|

Related Topics |

|

We take a look at struggling food group, Famous Brands latest trading update. The share used to be the darling of the market but after buying Gourmet Burger Kitchen the UK and the struggling SA economy the group and its stock price has been struggling for some time now. So how did their trade go the last 6 months?

|

|

About Famous Brands

Famous Brands owns a large number of franchised restaurants, coffee shops and bars. And they have been fueling their growth over the last number of years by way of acquisition. They have been on a tremendous buying spree and they were hoping to replicate their local, South African success in the UK with the acquisition of GBK. However they are finding that it is a lot harder to do this than what they initially thought. They bought GBK for almost R2 billion and since then the group has written off substantial amounts of that investment.

Well they own the following brands (note we only listing a few of their brands below).

Well they own the following brands (note we only listing a few of their brands below).

- Mugg & Bean

- Wimpy

- Fishaways

- Debonairs

- Steers

- Vovo Telo

- Tashas

- Keg

- Mythos

- Turn 'n Tender

- Milky Lane

- Salsa Mexican Grill

- Giramundo

Trading update for the year ending 29 February 2020

The Group’s results for the year ended 29 February 2020 will be published on or about 26 May 2020. In the interim, shareholders are provided with the following brief voluntary performance update on the business. This update pertains to the 52 weeks ended 29 February 2020 for the Group’s South Africa (“SA”) and rest of Africa and Middle East (“AME”) regions. The United Kingdom (“UK”) operation narrative relates to the Gourmet Burger Kitchen Restaurants Limited (“GBK”) business for the 52-week period ended 23 February 2020. Collectively this reporting period is referred to as the “review period”. The challenging trading conditions outlined in the first half of the year persisted for the balance of the review period, featuring subdued consumer sentiment and constrained discretionary spend. In the SA market, margin pressure increased in the context of an intensely competitive trading landscape and sustained low food inflation. Furthermore, frequent power outages and the lack of transformational economic and socio- political reforms weighed heavily on economic growth and business and consumer confidence.

BRANDS

The Group’s restaurants trade in three primary markets, SA, AME and the UK. The brand portfolio is categorised into Leading (mainstream) and Signature (niche) brands.

SA

Trading performance over the review period - which includes the traditional peak SA summer holidays - broadly met management’s expectations, despite the untimely setback caused by load shedding in December. The Group’s Leading brands delivered creditable results for the period. Most of the brands in this portfolio are established market leaders and their value offering (price, quality and service) continued to enjoy strong customer loyalty. On balance, the Signature brands portfolio performed better than in the prior comparable period, attributable to implementation of remedial interventions and further rationalisation of under- performing sites and offerings. Certain brands remain the subject of critical review, with the goal being to ensure the portfolio delivers returns which are proportionally aligned with investment. Across our Leading and Signature brands, combined system-wide sales* increased 6.4%, while like-for-like sales** grew by 2.9%. Independently, Leading brands system-wide sales rose 5.7%, with like-for-like sales up 3.5%. Signature brands^ system-wide sales increased 10.6%, while like-for-like sales declined by 0.8%. Notably, while low menu pricing assisted with customer retention, it had an adverse impact on inflationary growth.

AME

Our AME operations recorded system-wide sales growth of 4.1% in Rand terms, a pleasing return on investments made over recent years.

UK: GBK

Uncertainty regarding the resolution of Brexit persisted during most of the reporting period, subduing consumer confidence and spend in the UK market. GBK’s results for the review period reflect the difficult and intensely competitive trading conditions, however, management is satisfied that ongoing and extensive operational improvements as well as the benefits derived from the Company Voluntary Arrangement (“CVA”) restructuring programme continue to impact positively on the business. System-wide sales (Sterling) declined by 13.9% (attributable to the closure of restaurants as part of the CVA process), while like-for-like sales increased by 3.7% compared to the previous year.

SUPPLY CHAIN: MANUFACTURING AND LOGISTICS

Softer pricing at the front-end of the business impacted on this division’s revenue growth, as stubbornly low food inflation inhibited opportunities to increase prices; this, together with the deliberate strategy to entrench the competitiveness of the supply chain, served to erode profits. The financial information on which this voluntary performance update is based has not been reviewed or reported on by the Group’s external auditors.

BRANDS

The Group’s restaurants trade in three primary markets, SA, AME and the UK. The brand portfolio is categorised into Leading (mainstream) and Signature (niche) brands.

SA

Trading performance over the review period - which includes the traditional peak SA summer holidays - broadly met management’s expectations, despite the untimely setback caused by load shedding in December. The Group’s Leading brands delivered creditable results for the period. Most of the brands in this portfolio are established market leaders and their value offering (price, quality and service) continued to enjoy strong customer loyalty. On balance, the Signature brands portfolio performed better than in the prior comparable period, attributable to implementation of remedial interventions and further rationalisation of under- performing sites and offerings. Certain brands remain the subject of critical review, with the goal being to ensure the portfolio delivers returns which are proportionally aligned with investment. Across our Leading and Signature brands, combined system-wide sales* increased 6.4%, while like-for-like sales** grew by 2.9%. Independently, Leading brands system-wide sales rose 5.7%, with like-for-like sales up 3.5%. Signature brands^ system-wide sales increased 10.6%, while like-for-like sales declined by 0.8%. Notably, while low menu pricing assisted with customer retention, it had an adverse impact on inflationary growth.

