|

Related Topics |

|

We take a look at the interim results of the makers of Amarula, Savanna, Klipdrift Brandy, Richelieu Brandy, J-C le Roux sparkling wine as well as Two oceans, and whiskies such as Scottish Leader and Three Ships whiskey. So has the tough economic conditions in South Africa had an impact on their sales volumes or profit margins? We take a look below.

|

|

About Distell (DGH)

Distell is the only South African-owned and operated alcoholic beverages company and Africa's leading producer and marketer of wines, spirits, ciders and RTD's, sold across the world. We are becoming a geographically diverse group that is building long-term platforms to unlock growth in various geographies. Markets outside of South Africa are contributing almost a quarter of revenue.

Wines:

Distell's wines, with their rich heritage, have built significant mainstream and premium opportunities and are sold on every continent.

Spirits:

Amarula is ranked as the world's second-largest cream liqueur and Distell is South Africa's leading producer of brandy. Klipdrift is one of South Africa’s best-loved, well-crafted brandy spirits. For more than 77 years, Klipdrift has been made by stripping away the head and tail of the finest brandy to keep the part that really matters; a golden liquid so smooth and refined, we call it the Heart of Gold. The best friendships are made the same way. Whether old or new, celebrate the friends that really matter to you with a truly South African icon in hand; neat, on ice or with your favourite mixer.

Ciders and ready to drink (RTD's):

We pioneered the cider category in South Africa to become the second-largest producer of ciders worldwide. Ever since its inception, Savanna has been a brave and confident brand. Since it’s launch in 1996, we have won over the hearts and funny bones of South Africans with our dry humour, distinctly shaped bottle and well known previous pay-off line “It’s Dry. But you can drink it”. Savanna is one of the world’s largest selling ciders and South Africa’s leading cider export, available in more than 60 countries. Take your pick from our delicious variants, including Savanna Dry and Light.

We are building an empowered, high-performance organisational culture that encourages innovation from a diverse pool of talented professionals.

Wines:

Distell's wines, with their rich heritage, have built significant mainstream and premium opportunities and are sold on every continent.

Spirits:

Amarula is ranked as the world's second-largest cream liqueur and Distell is South Africa's leading producer of brandy. Klipdrift is one of South Africa’s best-loved, well-crafted brandy spirits. For more than 77 years, Klipdrift has been made by stripping away the head and tail of the finest brandy to keep the part that really matters; a golden liquid so smooth and refined, we call it the Heart of Gold. The best friendships are made the same way. Whether old or new, celebrate the friends that really matter to you with a truly South African icon in hand; neat, on ice or with your favourite mixer.

Ciders and ready to drink (RTD's):

We pioneered the cider category in South Africa to become the second-largest producer of ciders worldwide. Ever since its inception, Savanna has been a brave and confident brand. Since it’s launch in 1996, we have won over the hearts and funny bones of South Africans with our dry humour, distinctly shaped bottle and well known previous pay-off line “It’s Dry. But you can drink it”. Savanna is one of the world’s largest selling ciders and South Africa’s leading cider export, available in more than 60 countries. Take your pick from our delicious variants, including Savanna Dry and Light.

We are building an empowered, high-performance organisational culture that encourages innovation from a diverse pool of talented professionals.

- Distell maintained B-BBEE level 4 status (up from level 8 in 2016).

- We strive to further socio-economic development and make meaningful contributions to the communities we operate in.

- In 2018 the Distell Development Trust disbursed R7,5 million to 12 programmes.

