|

Tiger Brands (TBS) interim financial results for the period ending March 2019

Date: 22 May 2018 Category: Stock Market Share price at time of writing: R230.00 We take a look at food producing group Tiger Brands. They own some of South Africa's best known brands in the food and beverages categories. But more recently they are best known for bringing Listeriosis to the masses.

Recently it was announced that there is a class action lawsuit against Tiger Brands by those affected by the Listeria crises at the group. Tiger Brands stated that they will defend against the class action. |

|

Related Topics |

About Tiger Brands

Tiger Brands Limited, a Top 40 JSE Limited company whose footprint extends across the African continent and beyond, is one of the largest manufacturers and marketers of FMCG products in Southern Africa, and has been for several decades. Tiger Brands has been built over many decades through the acquisition and clustering of businesses. Our strategy for success comes from the perpetual renovation and innovation of our brands, while our approach to expansion, acquisitions and joint ventures has given traction to a distribution network that now spans more than 22 African countries. Our group focus is on the core business of FMCG categories that spread across the value chain. Our wide range of brands are underpinned by comprehensive research and meaningful insights into each of the markets in which Tiger Brands operates. Tiger Brands is a world–class operation – and will continue to hold and grow its position through constant investment in every asset of the business, be it in people, brands, technology, efficiency, quality or sustainability.

The groups brands include but are not limited to the following:

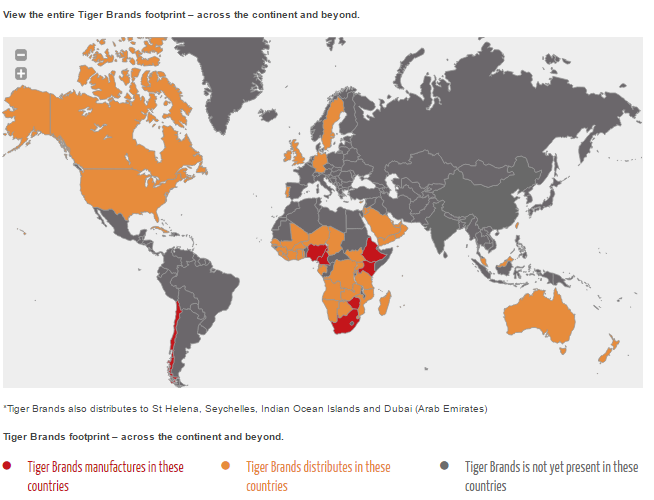

The image below shows Tiger Brands footprint across the African continent and the rest of the world.

The groups brands include but are not limited to the following:

- Energade

- Oros

- Tastic

- Koo

- Purity

- All Gold

- Beacon

- King Korn

- Ace

- All Sorts

- Jelly Tots

- Albany

- Golden Cloud

- Jungle Oats

- Enterprise (The cause of Listeriosis in South Africa)

- Bokkie

- Black Cat

- Maynards

- Fizzer

- Toff-o-luxe

The image below shows Tiger Brands footprint across the African continent and the rest of the world.

Tiger Brands Global Footprint

Financial results

The following was published on the JSE Security Exchange News Syteme (SENS) system earlier today

- Revenue declined by -1.8% to R15.4 billion

- Group operating income increased by 8.3% to R1.738 billion

- Group operating margin: 11,28%

- Headline Eearnings Per Share (HEPS) down 12% to R7.62 per share (placing the group on a PE ratio of 15.1)

- Dividend (R3.21) plus special dividend (R3.06) at R6.27 per share (placing the group on a dividend yield of 4.12% including the special dividend)

- Oceana Group Limited (Oceana) stake was unbundled

- Cash generated from operations: R1.4 billion (or R7.36 a share), down from R1.5 billion in prior period

- Cash and equivalents on the balance sheet: R1.581 billion (or R8.32 a share)

- Inventories: R5.36 billion (up 8.9% from R4.92 billion in prior year)

- Trade and other receivables: R4.57 billion (down 8.4% from R4.99 billion in prior year). This is a good sign for TBS. Shows they managing funds outstanding to them.

