|

Cartrack financial results for the year ending February 2019

Date: 28 May 2019 Category: Stock Market Share price at time of writing: R17.00 |

Related Topics |

|

Latest review of Cartrack's financial results for year ending February 2019. How much are their shares worth? And are they growing subscriber numbers?

|

|

About Cartrack

So what exactly does Cartrack do and in which markets do they operate in? Well the following section will provide more details regarding the group's operations, services and markets they operate it.

Cartrack commenced operations in 2004 and listed on the Johannesburg Stock Exchange as Cartrack Holdings Limited in 2014 Sharecode (CTK). Cartrack has developed into a leading global provider of Fleet Management, Stolen Vehicle Recovery and Insurance telematics services with a strong focus on technology development to enhance customer experience. An extensive footprint is already well established in Africa, Europe and South East Asia; more recently, operations have been opened in America and New Zealand.

Cartrack is a service-centric organisation supported by a strong focus on in-house design, development and installation of Telematics technology and data analytics. Cartrack provides fleet, mobile asset and workforce management solutions underpinned by real-time actionable business intelligence, delivered as Software-as-a-Service (‘SaaS’), plus the service of tracking and recovery of stolen vehicles.

Our technology is widely accepted by motor manufacturers and insurers, with hardware and installations being of the highest standard. Cartrack’s user-friendly and cost-effective web-based Fleet Management portal provides a comprehensive set of features ensuring the optimisation of both fleet and human resources. To expand its integrated service offering, Cartrack is providing driver risk assessment offerings in the field of Insurance Telematics.

Cartrack also specialises in vehicle tracking and recovery, providing an invaluable service to combat vehicle theft in countries where crime is prevalent. Demonstrating its confidence in its systems, Cartrack was the first company globally to offer a cash back recovery warranty of up to R150 000 to its customers in the unlikely event of non-recovery of their stolen vehicles. An industry leading audited recovery rate of 91% in South Africa is evidence of the superior quality of our technology and services.

Our vision is to achieve global industry leadership in the telematics industry including Fleet Management, Stolen Vehicle Recovery and Insurance Telematics services with our mission being to provide our clients and partners with real-time actionable business intelligence based on advanced technology and reliable data.

Cartrack commenced operations in 2004 and listed on the Johannesburg Stock Exchange as Cartrack Holdings Limited in 2014 Sharecode (CTK). Cartrack has developed into a leading global provider of Fleet Management, Stolen Vehicle Recovery and Insurance telematics services with a strong focus on technology development to enhance customer experience. An extensive footprint is already well established in Africa, Europe and South East Asia; more recently, operations have been opened in America and New Zealand.

Cartrack is a service-centric organisation supported by a strong focus on in-house design, development and installation of Telematics technology and data analytics. Cartrack provides fleet, mobile asset and workforce management solutions underpinned by real-time actionable business intelligence, delivered as Software-as-a-Service (‘SaaS’), plus the service of tracking and recovery of stolen vehicles.

Our technology is widely accepted by motor manufacturers and insurers, with hardware and installations being of the highest standard. Cartrack’s user-friendly and cost-effective web-based Fleet Management portal provides a comprehensive set of features ensuring the optimisation of both fleet and human resources. To expand its integrated service offering, Cartrack is providing driver risk assessment offerings in the field of Insurance Telematics.

Cartrack also specialises in vehicle tracking and recovery, providing an invaluable service to combat vehicle theft in countries where crime is prevalent. Demonstrating its confidence in its systems, Cartrack was the first company globally to offer a cash back recovery warranty of up to R150 000 to its customers in the unlikely event of non-recovery of their stolen vehicles. An industry leading audited recovery rate of 91% in South Africa is evidence of the superior quality of our technology and services.

Our vision is to achieve global industry leadership in the telematics industry including Fleet Management, Stolen Vehicle Recovery and Insurance Telematics services with our mission being to provide our clients and partners with real-time actionable business intelligence based on advanced technology and reliable data.

