|

Related Topics |

|

We take a look at the final results of listed general retail group Spar for the period ending September 2018. And the group broke the R100 billion revenue barrier for the financial year.

|

|

About SPAR Group

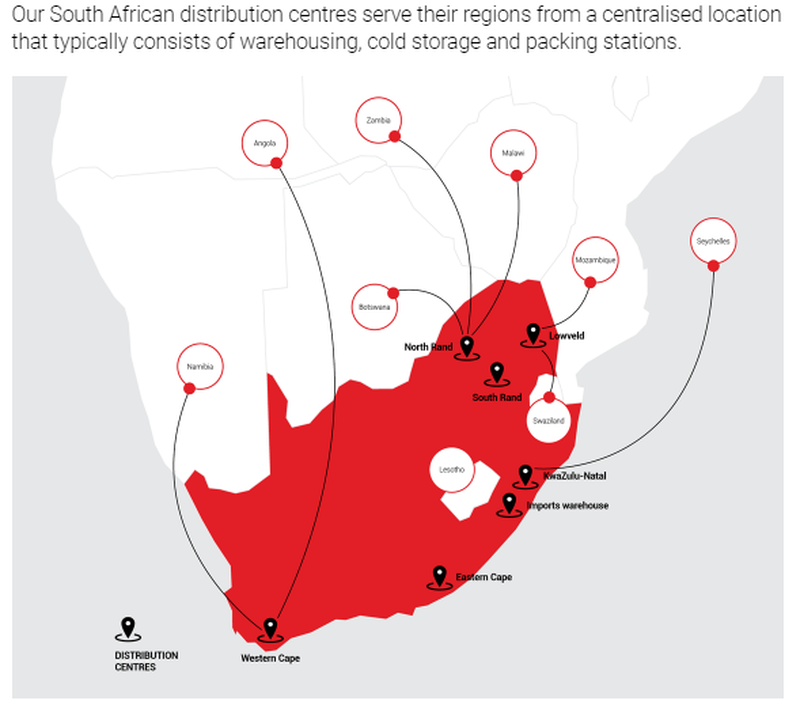

In the 1960’s with the emergence of grocery chains in South Africa, a group made up of 8 wholesalers were given exclusive rights to the SPAR name and brand in 1963, and serviced 500 small retailers. Over time and through many mergers and takeovers, today the SPAR Group Ltd operates 6 distribution centres and 1 Build it distribution centre, supplying goods and services to over 1 000 SPAR stores across Southern Africa.

SPAR is a warehousing and distribution business headquartered in Durban, South Africa. We have been operating in Southern Africa for over five decades. Since 2011, we have expanded into Ireland (including South West England) and Switzerland. We form part of SPAR International, which is present in 44 countries and has 240 distribution centres that serve 13 million customers every day. The SPAR Group Ltd, headquartered in Durban, South Africa, is present in nine countries, has 10 distribution centres and serves 3 768 retail members through 14 store formats every day.

The group currently owns and operates under the following brand names:

SPAR is a warehousing and distribution business headquartered in Durban, South Africa. We have been operating in Southern Africa for over five decades. Since 2011, we have expanded into Ireland (including South West England) and Switzerland. We form part of SPAR International, which is present in 44 countries and has 240 distribution centres that serve 13 million customers every day. The SPAR Group Ltd, headquartered in Durban, South Africa, is present in nine countries, has 10 distribution centres and serves 3 768 retail members through 14 store formats every day.

The group currently owns and operates under the following brand names:

- SPAR

- TOPS at SPAR (Their liquor store offering)

- Build It (Their build supplies and home renovation offering)

- S Buys (a pharmaceutical wholesale business)

- Pharmacy at SPAR (SPAR looking to take advantage of the lucrative personal care and pharmaceutical market in the same way Clicks and Dis-chem has)

SPAR Group distribution centres

Internationally, SPAR is the biggest independent supermarket retail network in the world with 13 000 stores. As part of a global brand, our retailers are able to leverage off international retail design and trends that have kept the SPAR brand at the forefront of food retailing in Southern Africa. SPAR has the most stores in urban residential areas in South Africa. BWG Group is the largest retailer in the Irish convenience retail market by market share. SPAR Switzerland has a state-of-the-art distribution centre and efficient distribution logistics. Pharmacy at SPAR is a SPAR store format and service that is unique to South Africa, with the potential to be rolled out into Ireland and South West England. 32.4% of our turnover is generated in foreign currency.

