets in developed (and emerging) economies default destinations for international investors seeking higher yields. For some time, this trend encouraged credit expansion in developing countries, appreciated their currencies and propelled commodity prices above the levels justified by market fundamentals alone. These flows have led to increasing indebtedness of developing countries, most notably, emerging market economies, but also some of the poorest countries emerging successfully from the Heavily Indebted Poor Countries Debt Initiative and the Multilateral Debt Relief Initiative, designed to relieve them from unsustainable debt. In recent years, developing countries have faced renewed financial stress in a context of increased (and, in many cases, premature) connectivity to international financial markets. It could be argued that the constraints imposed by a world with policy parameters shaped by unregulated international financial markets are particularly binding on developing countries. This point of departure acknowledges that developing countries’ vulnerabilities are not due to their failure to organize themselves and to create policy space for themselves; they are largely influenced by global trends over which they have little control (Dymski, 2018).

The picture worldwide appears to be one of economic growth that continues to be reliant on debt. This situation is a result of four decades of financial globalization that have undone regulation designed to contain cross-border capital flows, with financial capital chasing existing assets that have little to do with productive investment or employment creation. The returns have increasingly flowed to fewer and fewer multinationals, rather than to households or to the State. Governments have become increasingly diminished in terms of capacity and control, while remaining responsible should debt sustainability become a problem.

While it is unrealistic to expect developing countries to meet their development needs – let alone achieve the Sustainable Development Goals – without recourse to external resources, unregulated capital inflows can lead to exchange rate appreciation, reducing the competitiveness of domestic industry and having a negative impact on export earnings. Flows contributing to high levels of indebtedness are associated with increased vulnerability and high precautionary reserve accumulation. These reserves represent forgone opportunities in terms of much-needed investment and social expenditure in developing countries. The inflows to developing countries over the past decade also represent a rise in the accumulation of private, non-financial, corporate debt. The rise in corporate debt in developing countries in the context of liquidity seeking high yields presents a number of complexities for debt sustainability – the productivity of the inflows is questionable – and, given that such debt is contracted at market rates, its serviceability is unknown. When conditions in advanced countries change, developing countries are likely to experience sudden capital reversals. In recent decades, some emerging economies, particularly those relying on primary exports or low-skill manufactures, have enjoyed export success. However, this success has, in many cases, come at the expense of economic diversification, a key to growth in the long term. Those economies whose export growth is commodity dependent are now beginning to experience severe price shocks, diminishing fiscal and foreign exchange earnings and slower growth; all of which continue to challenge their debt sustainability. At the international level, what developing countries require most to help with finance structural transformation is long-term access to foreign demand, and thus reliable export markets, to support their emergent domestic growth, and investment to repay external debt.

The challenge for the Governments of increasingly vulnerable economies is finding room to manoeuvre to manage debt sustainably, while ensuring growth-inducing expenditure to enhance development. In this report, it is argued that, within the global financial system, developing countries have a limited number of choices, and that, in the absence of sweeping reform of the global financial system, regional and interregional monetary and financial cooperation and reliance on directed development banking may be a good place to start. The report is divided into five sections. Section I provides the point of departure for understanding the debt sustainability challenges of developing countries. Section II examines the debt indicators for 145 developing and transitional countries on a regional basis. The data are limited in scope but provide a useful point of departure for forming a picture of debt at the regional level. More specific data for emerging markets as a subcategory of developing countries show increasing exposure of emerging markets to spillover debt from advanced countries.

Financialization has not delivered on its promises of growth and, in the context of persistent downward pressure on aggregate demand, income and employment, together with systemic financial fragility and recurrent instability, a new development agenda must be found. Section III introduces elements of a balanced growth strategy and section IV contains discussion of the financial elements that would facilitate such a strategy. In the absence of international commitment to reform the global financial system, second best approaches to pre-empt and circumvent its influence on developing countries must be found. A number of such approaches, including the development of regional and interregional monetary and financial cooperation and an invigorated role for development banks in local development, are discussed in section IV. Section V consists of a brief conclusion.

Global debt stocks rose from US$69 trillion in 1995 to over US$140 trillion in 2007, and as much as US$247 trillion by early 2018. The indebtedness associated with this global rise in debt stocks between 1995 and 2007 affected all sectors, with the build-up concentrated in households and financial institutions (Kozul-Wright, 2019; United Nations, 2018).

The fragility accompanying the accumulation of trillions of dollars in debt has been compounded by an even larger volume of financial bets through derivatives, and other complex instruments that promised to diminish risk, and were buttressed by the idea that efficient financial markets do not make mistakes. Not only did the profitability of financial institutions rise sharply on the back of this lending activity, but non-financial firms also became increasingly dependent on financial activities for their revenue flows. Governments – whose own revenue flows were being squeezed by a combination of slow wage growth and tax cuts – also increased their lending. In this new debt-led growth model, it is the financial markets and its associated financial leverage that drive the real economy, evident in changes in consumption and investment trends. Consumption behaviour has become tied to rising asset prices and access to credit, and, at the firm level, rising profits have been channelled towards short-term investments, including buying other companies and their own shares on a massive scale.