The image above shows a few of Distell's best known brands

So lets take a look at the group's financial results

- Hunters Dry

- Nederberg Wine

- Savanna

- Drosty-Hof

- Durbanville Hills

- Klipdrift

- Richelieu

- Old Brown Sherry

So lets take a look at the group's financial results

Financial overview

Key information regarding Distell's latest financial results according to the group

Now for the numbers we are interested in:

- Comparable Group revenue up 9,1% on flat volumes

- Solid domestic revenue growth in all three categories in tough trading conditions

- Revenue (net of excise) growth in 12 out of the top 15 largest brands

- Exceptional African performance led by Kenya, Mozambique and Zambia

- International growth benefiting from focus

- EBITDA Reported up 5,7%

- EBITDA Normalised and adjusted for forex up 6,1%

- Headline earnings Reported up 12,1%

- Headline earnings Normalised and adjusted for forex up 6,6%

- Interim dividend up 5,5%

- Net cash generated from operating activities up 35,8%

Now for the numbers we are interested in:

- Revenue: R14.42 billion (up 7.3% from R13.43 billion in the prior)

- Cost of goods sold: R12.52 billion (up 7.2% from R11.68 billion in the prior year)

- Profit for the period: R1.27 billion (up 5.2% from R1.21 billion in the prior year)

- Net profit margin: 8.83%

- Diluted Headline Earnings per share: R5.70 (up 11.9% from R5.10 in the prior year)

- PE ratio: 11.25

- Dividend declared for interim period: R1.74 per share (up 5.4% from R1.65 in the prior year)

- Dividend yield: 2.7%

- Cash generated from operations: R2.899 billion (up 33.3% from R2.17 billion in the prior year)

- Cash generated from operations per share: R13.20 per share

- Net asset value per share: R56.67 (up 9.7% from R51.63 in the prior year)

- So trading at about 2.25 its stated net asset value

- Cash on balance sheet: R2.1 billion (up 215% from R977 million in the prior year)

- Cash on balance sheet per share: R9.61 or 7.5% of the current share price

Management commentary on the results

Comparable Group revenue grew by 9,1% to R14,4 billion on constant volumes. Revenue excluding excise duty grew by 9,3%. Reported revenue grew by 7,3%.

DOMESTIC MARKET

Comparable domestic market revenue increased by 7,8% with sales volumes down by 2,1% as declining disposable income impacted on peak-season sales and consumer confidence. As previously guided, the Group took proactive pricing decisions in the period which had a positive effect on revenue. The cider and ready-to-drink (RTD) portfolio continued to deliver overall revenue growth on marginally lower volumes, with Savanna, Extreme and Bernini achieving excellent volume and revenue growth. The spirits category showed strong revenue growth led by exceptional gin and vodka growth. The whisky category showed resilience with excellent volume and revenue growth with our blended whisky portfolio bucking international trends and capturing down-trading consumption. Bain's continues to outperform with double-digit volume and revenue growth. Brandy volumes declined as consumers traded down to value offerings and to beer where price competition has been intense across channels and occasions. The wine portfolio recorded muted revenue growth. The mainstream wine portfolio experienced single-digit revenue growth with standout performances from Drostdy-Hof and Paarl Perle showing double-digit revenue growth in each brand in spite of higher pricing caused by higher cost inflation associated with the recent drought. The premium wine portfolio recorded low revenue growth as aggressive pricing decisions were implemented across the brand portfolio. However, commendable growth was seen in established brands like Durbanville Hills, Nederburg and Pongracz.

AFRICA EXCLUDING SOUTH AFRICA

African markets, outside South Africa, delivered exceptional comparable revenue growth of 21,1% on sales volumes which were up by 12,7%. Focus markets on the continent, outside the Southern African Customs Union (SACU), delivered excellent results with revenue and volume growth of 43,0% and 34,1% respectively, giving impetus to our African growth objectives. Nigeria, Kenya, Zambia and Mozambique all recorded strong growth across all three categories as we continue to build our local production and route-to-market (RTM) across the markets. All categories delivered overall double-digit volume and revenue growth. The RTD category growth came from Hunter's and Savanna while spirits category growth was led by Kibao and Hunter's Choice in Kenya. Strong growth in wines was experienced across the portfolio with J.C. Le Roux and Nederburg the standout premium brands delivering double-digit growth. Mainstream brands delivered overall double-digit volume and revenue growth with 4th Street delivering triple-digit performance by volume and value. Trading conditions in Angola and Zimbabwe remained challenging with currency devaluations and liquidity restrictions impacting on operating performance. We are confident in managing these risks by continuing to expand our local production and RTM platforms whilst being less dependent on our historic export business. BLNS countries in SACU delivered low overall revenue growth. The Africa region contributed 62,4% to foreign revenue and pleasingly its contribution to Group revenue rose to 15,6% in the period.