So to the numbers we go

- Turnover: R101 billion (up 5.9% from R95.4 billion in the prior year)

- Cost of sales: R90.3 billion (up 5.9% from R85.2 billion in the prior year)

- Profit attributable to shareholders: R1.827 billion (up 0.4% from R1.821 billion in the prior year)

- Diluted earnings per share: R9.42 (up 0.3% from R9.39 a share in the prior year).

- Total dividends declared for the financial year: R7.29 a share

- Dividend declared for lat 6 months of the financial year: R4.59 a share

- PE ratio 18.7

- Dividend yield: 4.2%

- Net profit margin: 1.81%

- Cash generated from operations: R3.97 billion (or R20.68 a share)

- Cash and equivalents: R1.37 billion (or R7.13 a share)

So any comments from management on the results?

The following extracts were taken from their financial results as published earlier today.

The SPAR Group (the group) reported a pleasing performance for the year under review, with turnover increasing by 5.9% to R101.0 billion, despite continued challenging trading conditions. The result has again been positively impacted by improving contributions from the European businesses and the group increased operating profit by 7.9% to R2.8 billion. Profit before taxation of R2.5 billion was adversely impacted by fair value adjustments to, and foreign exchange losses on financial liabilities, together with increased interest expenditure resulting from cash outflows for acquisitions.

- SPAR Southern Africa contributed growth in wholesale turnover of 6.7%. This includes turnover reported by the pharmaceutical business, S Buys, acquired during the year. Excluding S Buys, SPAR Southern Africa produced wholesale turnover growth of 5.3% and stable gross margins, in a tough market environment. The TOPS liquor brand delivered an impressive result with wholesale sales growth of 13.0%. Despite a generally weak building materials sector, Build It increased sales by 7.5% enabled by strategic marketing efforts and grew market share. The SPAR Southern Africa store network increased to 2 236 stores, with 145 new stores opened across all brands. The group completed 276 store upgrades across all brands, compared to 259 upgrades in the prior year.

- The BWG Group (SPAR Ireland) has continued to deliver strong euro-denominated results. The BWG Foodservice business reported impressive double-digit turnover growth, while all of the retail brands enjoyed positive sales growth. The Kilcarbery distribution centre saw warehouse turnover increase by 6.9% as more product was directed through the facility. During May 2018, BWG completed the acquisition of 4 Aces Wholesale Limited which operates three cash-and-carry businesses in central Ireland. This business has been successfully integrated into the BWG Group's wholesale operations. SPAR Ireland's store network increased by a net 41 stores to finish the year at 1 371 stores.

- SPAR Switzerland has made significant progress in addressing the overall business performance, despite the difficult Swiss retail environment. While the reported turnover growth has remained negative, this was largely due to the strategic closure and sale of corporate retail stores during the year. However, this had a marked positive impact on the profitability of the overall business. The core wholesale business continued to record improvements in profitability. SPAR Switzerland's store network grew by the addition of 46 new stores to a total of 315 stores.

The SPAR Group (the group) reported a pleasing performance for the year under review, with turnover increasing by 5.9% to R101.0 billion, despite continued challenging trading conditions. The result has again been positively impacted by improving contributions from the European businesses and the group increased operating profit by 7.9% to R2.8 billion. Profit before taxation of R2.5 billion was adversely impacted by fair value adjustments to, and foreign exchange losses on financial liabilities, together with increased interest expenditure resulting from cash outflows for acquisitions.

- SPAR Southern Africa contributed growth in wholesale turnover of 6.7%. This includes turnover reported by the pharmaceutical business, S Buys, acquired during the year. Excluding S Buys, SPAR Southern Africa produced wholesale turnover growth of 5.3% and stable gross margins, in a tough market environment. The TOPS liquor brand delivered an impressive result with wholesale sales growth of 13.0%. Despite a generally weak building materials sector, Build It increased sales by 7.5% enabled by strategic marketing efforts and grew market share. The SPAR Southern Africa store network increased to 2 236 stores, with 145 new stores opened across all brands. The group completed 276 store upgrades across all brands, compared to 259 upgrades in the prior year.

- The BWG Group (SPAR Ireland) has continued to deliver strong euro-denominated results. The BWG Foodservice business reported impressive double-digit turnover growth, while all of the retail brands enjoyed positive sales growth. The Kilcarbery distribution centre saw warehouse turnover increase by 6.9% as more product was directed through the facility. During May 2018, BWG completed the acquisition of 4 Aces Wholesale Limited which operates three cash-and-carry businesses in central Ireland. This business has been successfully integrated into the BWG Group's wholesale operations. SPAR Ireland's store network increased by a net 41 stores to finish the year at 1 371 stores.