- Group equity R17.56 billion (or around R92.53 a share). So trading at 2.48 times its group equity per share.

- Tobin's Q: 1.85 (thus the group's market capital is 1.85 times the value of TBS's total assets)

So it is clear from the revenue numbers and the headline earnings per share numbers above that its been a tough year for the group. Revenues declined, operating margins declined, their headline earnings per share declined, cash generated from operations declined. They have a class action law suite against them which might lead to significant amounts the group needs to pay out. We saw earlier in the week that food producers and distributors are finding the South African market very tough, with Pioneer Foods also reporting that their margins are being squeezed.

Management commentary on the financial results

Tiger Brands delivers a mixed set of results under difficult trading conditions During the period under review, the trading environment remained difficult, with continued pressure on consumer spending, resulting in sales volume increases in the domestic business while low price inflation impacted margins.

Group revenue of R15,4 billion from continuing operations was down 2% compared with the corresponding period last year, which included Easter seasonal volumes. Domestic revenue excluding Value Added Meat Products (VAMP) was 6% higher driven by 2% volume growth and 4% inflation.

Revenue from Exports and International for the period under review declined by 11% to R1,7 billion. This was primarily due to lower Export volumes and price deflation in international markets. Operating income before IFRS 2 charges from continuing operations decreased by 24% to R1,5 billion. This decrease was driven largely by VAMP and Grains, but partially offset by significantly lower losses in Deli Foods and the Deciduous Fruit business. Operating income from continuing operations, excluding VAMP, declined by 9% to R1,8 billion.

Strong volume performances were recorded in Beverages, Home Care, Baby Care, and Groceries, offset by a 1,2% decline in Grains volumes. All categories, except sorghum-based products, maize, pasta and Baby Care recorded selling price inflation. However, price increases were not sufficient to fully recover cost increases, resulting in negative operating leverage. Power outages and social unrest continued to interrupt operations. During the period, goodwill of R100 million in respect of Davita was impaired. This arose as a result of the consistent risks associated with key export markets, with lower sales projected for Nigeria and Mozambique, as well as lower sales forecasted for the powdered seasoning brand, Benny.

On 24 January 2019, Tiger Brands advised shareholders that it had received and accepted a conditional but binding offer from Brimstone Investment Corporation Limited (Brimstone) to acquire 8 000 000 shares in Oceana (Brimstone sale). The Brimstone sale was concluded on 20 March 2019, giving rise to an after-tax capital profit of R282 million. The total abnormal profits of R329 million recorded at the half-year, include the after-tax profit from the Brimstone sale, as well as R100 million in insurance proceeds related to the temporary shutdown of the VAMP facilities last year. These gains were partially offset by costs related to the delayed re-opening of VAMP as well as retrenchment costs in other businesses.

Net financing costs of R26 million (2018: R45 million), reflect a reduction of R19 million compared to the same period last year. This was primarily due to a lower net foreign exchange loss of R6 million in the current period. Income from associates decreased by 41% to R200 million. As previously reported, following the decision to unbundle the company's investment in Oceana, the company ceased to equity account the earnings of Oceana with effect from 1 December 2018. The unbundling was concluded on 29 April 2019, being the implementation date of the unbundling. The total income from associates is therefore not strictly comparable with the corresponding period last year. Excluding the contribution from Oceana in both periods, income from associates reflects an overall improvement on the previous period. Carozzi and UAC Foods produced solid performances, with National Foods Holdings (NFH) performing satisfactorily in the current period.

The ongoing forex liquidity challenges in Zimbabwe have intensified significantly over the last six months. The challenge of trading sustainably in this environment for NFH has been exacerbated by the delays of the Reserve Bank of Zimbabwe in making payments of debts to the major supplier of NFH, which were assumed by the Reserve Bank of Zimbabwe as part of a funding agreement concluded during the period under review. Profit before tax from continuing operations improved marginally to R1,9 billion.

