|

About Paul:

|

Nu-World: The Old Guard continues to perform

Today I attended the Nu-World (NWL) AGM at their head office in Wynberg near Sandton. The office is a no-frills warehouse complex from the 1980’s and probably dates back to the time of the company’s listing in 1987. The CEO and chairman, the Goldberg brothers, both also date back to the listing and have therefore been at the helm for 32 years. As they listed at R1/share and are now trading at around R44/share and paying dividends over R3/share, they have created significant shareholder value over the period.

The business, like the AGM, is an unpretentious affair. No-one wears ties, the muffins are from Shoprite, “not those fancy Woolworth things”, in the words of the CEO, Jeff Goldberg. The meeting took place surrounded by fans, toasters, fridges and various other household appliances that the company distributes and warehouses.

In the current environment of constrained consumers and high unemployment, it could be expected that a company selling fast moving consumer goods would struggle. However, Nu-World’s EPS and dividends per share were both up strongly in the 2018 Financial Year.

Let’s face it, when our fridge, TV, fan or washing machine break, we have to get a new one. These are essentially non-discretionary items, once we have become accustomed to them. Nu-World, as a distributor, are ambivalent as to how we buy these items. Whether on Flipkart in India, Amazon in Australia or at Makro in South Africa, they make their margin on the importation and distribution.

The company is also sheltered from the South African economy, as 25% of the turnover and 38% of income now comes from outside South Africa. Fast growing markets of India and South America are in the mix and management expects offshore contributions to increase further in the future.

Despite the defensive nature of this business and the strong growth in earnings against the odds, the company trades at extremely attractive multiples. Its PE is 5, it pays 7.5% dividends and trades at a discount to the NAV of R52.35. The company is virtually ungeared. Management owns approximately 10%.

I confronted management with the very poor cash conversion of the business, where in 2018 cashflow was negative and most profits were consumed by Working Capital and remained in Inventory. They assured me that measures were being implemented to reverse that and we can expect a significant improvement in this regard in the upcoming half-year results.

Another, more longer term, concern is the composition of the board which is entirely composed of older men. As women and young people are more likely to be the end consumer of the company’s products, it is hoped that the board will be strengthened with a few different people, with potentially different opinions in the future. Nevertheless, it is difficult to be too critical of a board and executive management that has created significant value and that continues to have a firm grasp both on the business and the market.

Nu-World has just over 1000 shareholders, most of whom are probably delighted both with the recent increase in share price and the healthy and growing dividend. One of these content shareholders is me. I will be buying more shares after experiencing first hand how management reflects its frugal mindset with its no-frills head office, hands on approach and positive view of the future. At current valuations, the upside looks promising and a 7.5% dividend is a good incentive to wait for this upside to materialise.

Article ends

Follow Paul on Twitter (@klugerpaul) or visit his website at https://businessmusings.co.za/

The business, like the AGM, is an unpretentious affair. No-one wears ties, the muffins are from Shoprite, “not those fancy Woolworth things”, in the words of the CEO, Jeff Goldberg. The meeting took place surrounded by fans, toasters, fridges and various other household appliances that the company distributes and warehouses.

In the current environment of constrained consumers and high unemployment, it could be expected that a company selling fast moving consumer goods would struggle. However, Nu-World’s EPS and dividends per share were both up strongly in the 2018 Financial Year.

Let’s face it, when our fridge, TV, fan or washing machine break, we have to get a new one. These are essentially non-discretionary items, once we have become accustomed to them. Nu-World, as a distributor, are ambivalent as to how we buy these items. Whether on Flipkart in India, Amazon in Australia or at Makro in South Africa, they make their margin on the importation and distribution.

The company is also sheltered from the South African economy, as 25% of the turnover and 38% of income now comes from outside South Africa. Fast growing markets of India and South America are in the mix and management expects offshore contributions to increase further in the future.

Despite the defensive nature of this business and the strong growth in earnings against the odds, the company trades at extremely attractive multiples. Its PE is 5, it pays 7.5% dividends and trades at a discount to the NAV of R52.35. The company is virtually ungeared. Management owns approximately 10%.

I confronted management with the very poor cash conversion of the business, where in 2018 cashflow was negative and most profits were consumed by Working Capital and remained in Inventory. They assured me that measures were being implemented to reverse that and we can expect a significant improvement in this regard in the upcoming half-year results.

Another, more longer term, concern is the composition of the board which is entirely composed of older men. As women and young people are more likely to be the end consumer of the company’s products, it is hoped that the board will be strengthened with a few different people, with potentially different opinions in the future. Nevertheless, it is difficult to be too critical of a board and executive management that has created significant value and that continues to have a firm grasp both on the business and the market.

Nu-World has just over 1000 shareholders, most of whom are probably delighted both with the recent increase in share price and the healthy and growing dividend. One of these content shareholders is me. I will be buying more shares after experiencing first hand how management reflects its frugal mindset with its no-frills head office, hands on approach and positive view of the future. At current valuations, the upside looks promising and a 7.5% dividend is a good incentive to wait for this upside to materialise.

Article ends

Follow Paul on Twitter (@klugerpaul) or visit his website at https://businessmusings.co.za/

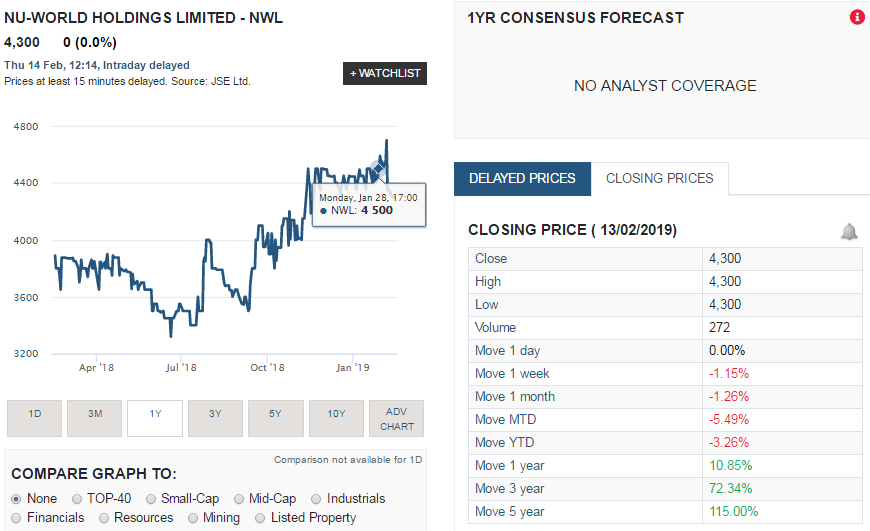

Share price history

The image below, obtained from Sharnet shows the share price performance of Nu-world over the last 12 months as well as the returns it has provided over the last year, 3 years and 5 years. The company has rewarded shareholders handsomely over the long term, but over the shorter term it has struggled slightly. But still a lot better than any of the big retailers in SA had to offer investors recently

Let us know what you thought of this article: |