Cartrack service offerings

Cartrack spread far and wide.

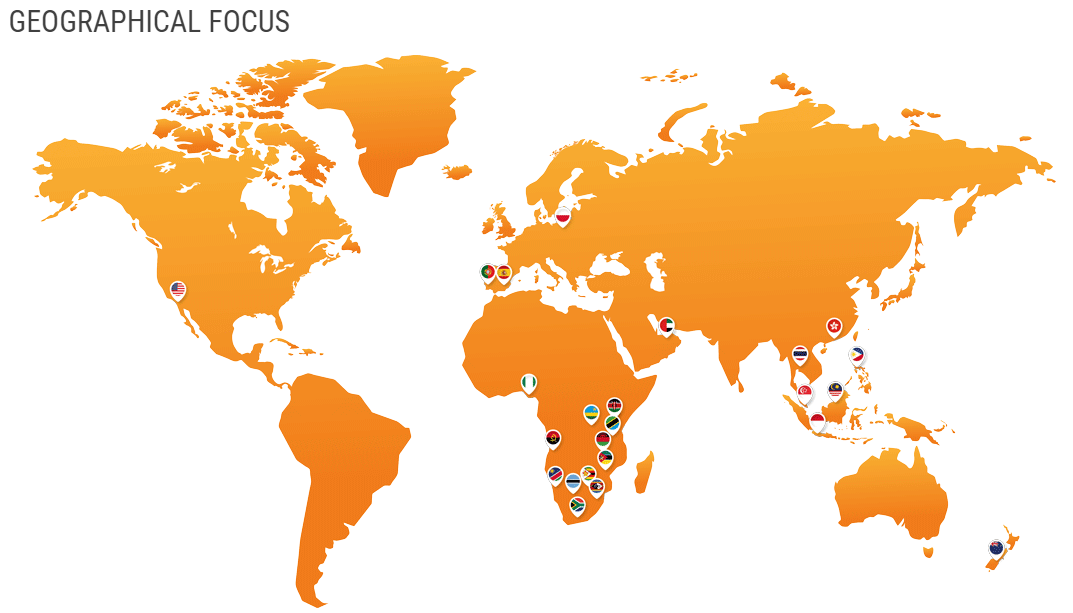

The image below shows in which markets Cartrack are actively operating in. The fact that they are not just in South Africa means the group does provide potential "Rand hedge" benefits, by which a weakening exchange rate could lead to higher reported earnings in Rands from their offshore operations.

Cartrack Geographical representation of their markets

Overview of the results

A short summary on their current group profile

Cartrack, with an active subscriber base of more than 960 78917, ranks amongst of the largest telematics companies globally. The Group's impressive growth since its inception in 2004 has resulted in the development of an extensive footprint in 24 countries across Africa, Europe, North America, Asia Pacific and the Middle East.

Cartrack's success is attributed to its status as a service-centric organisation that focuses on the in-house design, development, production and installation of telematics technology and data analytics products. The Group's technology is widely accepted by motor manufacturers and insurers. Cartrack's customer telematics web interface provides a comprehensive set of features, thereby ensuring the optimisation of its customers' fleet and human resources. As an expansion of its integrated service offering, Cartrack also provides driver risk-assessment offerings in the insurance telematics field.

Cartrack, with an active subscriber base of more than 960 78917, ranks amongst of the largest telematics companies globally. The Group's impressive growth since its inception in 2004 has resulted in the development of an extensive footprint in 24 countries across Africa, Europe, North America, Asia Pacific and the Middle East.

Cartrack's success is attributed to its status as a service-centric organisation that focuses on the in-house design, development, production and installation of telematics technology and data analytics products. The Group's technology is widely accepted by motor manufacturers and insurers. Cartrack's customer telematics web interface provides a comprehensive set of features, thereby ensuring the optimisation of its customers' fleet and human resources. As an expansion of its integrated service offering, Cartrack also provides driver risk-assessment offerings in the insurance telematics field.