AME

Our AME operations recorded system-wide sales growth of 4.1% in Rand terms, a pleasing return on investments made over recent years.

UK: GBK

Uncertainty regarding the resolution of Brexit persisted during most of the reporting period, subduing consumer confidence and spend in the UK market. GBK’s results for the review period reflect the difficult and intensely competitive trading conditions, however, management is satisfied that ongoing and extensive operational improvements as well as the benefits derived from the Company Voluntary Arrangement (“CVA”) restructuring programme continue to impact positively on the business. System-wide sales (Sterling) declined by 13.9% (attributable to the closure of restaurants as part of the CVA process), while like-for-like sales increased by 3.7% compared to the previous year.

SUPPLY CHAIN: MANUFACTURING AND LOGISTICS

Softer pricing at the front-end of the business impacted on this division’s revenue growth, as stubbornly low food inflation inhibited opportunities to increase prices; this, together with the deliberate strategy to entrench the competitiveness of the supply chain, served to erode profits. The financial information on which this voluntary performance update is based has not been reviewed or reported on by the Group’s external auditors.

Fish Aways, one of Famous Brand's fast food and take out brands

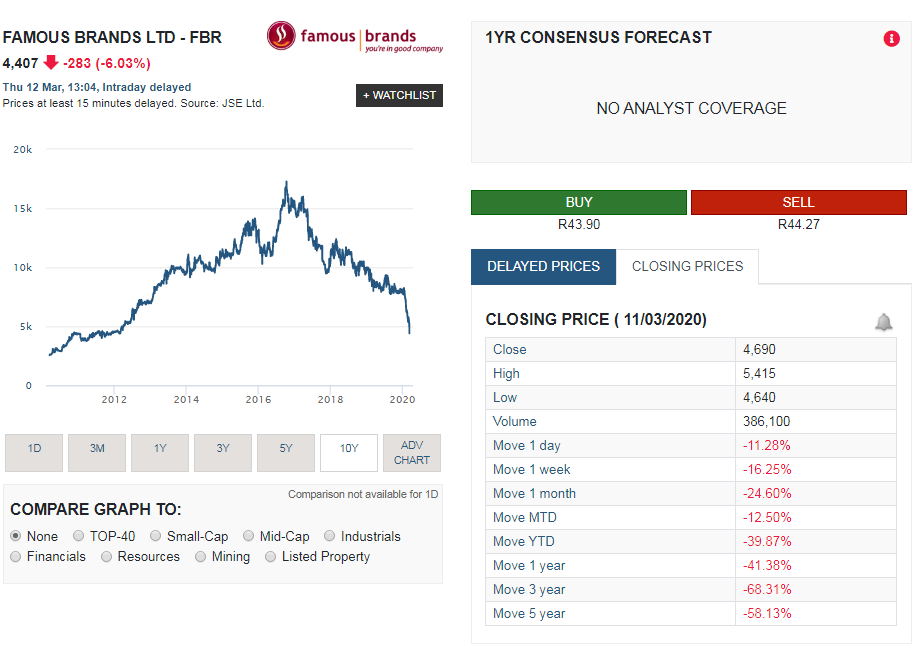

So how has FBR's share price been doing?

The graphic below shows how FBR's share price has been performing in recent years, and as readers can see FBR current share price is a long way off from the highs reached just a few years ago, showing just how tough the going has been for the group. The screenshot was taken from Sharenet

The summary below shows the share price performance of Famous Brands (FBR) over various time periods:

- 1 week: -16.25%

- 1 month: -24.60%

- Year to date: -39.87%

- 1 year: -41.38%

- 3 years: -68.31%

- 5 years: -58.13%

So should you buy FBR shares?

At this point in time, we would not recommend buying into the fast food/ casual dining market. South African consumers are struggling, the Food and Beverages sector has been spinning its wheels in South Africa for a while now, and FBR with their issues in the UK will be focused on trying to get that fixed, which according to us will leave management with less time to focus on South Africa and expanding their business and footprint here, in a market that is already struggling. They not the biggest dividend payer, they trading on a very high PE ratio, but on the positive side they have extremely strong cash generation. But overall we recommend staying away from FBR at this point in time.

But if you really want a benchmark or target price for Famous Brands (FBR), taking all their financials, their brands, their markets and their current issues and obstacles into account, our valuation model places a value of R62.40 per share on FBR (up slightly from our last full year financial results valuation of Famous Brands). But with the markets in free fall due to Coronavirus fears and its potential impact on global economic growth we would not recommend that investors buy into stocks at this point in time, even if stocks are overvalued. Rather wait for more clarity on the Coronavirus and its impact before looking to enter undervalued stocks.

But if you really want a benchmark or target price for Famous Brands (FBR), taking all their financials, their brands, their markets and their current issues and obstacles into account, our valuation model places a value of R62.40 per share on FBR (up slightly from our last full year financial results valuation of Famous Brands). But with the markets in free fall due to Coronavirus fears and its potential impact on global economic growth we would not recommend that investors buy into stocks at this point in time, even if stocks are overvalued. Rather wait for more clarity on the Coronavirus and its impact before looking to enter undervalued stocks.