The mushrooming of mostly short-term, cross-border capital flows from the early 1990s failed to generate the levels of capital formation associated with the 1970s. Those who promote globalization claim that the spread of competitive markets, increased flows of foreign direct investment and advances in information and communication technology, have, since the collapse of the Union of Soviet Socialist Republics, resulted in a massive increase in global welfare. Expanding trade and advances in communications have certainly been important in connecting and shrinking the world over the past 30 years, indeed, in making parts of that world more prosperous. However, these were also features of the post-war era of regulated market capitalism and the accompanying pattern of partial globalization. What distinguishes the last three decades of economic change, at the global as well as the national levels, is the dominant role of financial markets, activities and innovation, or what has been termed “financialization”, in generating a “hyperglobalized” world economy (UNCTAD, 2017a).

While there is no simple definition of financialization, commentators point to rising cross-border capital flows, the explosion of bank assets and the increasing proportion of national income accruing to the financial sector. It is a process whereby financial markets, financial institutions and financial elites have gained influence over economic policy and outcomes. It involves a structural shift in the organization of economic activity, along with changes to economic and political behaviour, which together have altered the way in which income is produced, distributed and consumed. Financial innovation has come to rival technological innovation as a focus for entrepreneurial energies, and the rights of the owners of financial assets have trumped those of other economic actors and have at times escaped social and even judicial accountability.

Moreover, the validation of policies (and not just economic policies) seems to come from reference to market interests, measured by performance indicators devised, managed and endorsed by the financial institutions themselves, including stock prices, credit ratings, returns from real estate investments, quarterly earnings, the scale of mergers and acquisitions, etc. Stiglitz (2016, p. 423) refers to the process by which the financial institutions use their dominance and power to get special treatment from regulators (including bailouts, direct injections, propping up the mortgage market, etc.) as rent-seeking behaviour. The rents extracted are paid out as dividends to shareholders and as bonuses to management, as earned income – rather than investment income – and are ascribed to individual performance. In economies where this has been most extreme, such as the United States of America, 95 per cent of income gains since 2009 have been captured by the top 1 per cent (ibid., 2015, p. 120). This is the world of “superstar” earnings of executives and senior managers where gains from financialized growth spurts and boom conditions have been captured on a scale that would have been impossible, or even conceivable, under more regulated financial structures barely a generation ago (Piketty, 2015).

Financialization has taken place in the context of three decades of “hyperglobalization” – the combined and continuous deregulation of financial, labour and product markets at global levels – that have given rise to structural shifts in the relations between States and large corporations, and a new breed of corporate rentierism (UNCTAD, 2017a). Rent-seeking corporates intent on predatory extraction have successfully lobbied to influence key national and regional regulatory policy frameworks that affect development outcomes – including intellectual property rights, investment policies, taxation issues and, of course, development financing. Keynes famously anticipated “the euthanasia of the rentier”, which he described as “the cumulative oppressive power of the capitalist to exploit the scarcity value of capital”, a power which he viewed as functionless. Keynes optimistically assumed that a monetary policy of low long-term interest rates, in combination with a gradual socialization of investment, would create a large enough capital stock to make rental (fixed) income from capital non-viable. However, more recent discourse has identified a new generation of rentiers emerging from the financial sector, in which corporate “looting” is the game in town. The extraction of value and market manipulation of companies by senior management for their own gain has been described at least since the savings and loans crisis in the United States (see Akerlof and Roemer, 1993).

There is mounting evidence that firms in developed economies, but also in some emerging economies, are diverting profits away from reinvestment and into dividend payments, share buy-backs and acquisitions in order to raise share prices and reward senior management (Lazonick, 2014; UNCTAD, 2016). Galbraith (2014, p. 160) argues that firms employing predatory strategies “can quickly come to dominate markets, using their apparent financial success to attract capital, boost market valuation, and expand through mergers and acquisitions”. Seen from this perspective, it is possible to describe contemporary financialization as a new mode of social regulation that strives to subject everyone – from pensioners in advanced economies to the ‘deserving’ poor in developing countries – to the private logic of financial risk management (Storm, 2018). Rather than describing a relatively benign situation where markets have moved closer towards deregulation on some kind of regulation continuum, financialization should be seen as a core obstacle, preventing the recovery of a degree of public policy coordination at the regional, national and international levels, to mobilize both public and private financial resources for structural transformation in developing countries in a stable and reliable manner (Kozul-Wright, 2019)

The fragility accompanying the accumulation of trillions of dollars in debt has been compounded by an even larger volume of financial bets through derivatives, and other complex instruments that promised to diminish risk, and were buttressed by the idea that efficient financial markets do not make mistakes. Not only did the profitability of financial institutions rise sharply on the back of this lending activity, but non-financial firms also became increasingly dependent on financial activities for their revenue flows. Governments – whose own revenue flows were being squeezed by a combination of slow wage growth and tax cuts – also increased their lending. In this new debt-led growth model, it is the financial markets and its associated financial leverage that drive the real economy, evident in changes in consumption and investment trends. Consumption behaviour has become tied to rising asset prices and access to credit, and, at the firm level, rising profits have been channelled towards short-term investments, including buying other companies and their own shares on a massive scale.