- SPAR Switzerland has made significant progress in addressing the overall business performance, despite the difficult Swiss retail environment. While the reported turnover growth has remained negative, this was largely due to the strategic closure and sale of corporate retail stores during the year. However, this had a marked positive impact on the profitability of the overall business. The core wholesale business continued to record improvements in profitability. SPAR Switzerland's store network grew by the addition of 46 new stores to a total of 315 stores.

PROSPECTS

Against the backdrop of subdued consumer and business confidence in Southern Africa, the trading environment is expected to remain largely unchanged in the medium term. While food price inflation has recently dropped to extremely low levels, there are discernible signs that the cycle will start to turn. Recent record movements in fuel prices and continued foreign currency weakness also indicate that consumers will remain under pressure, with a constrained spending outlook. In response, SPAR's extensive distribution capability and market-leading brands are well positioned to deliver exceptional value to consumers and to also ensure that its independent retailers remain suitably positioned to meet these economic challenges.

The Irish business outlook, still influenced by Brexit uncertainties, remains positively cautious in both territories where they operate. Management's proactive response to market changes should ensure that SPAR Ireland will deliver a result in line with expectations. The acquisition of the Corrib Food Products wholesale business subsequent to the reporting date will further strengthen the Irish group's growth objectives.

The Swiss business will maintain its focus on driving the identified strategic initiatives to improve the turnover performance. The group continues to recognise that these objectives will take time to realise, but positive changes are being recorded.The group remains well positioned to continue to create value for shareholders through its growing, diversified business and well-established retail brands.

Against the backdrop of subdued consumer and business confidence in Southern Africa, the trading environment is expected to remain largely unchanged in the medium term. While food price inflation has recently dropped to extremely low levels, there are discernible signs that the cycle will start to turn. Recent record movements in fuel prices and continued foreign currency weakness also indicate that consumers will remain under pressure, with a constrained spending outlook. In response, SPAR's extensive distribution capability and market-leading brands are well positioned to deliver exceptional value to consumers and to also ensure that its independent retailers remain suitably positioned to meet these economic challenges.

The Irish business outlook, still influenced by Brexit uncertainties, remains positively cautious in both territories where they operate. Management's proactive response to market changes should ensure that SPAR Ireland will deliver a result in line with expectations. The acquisition of the Corrib Food Products wholesale business subsequent to the reporting date will further strengthen the Irish group's growth objectives.

The Swiss business will maintain its focus on driving the identified strategic initiatives to improve the turnover performance. The group continues to recognise that these objectives will take time to realise, but positive changes are being recorded.The group remains well positioned to continue to create value for shareholders through its growing, diversified business and well-established retail brands.

So should you buy their shares?

Well thats the million dollar question everyone wants to know the answer to. Their margins are paper thin, similar to that of their peers in the industry such as Shoprite. They are looking to expand into the higher margin products such as the personal care and pharmaceutical space with their Pharmacy at SPAR offering. However they are going head on with two giants in the South African market in that product space, namely Dis-Chem and Clicks. Both of which have a significant footprint and market share in this space already.

For South African investors who like to hedge their investments against the volatile Rand, SPAR offers a bit of Rand hedge opportunity with the group earning about one third of their revenues in other currencies. They have a decent dividend yield of over 4%, their PE ratio is on the high side, but they do offer essential goods and services consumers cannot live without so there will always be a demand for the goods they sell, and this type of high demand goods suppliers tend to trade at relatively high PE ratios as investors know demand for their goods will always be there, regardless of what the economic environment looks like.

For South African investors who like to hedge their investments against the volatile Rand, SPAR offers a bit of Rand hedge opportunity with the group earning about one third of their revenues in other currencies. They have a decent dividend yield of over 4%, their PE ratio is on the high side, but they do offer essential goods and services consumers cannot live without so there will always be a demand for the goods they sell, and this type of high demand goods suppliers tend to trade at relatively high PE ratios as investors know demand for their goods will always be there, regardless of what the economic environment looks like.

SPAR Group (SPP) share valuation

Based on their financial results, their cash generation and current cash position as well as their PE ratio and dividend yield, and their small Rand hedge characteristic our valuation model values the group at R180.50 a share. Thus at its current price it is very close to fully valued. We would therefore advise potential buyers of the share to look to buy into the company at levels below R180 a share, preferably closer to the R160 a share, as this provides some meat on the bone for investors looking to minimise potential downside to their investments