|

Related Topics |

|

In today's blog we look at one of South Africa's most well known asset managers and financial service providers, PSG Wealth's investment approach, as contained in their Spring 2017, Research and strategy report.

|

|

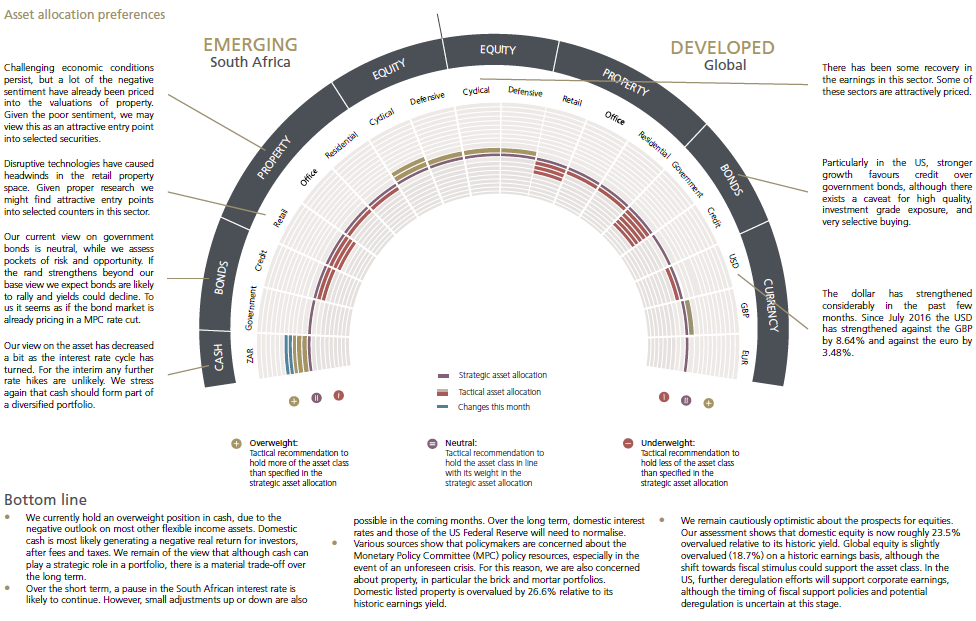

PSG Wealth's Asset Allocation Preferences Wheel

The image below provides a broad summary of PSG's investment strategy when it comes to the local market (South Africa) and other emerging markets compared to the approach they follow when allocation assets in developed countries across the world.

PSG Wealth Investment Strategy

A brief description of the wheel:

Starting at the left it reads Cash, Bonds, Property, Equity. Those are the four main asset classes they investing in, in emerging markets such as South Africa. The colours lower down shows whether PSG is overweight , neutral or underweight in a particular asset class. And blue shows changes during the last month.

Starting at the left it reads Cash, Bonds, Property, Equity. Those are the four main asset classes they investing in, in emerging markets such as South Africa. The colours lower down shows whether PSG is overweight , neutral or underweight in a particular asset class. And blue shows changes during the last month.

From the image it is clear that PSG is overweight in cash in South Africa, neutral in SA government bonds, negative in all types of property (be it Retail, Office or Residential), and overweight in cyclical and defensive equities. PSG being negative in a particular sector does not mean they dont invest in the sector at all, but it implies they are not heavily invested in such sectors and that they dont expect great returns from it over the short to medium term.