So get to the numbers already

So lets take a look at the main numbers published and highlighted in the results:

So now for some of the numbers we are interested in:

PE ratio : 14.65

Dividend yield: 0.71%

Net profit margin: 21.32%

Cash generated per share: R1.81

Cash on balance sheet per share: 17.3c a share

Equity per share/Net asset value per share : R2.79

Tobin's Q: 3.35 (Tobin's Q of 1 implies the group's market capital is the same value as the total value of the group's assets). In the case of CarTrack the market capital of the group is 3.35 times the value of the group's total assets

- Robust subscriber growth of 28% to 960,798

- Net subscriber additions of 209,418 (FY18: 150,770)

- Subscription revenue up 30% to R1,521 million

- Subscription revenue is 90% of the total revenue and growing

- Total revenue up 28% to R1,693 million

- EBITDA of R761 million (FY18: R651 million) with a margin of 45%

- Operating margin of 30%

- Operating profit up 15% to R500 million after accelerated investment for growth

- Basic earnings per share ('EPS') of 116 cents, up 16%

- Headline EPS ('HEPS') of 116 cents, up 15%

- Dividend per share of 12 cents

- Cash generated from operating activities of R544 million (FY18: R468 million)

So now for some of the numbers we are interested in:

PE ratio : 14.65

Dividend yield: 0.71%

Net profit margin: 21.32%

Cash generated per share: R1.81

Cash on balance sheet per share: 17.3c a share

Equity per share/Net asset value per share : R2.79

Tobin's Q: 3.35 (Tobin's Q of 1 implies the group's market capital is the same value as the total value of the group's assets). In the case of CarTrack the market capital of the group is 3.35 times the value of the group's total assets

So what did Cartrack management have to say about the results and their prospects?

Below follows a few extracts from Cartrack's financial results.

Cartrack delivered a strong performance across its key-growth-metrics, with total revenue growing by 28%, from R1,324 million to R1,693 million, and subscription revenue growing by 30% year-on-year, from R1,166 million to R1,521 million. Subscription revenue now represents 90% (FY18: 88%) of total revenue and we expect this to increase further with scale. The number of total subscribers increased by 28%, from 751,380 to 960,798 and the Group continues to maintain a strong pipeline and order book while focusing on fully utilising the distribution footprint it has expanded in the current financial year. The net new subscriber addition of 209,418 is a significant increase from the prior year net additions of 150,770, an achievement worth noting. The decision for ongoing investment in pursuit of sensible growth coupled with the realisation of economies of scale across the businesses and segments will continue to generate robust results in the future and we foresee margin expansion in the short-term. We maintain a focus on ensuring a meaningful return on capital invested for our shareholders. While the Group is gearing for continued sustainable growth, it continues to have an industry-leading EBITDA margin of 45% and an operating profit margin of 30%. On the back of these metrics, management is satisfied with the business performance and delivery of basic EPS of 116 cents compared to 100 cents in the prior year. The high return on equity of 50% and the return on assets of 28% indicate that capital was efficiently applied across the Group and that Cartrack's business model delivers very attractive returns on capital employed for shareholders. It is anticipated that demand for telematics data will continue to increase and lucrative growth opportunities across all distribution channels will increase in all of Cartrack's operating regions.