INTERNATIONAL MARKETS

Volumes in international markets outside Africa declined by 6,5%, predominantly affected by trading conditions in Europe and North America where we have curtailed the sales of lower margin wines. Comparable revenue increased by 3,7% as momentum built on a narrower and more profitable portfolio. Volume and revenue growth in our spirits portfolio was led by excellent Scottish Leader growth in Taiwan and strong sales of single malts in all major markets. Wine volumes and revenue in the UK delivered excellent growth. Comparable operating costs rose by 9,4%, of which sales and marketing costs rose by 9,8%. Our underlying operating costs were well controlled and grew at 8,4%. However, Group retrenchment, restructuring and other one-off costs of R68,0 million are included in operating costs. The Group invested USD21,7 million in savings bonds of the Reserve Bank of Zimbabwe following severe currency restrictions that limited the ability of customers to repatriate funds to South Africa. Included in operating costs are expected credit losses of R42,1 million related to this investment. More detail is provided in note 12(b) to the condensed consolidated interim financial statements.

The Group has recently announced further initiatives to optimise and improve the efficiencies of our supply chain. It is also reviewing central support functions throughout the Group to align to new ways of working which support a change in culture, operating model efficiencies and decision making.

PROSPECTS

Global expansion has weakened and growth forecasts for 2019 and 2020 have been revised downward. An escalation of trade tensions remain a key source of risk and financial conditions have tightened internationally as debt levels remain high. On the contrary, growth in sub-Saharan Africa is expected to improve over the same period with caution towards Angola and Nigeria due to softer oil prices alongside changes in government.

This year continues to be another challenging period for the South African economy as per capita GDP continues to decline together with high rates of unemployment. Less favourable weather conditions in certain maize-production areas may also negatively impact on the country's growth outlook. However, inflation forecasts indicate that subdued levels will continue and the overall economic growth momentum is expected to pick up from the second half of the calendar year. The Group has secured sufficient grape and wine supply for the forthcoming cycle following early indications that this year's harvest will not produce an increase in volumes compared to the previous year. The Group is maintaining its water management and reduction programme, especially in the Western Cape, as it extends the programme nationally.

We will continue to defend and grow our South African business with a targeted annual 0,5% increase in market share across our portfolios. We will leverage off improved market execution and revitalised and improved marketing investment behind key brands while we continue to restructure our portfolio for optimal returns.

Sub-Saharan Africa growth affirms our strategy to continue the expansion of our local production and RTM platform across selected African countries. We anticipate further growth as we invest behind and leverage off opportunities in mainstream spirits and wine as well as cider and RTDs.

Conditions outside Africa affirm our refined international focus to grow our premium spirits portfolio while restructuring the wine portfolio to extract more scale and profitability.

Distell's diversified portfolio of well-known brands, which trades across taste profiles, mixed-gender occasions and repertoires, underscores our ability to capture growth opportunities as they arise. This is driven by a purpose-led ambition to become an African drinks champion and benefit communities in which we operate for the better.