The mushrooming of mostly short-term, cross-border capital flows from the early 1990s failed to generate the levels of capital formation associated with the 1970s. Those who promote globalization claim that the spread of competitive markets, increased flows of foreign direct investment and advances in information and communication technology, have, since the collapse of the Union of Soviet Socialist Republics, resulted in a massive increase in global welfare. Expanding trade and advances in communications have certainly been important in connecting and shrinking the world over the past 30 years, indeed, in making parts of that world more prosperous. However, these were also features of the post-war era of regulated market capitalism and the accompanying pattern of partial globalization. What distinguishes the last three decades of economic change, at the global as well as the national levels, is the dominant role of financial markets, activities and innovation, or what has been termed “financialization”, in generating a “hyperglobalized” world economy (UNCTAD, 2017a).

While there is no simple definition of financialization, commentators point to rising cross-border capital flows, the explosion of bank assets and the increasing proportion of national income accruing to the financial sector. It is a process whereby financial markets, financial institutions and financial elites have gained influence over economic policy and outcomes. It involves a structural shift in the organization of economic activity, along with changes to economic and political behaviour, which together have altered the way in which income is produced, distributed and consumed. Financial innovation has come to rival technological innovation as a focus for entrepreneurial energies, and the rights of the owners of financial assets have trumped those of other economic actors and have at times escaped social and even judicial accountability.

Moreover, the validation of policies (and not just economic policies) seems to come from reference to market interests, measured by performance indicators devised, managed and endorsed by the financial institutions themselves, including stock prices, credit ratings, returns from real estate investments, quarterly earnings, the scale of mergers and acquisitions, etc. Stiglitz (2016, p. 423) refers to the process by which the financial institutions use their dominance and power to get special treatment from regulators (including bailouts, direct injections, propping up the mortgage market, etc.) as rent-seeking behaviour. The rents extracted are paid out as dividends to shareholders and as bonuses to management, as earned income – rather than investment income – and are ascribed to individual performance. In economies where this has been most extreme, such as the United States of America, 95 per cent of income gains since 2009 have been captured by the top 1 per cent (ibid., 2015, p. 120). This is the world of “superstar” earnings of executives and senior managers where gains from financialized growth spurts and boom conditions have been captured on a scale that would have been impossible, or even conceivable, under more regulated financial structures barely a generation ago (Piketty, 2015).

Financialization has taken place in the context of three decades of “hyperglobalization” – the combined and continuous deregulation of financial, labour and product markets at global levels – that have given rise to structural shifts in the relations between States and large corporations, and a new breed of corporate rentierism (UNCTAD, 2017a). Rent-seeking corporates intent on predatory extraction have successfully lobbied to influence key national and regional regulatory policy frameworks that affect development outcomes – including intellectual property rights, investment policies, taxation issues and, of course, development financing. Keynes famously anticipated “the euthanasia of the rentier”, which he described as “the cumulative oppressive power of the capitalist to exploit the scarcity value of capital”, a power which he viewed as functionless. Keynes optimistically assumed that a monetary policy of low long-term interest rates, in combination with a gradual socialization of investment, would create a large enough capital stock to make rental (fixed) income from capital non-viable. However, more recent discourse has identified a new generation of rentiers emerging from the financial sector, in which corporate “looting” is the game in town. The extraction of value and market manipulation of companies by senior management for their own gain has been described at least since the savings and loans crisis in the United States (see Akerlof and Roemer, 1993).