South Africa

The South African segment delivered particularly strong subscription revenue growth of 31% from R854 million to R1,117 million, while subscribers grew by 30%. The sales mix in FY19 continued to include significantly more bundled sales resulting in a decrease in hardware and installation revenue. The combination of these two delivered strong revenue growth of 27% from R984 million to R1.246 million in a tough trading environment. The increase in distribution expenses is largely a result of focused growth in subscriber acquisition driven through increased marketing expenses and expanded headcount. Investment in sales and marketing has had an immediate positive impact on subscriber growth and we plan to leverage these learnings across our 23 countries globally. This expense line will right size as subscriber growth translates into revenue growth. Similarly, the increase in non-distribution expenses is largely a result of the costs associated with collections. Cartrack has made a substantial investment in its back office to manage the credit risk associated with an economy under pressure. Cartrack will continue to exploit the growth opportunities in South Africa to the extent that operating profit margins can be maintained at target levels. South Africa's operating profit of R422 million, up from R376 million in the prior year, represents a 34% margin. We anticipate margin expansion and continued subscriber growth in FY20 Cartrack will continue to invest in data analytics and behavioural science to ensure insurance partners get relevant and accurate data to manage their own risk and enhance the customer's experience. As the subscriber base and vehicle community continues to grow, Cartrack will continue to identify and exploit opportunities to realise investment return from the economies of scale that this platform brings to it's business. This, in turn, gives Cartrack further opportunity to drive operational efficiency and overall profitable performance.

Asia Pacific

Asia Pacific is the second largest revenue contributor and the fastest growing segment in the Group, with total revenue up by 52% from R118 million to R180 million and subscription revenue up by 51% from R106 million to R160 million. These results are due to an increase of 53% in subscribers. Given the heavy investment in distribution capabilities, the operating profit increased to R16 million up from 15 million in the prior year, representing a 9% margin. Management remains mindful that this segment has the largest potential in the long term and, as such, is devoted to acquiring and coaching the necessary talent to ensure successful long-term growth. The market in this segment remains considerably underpenetrated due to fragmented market participants delivering entry-level telematics offerings, thereby enabling Cartrack to exploit its more sophisticated, reliable products and customer-centric services. Cartrack remains poised to exploit new opportunities while expanding cross-border relationships as it drives it's robust and proven offerings to customers in this segment. Cartrack has also identified the region as having significant strategic benefit to enable the efficient development of world class SaaS products. In line with this, management has taken the necessary steps to establish a R&D centre in Singapore to support the Group's long term vision.

Europe

The European segment delivered subscriber growth of 15%, total revenue growth of 27%, from R116 million to R148 million, and subscription revenue growth of 28% from R111 million to R142 million. The substantial increase in subscription revenue growth is largely attributable to subscriber sales done in the prior financial year. Operating profit of R30 million, up from R19 million in the prior year, represents a 20% margin. The investment in distribution and operating capacity will continue as new channels to market are established. Cartrack is currently evaluating it's strategy to expand into the rest of Europe. Africa (excluding South Africa) The African segment (excluding South Africa) delivered an improved performance despite a weak regional economic backdrop. Africa continues to play a critical role in ensuring a high level of service to customers that increasingly do cross-border travel. The subscriber base in Africa increased by 4% and subscription revenue grew by 5% from R93 million to R98 million , while total revenue increased by 11% from R105 million to R116 million, driven by an increase of new sales in the current year. Operating profit increased to R39 million, up from R32 million in the prior year, representing a 33% margin. Management remains conscious of the importance and potential of this segment and Africa continues to generate positive cash flows.

USA

Cartrack's investment in the US has yielded many key insights that have positively contributed to the Group and this continues to be strategic in nature.

So what is the group's outlook and prospects like? Well the management of the group sounds very positive. Below their outlook

Cartrack delivered a strong performance across its key-growth-metrics, with total revenue growing by 28%, from R1,324 million to R1,693 million, and subscription revenue growing by 30% year-on-year, from R1,166 million to R1,521 million. Subscription revenue now represents 90% (FY18: 88%) of total revenue and we expect this to increase further with scale. The number of total subscribers increased by 28%, from 751,380 to 960,798 and the Group continues to maintain a strong pipeline and order book while focusing on fully utilising the distribution footprint it has expanded in the current financial year. The net new subscriber addition of 209,418 is a significant increase from the prior year net additions of 150,770, an achievement worth noting. The decision for ongoing investment in pursuit of sensible growth coupled with the realisation of economies of scale across the businesses and segments will continue to generate robust results in the future and we foresee margin expansion in the short-term. We maintain a focus on ensuring a meaningful return on capital invested for our shareholders. While the Group is gearing for continued sustainable growth, it continues to have an industry-leading EBITDA margin of 45% and an operating profit margin of 30%. On the back of these metrics, management is satisfied with the business performance and delivery of basic EPS of 116 cents compared to 100 cents in the prior year. The high return on equity of 50% and the return on assets of 28% indicate that capital was efficiently applied across the Group and that Cartrack's business model delivers very attractive returns on capital employed for shareholders. It is anticipated that demand for telematics data will continue to increase and lucrative growth opportunities across all distribution channels will increase in all of Cartrack's operating regions.