DOMESTIC MARKET

Comparable domestic market revenue increased by 7,8% with sales volumes down by 2,1% as declining disposable income impacted on peak-season sales and consumer confidence. As previously guided, the Group took proactive pricing decisions in the period which had a positive effect on revenue. The cider and ready-to-drink (RTD) portfolio continued to deliver overall revenue growth on marginally lower volumes, with Savanna, Extreme and Bernini achieving excellent volume and revenue growth. The spirits category showed strong revenue growth led by exceptional gin and vodka growth. The whisky category showed resilience with excellent volume and revenue growth with our blended whisky portfolio bucking international trends and capturing down-trading consumption. Bain's continues to outperform with double-digit volume and revenue growth. Brandy volumes declined as consumers traded down to value offerings and to beer where price competition has been intense across channels and occasions. The wine portfolio recorded muted revenue growth. The mainstream wine portfolio experienced single-digit revenue growth with standout performances from Drostdy-Hof and Paarl Perle showing double-digit revenue growth in each brand in spite of higher pricing caused by higher cost inflation associated with the recent drought. The premium wine portfolio recorded low revenue growth as aggressive pricing decisions were implemented across the brand portfolio. However, commendable growth was seen in established brands like Durbanville Hills, Nederburg and Pongracz.

AFRICA EXCLUDING SOUTH AFRICA

African markets, outside South Africa, delivered exceptional comparable revenue growth of 21,1% on sales volumes which were up by 12,7%. Focus markets on the continent, outside the Southern African Customs Union (SACU), delivered excellent results with revenue and volume growth of 43,0% and 34,1% respectively, giving impetus to our African growth objectives. Nigeria, Kenya, Zambia and Mozambique all recorded strong growth across all three categories as we continue to build our local production and route-to-market (RTM) across the markets. All categories delivered overall double-digit volume and revenue growth. The RTD category growth came from Hunter's and Savanna while spirits category growth was led by Kibao and Hunter's Choice in Kenya. Strong growth in wines was experienced across the portfolio with J.C. Le Roux and Nederburg the standout premium brands delivering double-digit growth. Mainstream brands delivered overall double-digit volume and revenue growth with 4th Street delivering triple-digit performance by volume and value. Trading conditions in Angola and Zimbabwe remained challenging with currency devaluations and liquidity restrictions impacting on operating performance. We are confident in managing these risks by continuing to expand our local production and RTM platforms whilst being less dependent on our historic export business. BLNS countries in SACU delivered low overall revenue growth. The Africa region contributed 62,4% to foreign revenue and pleasingly its contribution to Group revenue rose to 15,6% in the period.

INTERNATIONAL MARKETS

Volumes in international markets outside Africa declined by 6,5%, predominantly affected by trading conditions in Europe and North America where we have curtailed the sales of lower margin wines. Comparable revenue increased by 3,7% as momentum built on a narrower and more profitable portfolio. Volume and revenue growth in our spirits portfolio was led by excellent Scottish Leader growth in Taiwan and strong sales of single malts in all major markets. Wine volumes and revenue in the UK delivered excellent growth. Comparable operating costs rose by 9,4%, of which sales and marketing costs rose by 9,8%. Our underlying operating costs were well controlled and grew at 8,4%. However, Group retrenchment, restructuring and other one-off costs of R68,0 million are included in operating costs. The Group invested USD21,7 million in savings bonds of the Reserve Bank of Zimbabwe following severe currency restrictions that limited the ability of customers to repatriate funds to South Africa. Included in operating costs are expected credit losses of R42,1 million related to this investment. More detail is provided in note 12(b) to the condensed consolidated interim financial statements.

The Group has recently announced further initiatives to optimise and improve the efficiencies of our supply chain. It is also reviewing central support functions throughout the Group to align to new ways of working which support a change in culture, operating model efficiencies and decision making.

PROSPECTS

Global expansion has weakened and growth forecasts for 2019 and 2020 have been revised downward. An escalation of trade tensions remain a key source of risk and financial conditions have tightened internationally as debt levels remain high. On the contrary, growth in sub-Saharan Africa is expected to improve over the same period with caution towards Angola and Nigeria due to softer oil prices alongside changes in government.

This year continues to be another challenging period for the South African economy as per capita GDP continues to decline together with high rates of unemployment. Less favourable weather conditions in certain maize-production areas may also negatively impact on the country's growth outlook. However, inflation forecasts indicate that subdued levels will continue and the overall economic growth momentum is expected to pick up from the second half of the calendar year. The Group has secured sufficient grape and wine supply for the forthcoming cycle following early indications that this year's harvest will not produce an increase in volumes compared to the previous year. The Group is maintaining its water management and reduction programme, especially in the Western Cape, as it extends the programme nationally.