There is mounting evidence that firms in developed economies, but also in some emerging economies, are diverting profits away from reinvestment and into dividend payments, share buy-backs and acquisitions in order to raise share prices and reward senior management (Lazonick, 2014; UNCTAD, 2016). Galbraith (2014, p. 160) argues that firms employing predatory strategies “can quickly come to dominate markets, using their apparent financial success to attract capital, boost market valuation, and expand through mergers and acquisitions”. Seen from this perspective, it is possible to describe contemporary financialization as a new mode of social regulation that strives to subject everyone – from pensioners in advanced economies to the ‘deserving’ poor in developing countries – to the private logic of financial risk management (Storm, 2018). Rather than describing a relatively benign situation where markets have moved closer towards deregulation on some kind of regulation continuum, financialization should be seen as a core obstacle, preventing the recovery of a degree of public policy coordination at the regional, national and international levels, to mobilize both public and private financial resources for structural transformation in developing countries in a stable and reliable manner (Kozul-Wright, 2019)

Worsening debt vulnerability of developing countries

Analysis of debt indicators of developing countries is confounded by poor data availability, quality and country coverage of different debt components and debt financing instruments. Improvement of such data remains an urgent priority, not only to better assess the short- and long-term sustainability of developing country debt, but also to improve debt management strategies and facilitate sovereign debt restructurings. This said, the debt indicators currently available for developing countries support the narrative presented in section I in the following ways:

• Debt stocks have grown over 8 per cent per annum over the past decade and now represent more than 25 per cent of GDP for all developing countries. The growth of the indebtedness of sub-Saharan Africa is of concern.

• High accumulated reserves show the vulnerability of developing countries to outflows and represent forgone opportunities to undertake development investment.

• Debt stocks are multiples of export earnings and debt servicing absorbs almost 14 per cent of export earnings on average.

• Private non-financial corporate sector debt makes up an increasing share of debt.

• Growth of developing country regions remains highly variable and on a downward trend.

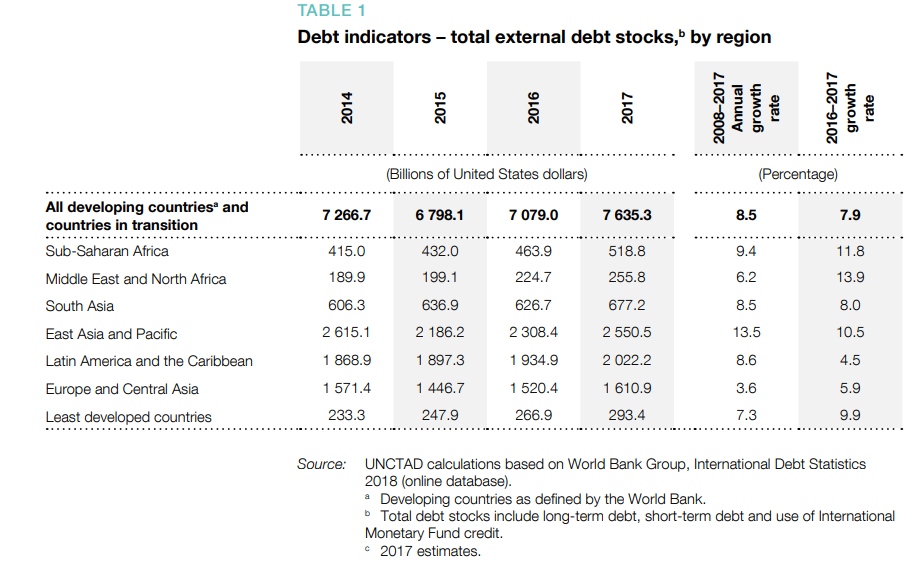

In aggregate terms, the debt owed by developing countries and countries in transition has grown by 8.5 per cent per annum since 2008–2017. Table 1 shows that debt stocks have grown across the board for developing countries and countries in transition across all regions. The annual growth of debt stocks in the East Asia and the Pacific region (13.5 per cent) and sub-Saharan Africa (9.4 per cent) has outstripped the average annual growth for all developing countries over this period. The former region notably includes China, a country whose share of total developing country debt stock increased from 11.5 per cent in 2009 to 21 per cent in 2017 (United Nations, 2018). It is notable that the sub-Saharan region includes 30 of the 36 countries that have benefited from the Heavily Indebted Poor Countries Debt Initiative and the Multilateral Debt Relief Initiative. These initiatives have been successful to the extent that they have reduced debt stocks, made debt servicing as a percentage of GDP more manageable and allowed slightly stimulatory GDP expenditure (International Monetary Fund, 2016). While it was always expected that countries emerging from the abovementioned initiatives would grow their debt again – given the realities of their own development demands and low tax bases – the speed with which the debt has grown has outstripped expectations.

Developing countries have expanded and opened their domestic financial markets to non-resident investors, foreign commercial banks and financial institutions prematurely: they have allowed their citizens to invest abroad and, as mentioned, many developing country Governments are engaged in raising finance in developed country financial markets. The rising indebtedness of developing countries has increased vulnerability and undermined growth prospects – capital inflows have led to exchange rate appreciation, which reduces competitiveness of the domestic industry (Kregel, 2018) and rising reserve accumulation means opportunity forgone in terms of much-needed investment and social expenditure (Elhiraika and Ndikumana, 2007).

• Debt stocks have grown over 8 per cent per annum over the past decade and now represent more than 25 per cent of GDP for all developing countries. The growth of the indebtedness of sub-Saharan Africa is of concern.