South Africa

The South African segment delivered particularly strong subscription revenue growth of 31% from R854 million to R1,117 million, while subscribers grew by 30%. The sales mix in FY19 continued to include significantly more bundled sales resulting in a decrease in hardware and installation revenue. The combination of these two delivered strong revenue growth of 27% from R984 million to R1.246 million in a tough trading environment. The increase in distribution expenses is largely a result of focused growth in subscriber acquisition driven through increased marketing expenses and expanded headcount. Investment in sales and marketing has had an immediate positive impact on subscriber growth and we plan to leverage these learnings across our 23 countries globally. This expense line will right size as subscriber growth translates into revenue growth. Similarly, the increase in non-distribution expenses is largely a result of the costs associated with collections. Cartrack has made a substantial investment in its back office to manage the credit risk associated with an economy under pressure. Cartrack will continue to exploit the growth opportunities in South Africa to the extent that operating profit margins can be maintained at target levels. South Africa's operating profit of R422 million, up from R376 million in the prior year, represents a 34% margin. We anticipate margin expansion and continued subscriber growth in FY20 Cartrack will continue to invest in data analytics and behavioural science to ensure insurance partners get relevant and accurate data to manage their own risk and enhance the customer's experience. As the subscriber base and vehicle community continues to grow, Cartrack will continue to identify and exploit opportunities to realise investment return from the economies of scale that this platform brings to it's business. This, in turn, gives Cartrack further opportunity to drive operational efficiency and overall profitable performance.

Asia Pacific

Asia Pacific is the second largest revenue contributor and the fastest growing segment in the Group, with total revenue up by 52% from R118 million to R180 million and subscription revenue up by 51% from R106 million to R160 million. These results are due to an increase of 53% in subscribers. Given the heavy investment in distribution capabilities, the operating profit increased to R16 million up from 15 million in the prior year, representing a 9% margin. Management remains mindful that this segment has the largest potential in the long term and, as such, is devoted to acquiring and coaching the necessary talent to ensure successful long-term growth. The market in this segment remains considerably underpenetrated due to fragmented market participants delivering entry-level telematics offerings, thereby enabling Cartrack to exploit its more sophisticated, reliable products and customer-centric services. Cartrack remains poised to exploit new opportunities while expanding cross-border relationships as it drives it's robust and proven offerings to customers in this segment. Cartrack has also identified the region as having significant strategic benefit to enable the efficient development of world class SaaS products. In line with this, management has taken the necessary steps to establish a R&D centre in Singapore to support the Group's long term vision.

Europe

The European segment delivered subscriber growth of 15%, total revenue growth of 27%, from R116 million to R148 million, and subscription revenue growth of 28% from R111 million to R142 million. The substantial increase in subscription revenue growth is largely attributable to subscriber sales done in the prior financial year. Operating profit of R30 million, up from R19 million in the prior year, represents a 20% margin. The investment in distribution and operating capacity will continue as new channels to market are established. Cartrack is currently evaluating it's strategy to expand into the rest of Europe. Africa (excluding South Africa) The African segment (excluding South Africa) delivered an improved performance despite a weak regional economic backdrop. Africa continues to play a critical role in ensuring a high level of service to customers that increasingly do cross-border travel. The subscriber base in Africa increased by 4% and subscription revenue grew by 5% from R93 million to R98 million , while total revenue increased by 11% from R105 million to R116 million, driven by an increase of new sales in the current year. Operating profit increased to R39 million, up from R32 million in the prior year, representing a 33% margin. Management remains conscious of the importance and potential of this segment and Africa continues to generate positive cash flows.