We will continue to defend and grow our South African business with a targeted annual 0,5% increase in market share across our portfolios. We will leverage off improved market execution and revitalised and improved marketing investment behind key brands while we continue to restructure our portfolio for optimal returns.

Sub-Saharan Africa growth affirms our strategy to continue the expansion of our local production and RTM platform across selected African countries. We anticipate further growth as we invest behind and leverage off opportunities in mainstream spirits and wine as well as cider and RTDs.

Conditions outside Africa affirm our refined international focus to grow our premium spirits portfolio while restructuring the wine portfolio to extract more scale and profitability.

Distell's diversified portfolio of well-known brands, which trades across taste profiles, mixed-gender occasions and repertoires, underscores our ability to capture growth opportunities as they arise. This is driven by a purpose-led ambition to become an African drinks champion and benefit communities in which we operate for the better.

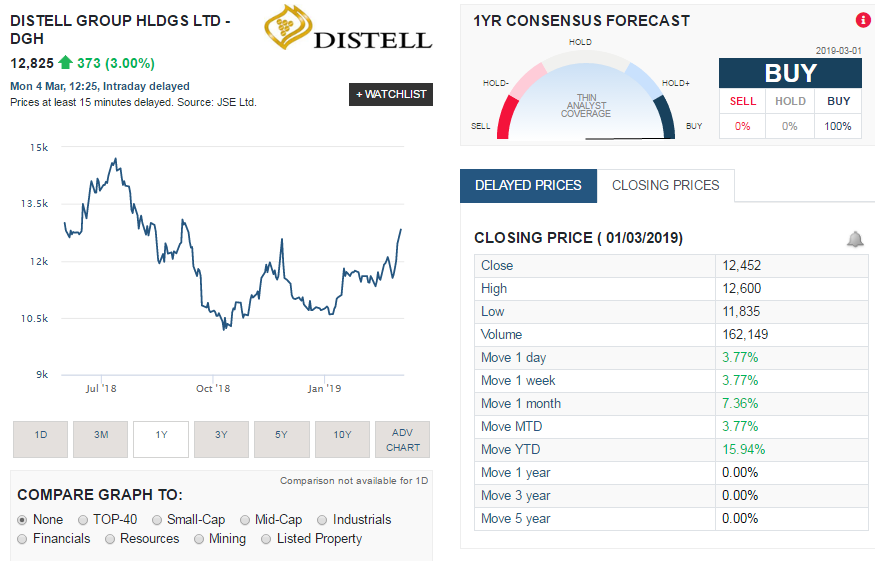

Share price performance

The screenshot below taken from Sharenet shows the share price performance of Distell (DGH) over the last 9 months. Below a summary of the performance of DGH shares over various time periods:

- 1 week: 3.77%

- 1 month: 7.36%

- Year to date (YTD): 15.94%

Shoprite (SHP) share price history

Valuation of Distell (DGH)

So what are Distell (DGH) shares worth? They have strong profit margins, very strong well known brands both locally and abroad. They have a solid balance sheet and strong cash generation. Their volumes in their biggest market, South Africa is declining though and with tough competition from international brands and even tougher economic conditions ahead for South Africa we would not be surprised if we see volumes continuing to decline in South Africa for a while still. But in saying that they have a great foothold in SA with strong customer loyalty towards their brands. All things considered we value Distell (DGH) at R140.80 a share

At R140.80 a share the group will trade a PE ratio of 12.8 and a dividend yield of 2.7%. Which even at our lowest valuation of R140.80 a share is not a demanding PE ratio at all for a relatively defensive stock considering their strong brand portfolio.

At R140.80 a share the group will trade a PE ratio of 12.8 and a dividend yield of 2.7%. Which even at our lowest valuation of R140.80 a share is not a demanding PE ratio at all for a relatively defensive stock considering their strong brand portfolio.