• High accumulated reserves show the vulnerability of developing countries to outflows and represent forgone opportunities to undertake development investment.

• Debt stocks are multiples of export earnings and debt servicing absorbs almost 14 per cent of export earnings on average.

• Private non-financial corporate sector debt makes up an increasing share of debt.

• Growth of developing country regions remains highly variable and on a downward trend.

In aggregate terms, the debt owed by developing countries and countries in transition has grown by 8.5 per cent per annum since 2008–2017. Table 1 shows that debt stocks have grown across the board for developing countries and countries in transition across all regions. The annual growth of debt stocks in the East Asia and the Pacific region (13.5 per cent) and sub-Saharan Africa (9.4 per cent) has outstripped the average annual growth for all developing countries over this period. The former region notably includes China, a country whose share of total developing country debt stock increased from 11.5 per cent in 2009 to 21 per cent in 2017 (United Nations, 2018). It is notable that the sub-Saharan region includes 30 of the 36 countries that have benefited from the Heavily Indebted Poor Countries Debt Initiative and the Multilateral Debt Relief Initiative. These initiatives have been successful to the extent that they have reduced debt stocks, made debt servicing as a percentage of GDP more manageable and allowed slightly stimulatory GDP expenditure (International Monetary Fund, 2016). While it was always expected that countries emerging from the abovementioned initiatives would grow their debt again – given the realities of their own development demands and low tax bases – the speed with which the debt has grown has outstripped expectations.

Developing countries have expanded and opened their domestic financial markets to non-resident investors, foreign commercial banks and financial institutions prematurely: they have allowed their citizens to invest abroad and, as mentioned, many developing country Governments are engaged in raising finance in developed country financial markets. The rising indebtedness of developing countries has increased vulnerability and undermined growth prospects – capital inflows have led to exchange rate appreciation, which reduces competitiveness of the domestic industry (Kregel, 2018) and rising reserve accumulation means opportunity forgone in terms of much-needed investment and social expenditure (Elhiraika and Ndikumana, 2007).

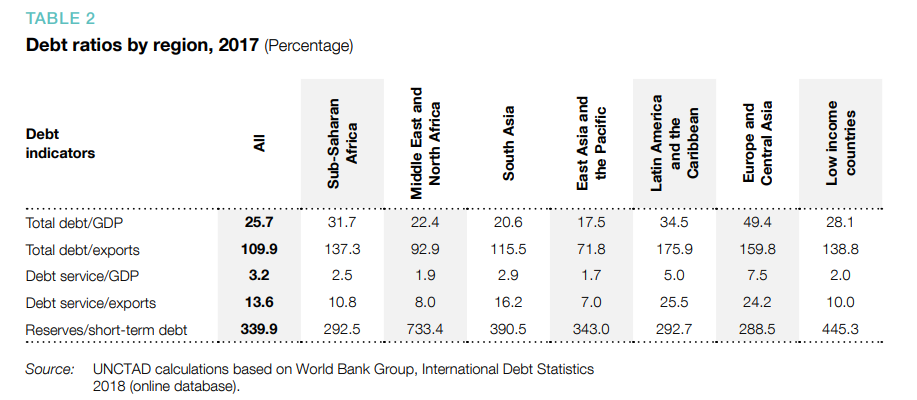

Taken together, tables 1 and 2 show that countries in East Asia and the Pacific and in Latin America and the Caribbean hold the greatest aggregate debt of developing regions. However, when compared with GDP, debt in East Asia and the Pacific accounts for a relatively low 17.5 per cent of GDP, but for 34.5 per cent in Latin American and the Caribbean. East Asia and the Pacific (17.5 per cent), South Asia (20.6 per cent) and the Middle East and North Africa (22.4 per cent) are the only regions whose debt to GDP ratio is below the average for all developing countries of 25.7 per cent. The debt to GDP ratios for sub-Saharan Africa, Latin America and the Caribbean and Europe and Central Asia exceed 30 per cent. The ratios in table 2 reveal that debt stocks are greater than export earnings in all regions (total debt/exports > 100 per cent) except East Asia and the Pacific (including China) and the Middle East and North Africa. While, on average, the debt servicing to exports is 13.6 per cent for all developing countries, it is 10 per cent or higher for low-income developing countries and sub-Saharan Africa, and above 20 per cent for Latin America and the Caribbean and for Europe and Central Asia. For all regions, reserves are close to, or more than three times higher than, short-term debt stocks. High reserve levels are a consequence of several factors but can be seen as a precaution against hot flows out of a country leading to currency crises. The level of reserves reveals the perception of risk and the extent to which policies in a given country are dominated by short-term concerns about “firefighting” immediate liquidity constraints and by the diversion of much-needed development finance to hedge against such liquidity risks through the build-up of substantive international reserves (Blankenburg, 2018). There is some speculation as to whether developing countries are holding excessive reserves (see, for example, Elhiraika and Ndikumana, 2007; Park and Estrada, 2009; Dadush and Stancil, 2011) but, in all cases, they represent costs to the countries involved. These reserves could, at the very least, be invested more actively, but importantly, they could also be more effectively spent on investment and social needs.