USA

Cartrack's investment in the US has yielded many key insights that have positively contributed to the Group and this continues to be strategic in nature.

So what is the group's outlook and prospects like? Well the management of the group sounds very positive. Below their outlook

As we look toward the future, Cartrack remains focused on related telematics and Internet of Things ('IoT') expansion. We continue to drive innovation through our interaction with customers and strategic research activities. We expect double-digit annuity revenue and subscriber growth to continue for the foreseeable future.

Our long term growth is driven by four key factors:

- Connected Vehicles: We are enhancing our platform for connected-vehicles that is brand agnostic as we experiment in smart-mobility, partnering with two of the world's leading companies in pay-as-a-service transportation. This development affirms the strengthening of telematics companies' value proposition and the growing eco-system of services around the motor vehicle. We capitalise on our present and future opportunities as we leverage both Original Equipment Manufacturer (OEM) and third-party telematics devices and data.

- Technology Investment Rises: Favourable industry dynamics are driving our position in the marketplace as our customers are becoming reliant on the telematics market to optimise business intelligence relating to both assets and people on a global scale. As a result of the rapidly changing market, we will continue to invest in technology, information management and human resources, as well as in the distribution and operating capacity in current and new markets

- Increased Demand for Telematics Data: We have seen a notable rise in demand for telematics data across the globe. Our key market, South Africa, remains underpenetrated, with many opportunities available to provide customer-centric solutions to individuals, enterprise customers and fleets alike. We believe that markets across the globe have a strong need for our products

- Exciting New Applications: As part of our drive to add value to our customers, we have added additional specialist applications to our software suite. This includes our easy-to-use administrative and vehicle cost accounting software called MiFleet and a CRM extension to assist our customers in driving profitability and customer retention within their businesses. As an ongoing commitment to our customers' needs, we continue to invest significantly into the enhancement of our existing platforms.

The Africa management team, under a new management structure, with a refreshed distribution and operating capacity, is expected to positively impact the Group results on a sustained basis. The order book in Europe remains strong while new sales are being actively pursued. While subscriber growth and customer service remain the primary focus in Europe, cost rationalisation strategies will be implemented in order to increase operating profit and margin. Asia Pacific continues to gain operational mass as a region, with a strong sales pipeline and many opportunities that are being exploited. As a result of these global strategies, we are confident we will continue to drive strong top line growth and maintain healthy profitability levels.

Our long term growth is driven by four key factors:

- Connected Vehicles: We are enhancing our platform for connected-vehicles that is brand agnostic as we experiment in smart-mobility, partnering with two of the world's leading companies in pay-as-a-service transportation. This development affirms the strengthening of telematics companies' value proposition and the growing eco-system of services around the motor vehicle. We capitalise on our present and future opportunities as we leverage both Original Equipment Manufacturer (OEM) and third-party telematics devices and data.

- Technology Investment Rises: Favourable industry dynamics are driving our position in the marketplace as our customers are becoming reliant on the telematics market to optimise business intelligence relating to both assets and people on a global scale. As a result of the rapidly changing market, we will continue to invest in technology, information management and human resources, as well as in the distribution and operating capacity in current and new markets

- Increased Demand for Telematics Data: We have seen a notable rise in demand for telematics data across the globe. Our key market, South Africa, remains underpenetrated, with many opportunities available to provide customer-centric solutions to individuals, enterprise customers and fleets alike. We believe that markets across the globe have a strong need for our products

- Exciting New Applications: As part of our drive to add value to our customers, we have added additional specialist applications to our software suite. This includes our easy-to-use administrative and vehicle cost accounting software called MiFleet and a CRM extension to assist our customers in driving profitability and customer retention within their businesses. As an ongoing commitment to our customers' needs, we continue to invest significantly into the enhancement of our existing platforms.