Outlook

We continue to focus on positioning the business for the future and are confident that our strategies remain compelling. Embedding the operating model remains a priority as is driving the cultural transformation that will result in a more agile and flexible organisation. In tandem with the above, we will review processes, structures and overhead costs to identify opportunities that will improve operational efficiencies and reduce our cost base, particularly as selling price inflation across the portfolio is expected to remain low against a backdrop of constrained consumer spending.

Listeria update

Shareholders are referred to the SENS announcement issued by the company on 17 April 2019 with regards to the serving of the Class Action summons. As previously confirmed, the company has product liability insurance cover appropriate for a group of its scale. Coverage is subject to the terms and limits of the policy. Our insurers have advised that the product liability policy does not include cover for exemplary or punitive damages, should such an award be made by the court, and in addition, should an award be made for Constitutional damages, the product liability policy will not cover that portion of the award which relates to exemplary or punitive damages which are not compensatory in nature. The company reserves its rights in this regard. On 2 May 2019, the company filed the required notice with the Registrar of the High Court, Gauteng Local Division, Johannesburg, of its intention to defend the Class Action. When appropriate, it will issue further communication as material milestones in the legal process are reached.

Group revenue of R15,4 billion from continuing operations was down 2% compared with the corresponding period last year, which included Easter seasonal volumes. Domestic revenue excluding Value Added Meat Products (VAMP) was 6% higher driven by 2% volume growth and 4% inflation.

Revenue from Exports and International for the period under review declined by 11% to R1,7 billion. This was primarily due to lower Export volumes and price deflation in international markets. Operating income before IFRS 2 charges from continuing operations decreased by 24% to R1,5 billion. This decrease was driven largely by VAMP and Grains, but partially offset by significantly lower losses in Deli Foods and the Deciduous Fruit business. Operating income from continuing operations, excluding VAMP, declined by 9% to R1,8 billion.

Strong volume performances were recorded in Beverages, Home Care, Baby Care, and Groceries, offset by a 1,2% decline in Grains volumes. All categories, except sorghum-based products, maize, pasta and Baby Care recorded selling price inflation. However, price increases were not sufficient to fully recover cost increases, resulting in negative operating leverage. Power outages and social unrest continued to interrupt operations. During the period, goodwill of R100 million in respect of Davita was impaired. This arose as a result of the consistent risks associated with key export markets, with lower sales projected for Nigeria and Mozambique, as well as lower sales forecasted for the powdered seasoning brand, Benny.

On 24 January 2019, Tiger Brands advised shareholders that it had received and accepted a conditional but binding offer from Brimstone Investment Corporation Limited (Brimstone) to acquire 8 000 000 shares in Oceana (Brimstone sale). The Brimstone sale was concluded on 20 March 2019, giving rise to an after-tax capital profit of R282 million. The total abnormal profits of R329 million recorded at the half-year, include the after-tax profit from the Brimstone sale, as well as R100 million in insurance proceeds related to the temporary shutdown of the VAMP facilities last year. These gains were partially offset by costs related to the delayed re-opening of VAMP as well as retrenchment costs in other businesses.

Net financing costs of R26 million (2018: R45 million), reflect a reduction of R19 million compared to the same period last year. This was primarily due to a lower net foreign exchange loss of R6 million in the current period. Income from associates decreased by 41% to R200 million. As previously reported, following the decision to unbundle the company's investment in Oceana, the company ceased to equity account the earnings of Oceana with effect from 1 December 2018. The unbundling was concluded on 29 April 2019, being the implementation date of the unbundling. The total income from associates is therefore not strictly comparable with the corresponding period last year. Excluding the contribution from Oceana in both periods, income from associates reflects an overall improvement on the previous period. Carozzi and UAC Foods produced solid performances, with National Foods Holdings (NFH) performing satisfactorily in the current period.

The ongoing forex liquidity challenges in Zimbabwe have intensified significantly over the last six months. The challenge of trading sustainably in this environment for NFH has been exacerbated by the delays of the Reserve Bank of Zimbabwe in making payments of debts to the major supplier of NFH, which were assumed by the Reserve Bank of Zimbabwe as part of a funding agreement concluded during the period under review. Profit before tax from continuing operations improved marginally to R1,9 billion.