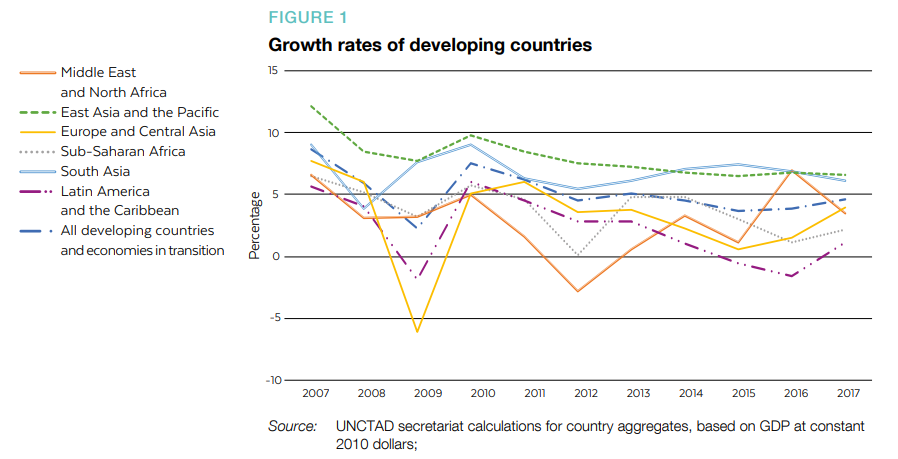

Figure 1 provides an aggregated view of growth for all developing countries and by region. The swings in the data from year to year suggest exposure to external shocks associated with export prices, cross-border capital flows and external debt service burdens, which are largely determined by policy decisions in advanced economies. There is little evidence that developing country reliance on financial and trade openness has generated the higher growth paths promised: instead, the data suggest gradual convergence to lower, rather than higher, growth rates for developing countries.

With financial globalization, economists have stressed the importance of “push factors” – mainly changes to global liquidity and risk – as the main determinants of surges and reversals in capital flows, giving “pull factors”, i.e. country-specific factors and demand, only a secondary role. Global factors act as “gatekeepers”, whereas “pull factors” – in particular, the foreign exchange regime – explain different degrees of exposure to changes in global conditions and the final magnitude of the surge in particular countries (Fernández-Arias, 1996; Cerutti et al., 2015).

As global debt stocks of developing countries have risen, the composition of longterm debt has changed. Data for long-term debt – defined as debt that has an original or extended maturity of more than one year and that is owed to nonresidents by residents of an economy and repayable in foreign currency, goods or services – is typically divided into public (and publicly guaranteed) debt and private debt. Figure 2 shows that public debt clearly outstripped private sector debt at the turn of the century, but the private debt share has gradually increased, meaning that, by 2008, the two types of debt were at roughly the same level and have been ever since. Private sector debt of all developing countries, including China, amounted to 53.4 per cent of total debt stocks in 2017; with China excluded, that figure stands at 50 per cent.

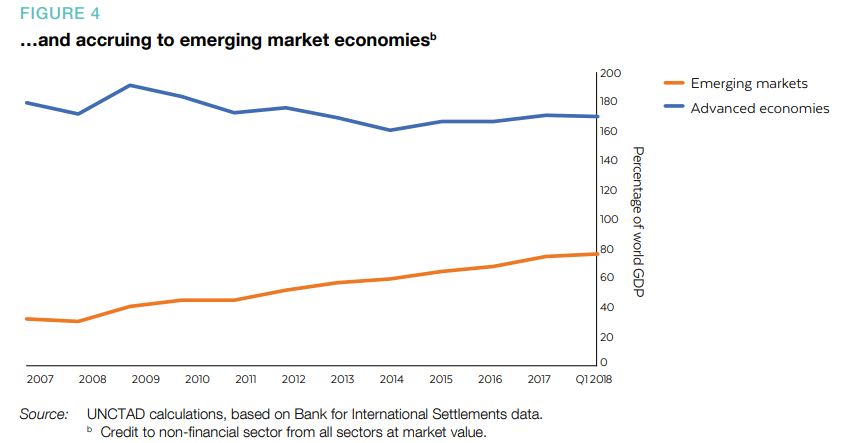

In particular, non-financial corporate debt in emerging markets rose to above 40 per cent of world GDP in 2009 and has grown steadily ever since (see figure 4). By the first quarter of 2018, private non-financial debt in emerging markets had grown to 80 per cent of global GDP. This emphasizes the extent to which emerging market have absorbed liquidity and grown their debt relative to advanced countries, whose non-financial debt has declined to some extent since 2009, when it peaked at 190 per cent of world GDP, to nearly 170 per cent of world GDP by the first quarter of 2018.