The Africa management team, under a new management structure, with a refreshed distribution and operating capacity, is expected to positively impact the Group results on a sustained basis. The order book in Europe remains strong while new sales are being actively pursued. While subscriber growth and customer service remain the primary focus in Europe, cost rationalisation strategies will be implemented in order to increase operating profit and margin. Asia Pacific continues to gain operational mass as a region, with a strong sales pipeline and many opportunities that are being exploited. As a result of these global strategies, we are confident we will continue to drive strong top line growth and maintain healthy profitability levels.

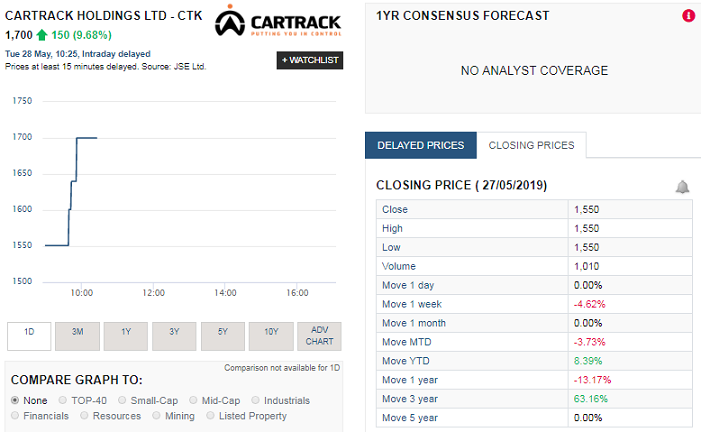

CarTrack share price history and performance

The screenshot below, taken from Sharenet show's Cartrack's share price performance for the day (the market is clearly happy with the results published today) , as well as the returns offered over various periods of time.

The summary below shows the returns provided by Cartrack shares over various periods of time:

So the returns offered by Cartrack has been pretty mixed over the last couple of years.

- 1 week: -4.62%

- 1 month: 0%

- Year to date (YTD): 8.39%

- 1 year: -13.17%

- 3 years: 63.18%

So the returns offered by Cartrack has been pretty mixed over the last couple of years.

So should you buy their shares?

Well crime and hijackings in South Africa will not go away anytime soon. So we suspect the demand for their services will continue to be strong on one of their main markets which is South Africa. Their growth has been pretty rapid, but we are worried that they are financing their growth with debt. And increased debt means increased debt repayments, which for investors will imply less or no dividends being paid, as they would need to pay back debt before being able to splash out on shareholders. And if they pay dividends while having mountains of debt to service, one has to be worried about that to. So investors or potential investors needs to take this into account,.

They are currently trading on a dividend yield of 1.76% after the gross dividend of 12c a share was declared, and PE ratio of close to 15, which is below the market average PE ratio. But it shows the market is expecting significant earnings growth due to their rapid expansion and growth. We would advise investors to sit on the side line at the current price, unless an investor feels the market they operate in is to good to miss out on and believes subscriber numbers will continue to increase at a rapid rate. If not, we believe there are better quality shares out there that investors can invest in. Based on the group's financial results we value the group at R19.48 a share. And we are being pretty generous with this valuation. The main reason for this being the strong cash generation of the group.

They are currently trading on a dividend yield of 1.76% after the gross dividend of 12c a share was declared, and PE ratio of close to 15, which is below the market average PE ratio. But it shows the market is expecting significant earnings growth due to their rapid expansion and growth. We would advise investors to sit on the side line at the current price, unless an investor feels the market they operate in is to good to miss out on and believes subscriber numbers will continue to increase at a rapid rate. If not, we believe there are better quality shares out there that investors can invest in. Based on the group's financial results we value the group at R19.48 a share. And we are being pretty generous with this valuation. The main reason for this being the strong cash generation of the group.