Outlook

We continue to focus on positioning the business for the future and are confident that our strategies remain compelling. Embedding the operating model remains a priority as is driving the cultural transformation that will result in a more agile and flexible organisation. In tandem with the above, we will review processes, structures and overhead costs to identify opportunities that will improve operational efficiencies and reduce our cost base, particularly as selling price inflation across the portfolio is expected to remain low against a backdrop of constrained consumer spending.

Listeria update

Shareholders are referred to the SENS announcement issued by the company on 17 April 2019 with regards to the serving of the Class Action summons. As previously confirmed, the company has product liability insurance cover appropriate for a group of its scale. Coverage is subject to the terms and limits of the policy. Our insurers have advised that the product liability policy does not include cover for exemplary or punitive damages, should such an award be made by the court, and in addition, should an award be made for Constitutional damages, the product liability policy will not cover that portion of the award which relates to exemplary or punitive damages which are not compensatory in nature. The company reserves its rights in this regard. On 2 May 2019, the company filed the required notice with the Registrar of the High Court, Gauteng Local Division, Johannesburg, of its intention to defend the Class Action. When appropriate, it will issue further communication as material milestones in the legal process are reached.

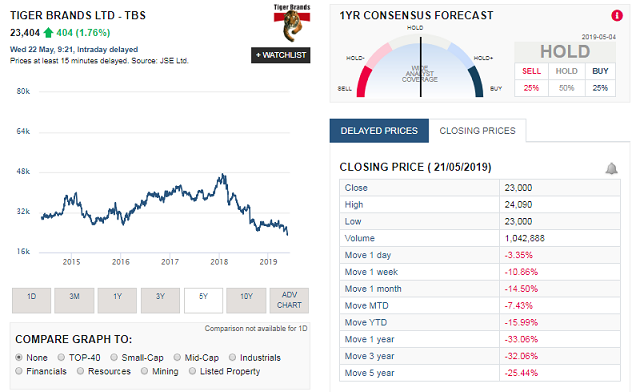

Tiger Brands (TBS) share price history

The image below, taken from Sharenet shows Tiger Brands' share price performance over the last 5 years, and the graphic clearly shows that TBS has done little to please investors in the group over the last 5 years.

The summary below shows the share price returns of Tiger Brands over various time periods:

- 1 week: -10.86%

- 1 month: -14.5%

- Year to Date (YTD): -15.99%

- 1 Year: -33.06%

- 3 Years: -32.06%

- 5 Years: -25.44%

Tiger Brands (TBS) share valuation

So should you buy Tiger Brands shares? Well they are trading at a relatively stiff PE ratio, they not trading at the highest dividend yield around either, with their dividend yield being just over 4% (and that includes the special dividend announced in this set of results) . While their net profit margin of around 9.37% is pretty healthy, the concerns regarding the class action against the group lingers. While the worst of the impact of the listeriosis outbreak one can assume is past Tiger Brands, one wonders if they will be able to win back the trust of consumers. In particular the brand assigned to the whole saga which is Enterprise.

The group has a very strong balance sheet, good cash generation and has managed to keep their trade and other receivables in check during difficult economic times. Based on their results we value the group at R251 a share, down from the R280 valuation we had on the group based on their previous set of full year results. We also saw a mark down in our target price of their rival Pioneer Foods recently. Share valuations currently reflects the latest results and operating environments and future prospects.

So at their current price they offer a bit of value to those willing to take the risk of buying and holding before the class action outcome. At this point in time if an investor wants to get into the food production and sales category, we would recommend Pioneer Foods ahead of Tiger Brands based on both's financial results published recently.

So at their current price they offer a bit of value to those willing to take the risk of buying and holding before the class action outcome. At this point in time if an investor wants to get into the food production and sales category, we would recommend Pioneer Foods ahead of Tiger Brands based on both's financial results published recently.