As global debt stocks of developing countries have risen, the composition of longterm debt has changed. Data for long-term debt – defined as debt that has an original or extended maturity of more than one year and that is owed to nonresidents by residents of an economy and repayable in foreign currency, goods or services – is typically divided into public (and publicly guaranteed) debt and private debt. Figure 2 shows that public debt clearly outstripped private sector debt at the turn of the century, but the private debt share has gradually increased, meaning that, by 2008, the two types of debt were at roughly the same level and have been ever since. Private sector debt of all developing countries, including China, amounted to 53.4 per cent of total debt stocks in 2017; with China excluded, that figure stands at 50 per cent.

In particular, non-financial corporate debt in emerging markets rose to above 40 per cent of world GDP in 2009 and has grown steadily ever since (see figure 4). By the first quarter of 2018, private non-financial debt in emerging markets had grown to 80 per cent of global GDP. This emphasizes the extent to which emerging market have absorbed liquidity and grown their debt relative to advanced countries, whose non-financial debt has declined to some extent since 2009, when it peaked at 190 per cent of world GDP, to nearly 170 per cent of world GDP by the first quarter of 2018.

A more balanced growth strategy in developing countries inevitably implies using a wide range of policy instruments to manage internal and external integration. Policy space is, therefore, critical. UNCTAD has been concerned for some time about how policy choices, often promoted as the irresistible consequence of globalization, have been reducing that space. To counter this trend, the developmental State has a key role in guaranteeing and employing the policy space needed to manage integration in a way that is sustainable and inclusive (Kozul-Wright, 2019). The slow growth that has accompanied financialization reflects persistent downward pressure on aggregate demand, income and employment, combined with systemic financial fragility and recurrent instability. Raising aggregate demand is, from this perspective, a policy priority for the short term and the long term, with investment demand playing a key bridging role, combined with the reform of a financial system that has become obsessed with short-term, rent-seeking behaviour. Policy prescriptions can be grouped along three fronts:

• First, boosting effective demand: If maintained for a sufficiently long period and calibrated towards expenditures with the greatest impact, expansionary fiscal policy can have a substantial and self-sustained effect on rising consumer and investment demand. In the process, government revenues will rise and the pace of public spending could be eased as private spending resumes. Credit expansion should also be channelled towards sustaining real investment.

• Second, boosting labour incomes: labour incomes need to be boosted so that households can sustain a higher level of consumption without adding to household debt. This will include raising the minimum wage to correct for real declines over the past decades, aligning average wage rises with productivity growth and expanding training and higher education programmes.

• Third, financial reform and reregulation: the need for reform to ensure that financial markets better serve the real economy by realigning incentives, clamping down on toxic financial products, curtailing the power of bloated financial institutions and reregulating areas that have been left to the markets, and strengthening the enforcement and supervisory role of regulators.

Recognizing that the main obstacle to sustained growth presently lies on the demand side should not lead to a disregard of the need to expand and modernize production associated with supply side “structural” policies. Some policies aimed at enhancing demand are structural in nature, for instance: strengthening social security systems; creating minimum income schemes; introducing more progressive taxation rules; improving labour rights; and establishing wage negotiations procedures. In addition, these policies encourage real investment because they provide firms with a long-term expectation of expanding demand, without which they would not have the incentive to invest.

Conversely, some supply side policies aimed at expanding the profitability of firms and, consequently, their investment (for example, wage compression) have negative impacts on demand and, therefore, on investment decisions. Ignoring the linkages between supply and demand policies may, therefore, lead to self-defeating outcomes. Raising aggregate demand requires that spending programmes in support of development be properly financed using multiple sources. The availability of sufficient appropriate financing instruments and capacity is a potential constraint. However, a more fundamental issue is that of putting that capacity into the hands of agents wishing to undertake long-term investment projects that generate large positive externalities and therefore encourage rising productivity and incomes and induce further investments. In order to avoid the risk of government spending creating sovereign debt pressures, debt financing should be limited in the medium term to the level of expenditure for public investment.

Borrowing in a foreign currency, in turn, should be limited to meeting a country’s actual foreign exchange needs (for capital goods, materials, technology, etc.) or for necessary foreign exchange reserves. Caution is the key word. While bank credit is another major instrument to finance investment, private banks are seldom willing to undertake the risks associated with large-scale projects of long maturation. By contrast, development banks are, by design, appropriate institutions to provide long-term finance and to address market failures. They have a clear mandate to support developmentally oriented projects, a funding base whose liabilities are predominately long term and equity, which is for the most part owned by highly rated sovereigns. For this reason, development banks are able to borrow long term in the international financial markets at relatively low costs (Kozul-Wright, 2019). As is clear from the discussion above, debt sustainability of developing countries is hardly in the hands of the affected sovereigns. In an environment of fragility and spillovers, things can turn ugly against the backdrop of falling commodity prices and weakening growth in developed economies.