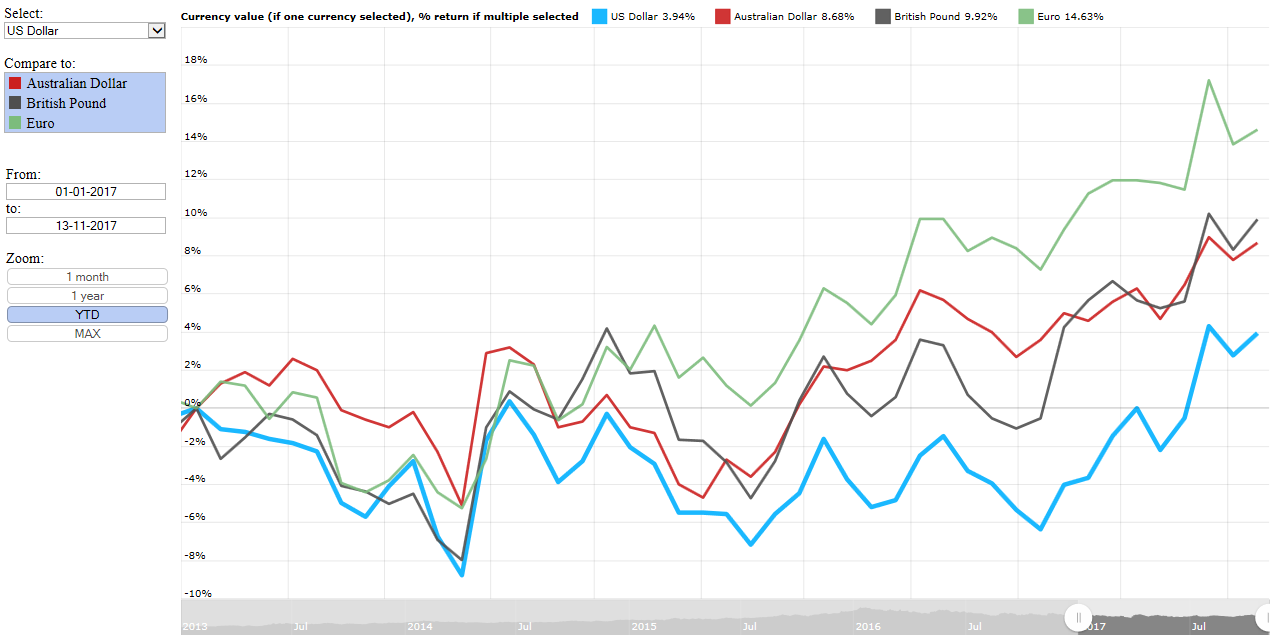

When it comes to the developed world, PSG is exceptionally negative in government bonds and all forms of property (as is the case with South Africa). Interestingly PSG is underweight in US Dollars and overweight in Great British Pounds, perhaps taking advantage of the massive drop in GBP after brexit. And PSG is neutral on Euro's. Interesting to note the Euro has been the best performing currency against the ZAR in 2017 (when looking at Pounds, Dollars and Euro's). See the image below, or visit our exchange rate page.

When it comes to the developed world, PSG is exceptionally negative in government bonds and all forms of property (as is the case with South Africa). Interestingly PSG is underweight in US Dollars and overweight in Great British Pounds, perhaps taking advantage of the massive drop in GBP after brexit. And PSG is neutral on Euro's. Interesting to note the Euro has been the best performing currency against the ZAR in 2017 (when looking at Pounds, Dollars and Euro's). See the image below, or visit our exchange rate page.

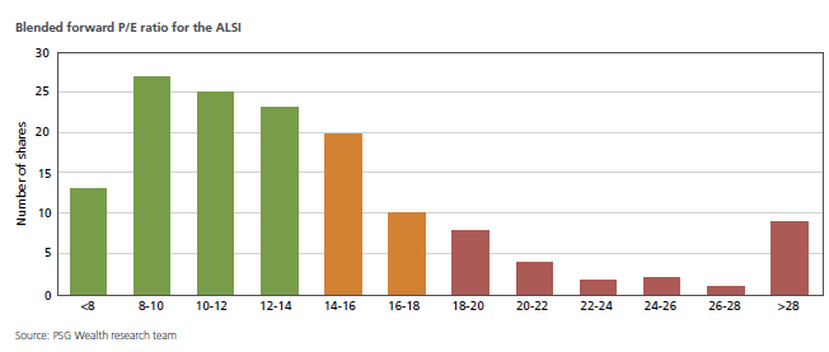

One last graphic we want to take a look at the Price/Earnings Ratio of various companies as listed on the JSE All Share Index (ALSI). The image was also obtained from PSG's Spring report. We take a look at the image below.

According to the image below there is a large cluster of companies listed on the JSE with PE ratios below or equal to 14. Which in most markets and peoples eyes would be deemed relatively cheap, and then there is a small chunk of companies with PE ratios well above 28, which most market commentators would deem as extremely expensive at such high PE ratios.

The problem with those companies with the exceptionally high PE ratio's is the fact that some of them are some of the biggest shares listed on the JSE,and therefore they carry a significant weight in the overall market, and it pushes the overall PE ratio of the ALSI up. As at end of October 2017, the JSE ALSI had a overall PE ratio of 20.5, yet the majority of shares on the JSE trade at PE ratios well below the overall market average.

For more on the markets see www.jse.co.za or for more information from PSG see www.psg.co.za

For more on the markets see www.jse.co.za or for more information from PSG see www.psg.co.za

Let us know what you thought of this article: |