If monetary policy decisions in advanced economies suddenly drive up borrowing costs, debt burdens that seemed reasonable under favourable conditions can quickly become unsustainable debt in emerging markets and other developing countries. The procyclical nature of capital flows – cheap during a boom and expensive during downturns – is not the only drawback. Once a crisis looms, currency devaluations to improve export prospects simultaneously increase the value of foreign currency denominated debt. For commodity exporters, the need to meet rising debt servicing requirements also generates pressures to continue to produce, potentially worsening excess supply constraints and downward pressures on commodity prices (Akyüz, 2016). In this environment, debt sustainability is largely about the perceived fragility of developing countries and their ability to withstand external shocks. Scaling up of development finance efforts is, therefore, closely linked to the need to reduce, as much as possible, the exposure of developing countries to external shocks, crossborder capital flows and external debt service burdens.

• First, boosting effective demand: If maintained for a sufficiently long period and calibrated towards expenditures with the greatest impact, expansionary fiscal policy can have a substantial and self-sustained effect on rising consumer and investment demand. In the process, government revenues will rise and the pace of public spending could be eased as private spending resumes. Credit expansion should also be channelled towards sustaining real investment.

• Second, boosting labour incomes: labour incomes need to be boosted so that households can sustain a higher level of consumption without adding to household debt. This will include raising the minimum wage to correct for real declines over the past decades, aligning average wage rises with productivity growth and expanding training and higher education programmes.

• Third, financial reform and reregulation: the need for reform to ensure that financial markets better serve the real economy by realigning incentives, clamping down on toxic financial products, curtailing the power of bloated financial institutions and reregulating areas that have been left to the markets, and strengthening the enforcement and supervisory role of regulators.

Recognizing that the main obstacle to sustained growth presently lies on the demand side should not lead to a disregard of the need to expand and modernize production associated with supply side “structural” policies. Some policies aimed at enhancing demand are structural in nature, for instance: strengthening social security systems; creating minimum income schemes; introducing more progressive taxation rules; improving labour rights; and establishing wage negotiations procedures. In addition, these policies encourage real investment because they provide firms with a long-term expectation of expanding demand, without which they would not have the incentive to invest.

Conversely, some supply side policies aimed at expanding the profitability of firms and, consequently, their investment (for example, wage compression) have negative impacts on demand and, therefore, on investment decisions. Ignoring the linkages between supply and demand policies may, therefore, lead to self-defeating outcomes. Raising aggregate demand requires that spending programmes in support of development be properly financed using multiple sources. The availability of sufficient appropriate financing instruments and capacity is a potential constraint. However, a more fundamental issue is that of putting that capacity into the hands of agents wishing to undertake long-term investment projects that generate large positive externalities and therefore encourage rising productivity and incomes and induce further investments. In order to avoid the risk of government spending creating sovereign debt pressures, debt financing should be limited in the medium term to the level of expenditure for public investment.

Borrowing in a foreign currency, in turn, should be limited to meeting a country’s actual foreign exchange needs (for capital goods, materials, technology, etc.) or for necessary foreign exchange reserves. Caution is the key word. While bank credit is another major instrument to finance investment, private banks are seldom willing to undertake the risks associated with large-scale projects of long maturation. By contrast, development banks are, by design, appropriate institutions to provide long-term finance and to address market failures. They have a clear mandate to support developmentally oriented projects, a funding base whose liabilities are predominately long term and equity, which is for the most part owned by highly rated sovereigns. For this reason, development banks are able to borrow long term in the international financial markets at relatively low costs (Kozul-Wright, 2019). As is clear from the discussion above, debt sustainability of developing countries is hardly in the hands of the affected sovereigns. In an environment of fragility and spillovers, things can turn ugly against the backdrop of falling commodity prices and weakening growth in developed economies.

If monetary policy decisions in advanced economies suddenly drive up borrowing costs, debt burdens that seemed reasonable under favourable conditions can quickly become unsustainable debt in emerging markets and other developing countries. The procyclical nature of capital flows – cheap during a boom and expensive during downturns – is not the only drawback. Once a crisis looms, currency devaluations to improve export prospects simultaneously increase the value of foreign currency denominated debt. For commodity exporters, the need to meet rising debt servicing requirements also generates pressures to continue to produce, potentially worsening excess supply constraints and downward pressures on commodity prices (Akyüz, 2016). In this environment, debt sustainability is largely about the perceived fragility of developing countries and their ability to withstand external shocks. Scaling up of development finance efforts is, therefore, closely linked to the need to reduce, as much as possible, the exposure of developing countries to external shocks, crossborder capital flows and external debt service burdens.