|

Related Topics |

|

We take a look at the latest trading update from Food Producer AVI (AVI). The group's stock was punished hard earlier in the year after the release of their trading statement for the half year. Will the same happen after the release of their full year results?

|

|

About AVI

AVI owns a fw very popular food consumer brands. AVI is the producer of Five roses tea and salticrax. Other well known AVI brands include:

- I&J

- LaCoste

- Baker's

- Provita

- LavAzza

AVI financial results overview

- Revenue: R13.150 billion (down from R13.437 billion for the same period of the previous year)

- Cost of sales: R7.740 billion (up from R7.498 billion for the same period of the previous year)

- Profit attributable to AVI: R1.604 billion (down from R1.675 billion for the same period of the previous year)

- Diluted headline earnings per share: R5.16

- Number of shares in issue: 328.315 million

- Cash generated from operations: R2.849 billion

- Cash generated from operations per share: R8.67

- Cash and equivalents: R233 million

- Cash and equivalents per share: R0.71

- Cash and equivalents makes up 2.3% of AVI's total assets

- Cash and equivalents makes up 0.8% of AVI's market capital

- Shareholders equity: R4.53 billion

- Shareholders equity per share: R13.79

- Inventories and biological assets: R2.501 billion (up from R2.165 billion for the same period of the previous year)

- Inventories grew by 15.51% over the last 12 months

- Inventories makes up 25.5% of AVI's total assets

AVI management commentary on the results

AVI recovered from a difficult first semester with growth in the second half of the year compared to the second half of last year. Although not sufficient to offset the first half decline, it is encouraging to see the resilience of the business in tough times and to commence the next financial year from a sound operating base.

Group revenue for the year was 1,2% higher than last year on a like-for-like basis. The trading environment remained difficult with continued pressure on consumer spending resulting in sales volume weakness in many of our businesses, exacerbated by aggressive competitor discounting in some categories. December’s sales volumes were lower than last year particularly in Spitz, which was unable to repeat record December 2017 sales volumes. Selling prices were maintained throughout the year in most categories and were only increased where there was a need to ameliorate accumulated cost pressures.

Gross profit margins were well protected reflecting generally low raw material cost inflation and good cost control, with the consolidated gross profit margin decreasing slightly from 44,2% to 43,5% on a like-for-like basis. Despite tight management of selling and administrative costs, which increased by 1,7% on a like-for-like basis, like-for-like operating profit was 3,0% lower due to the impact of lower sales volumes in some categories, restructuring costs of R27 million at Green Cross, and an unfavourable movement of R29 million in the mark-to-market adjustment on I&J’s fuel hedges as a result of the low oil price at the end of the period.

The new accounting standards had a negligible impact on headline earnings. Headline earnings declined by 4,4% from R1,77 billion to R1,70 billion due to the decrease in operating profit and higher finance costs in line with higher debt levels. Headline earnings per share decreased 4,9% from 543,1 cents to 516,6 cents with a 0,5% increase in the weighted average number of shares in issue due to the vesting of employee share options, including the AVI Black Staff Empowerment Scheme. Cash generated by operations decreased by 1,8% to R2,64 billion on a like-for-like basis.

Working capital rose R266,8 million due mostly to higher stock levels at year-end while capital expenditure amounted to R472,6 million, reflecting continued investment across the group to sustain and improve our businesses. Other material cash outflows during the period were ordinary dividends of R1,40 billion, a special dividend of R822,9 million and taxation of R604,0 million. Net debt at the end of June 2019 was R2,44 billion compared to R1,27 billion at the end of June 2018, including R408,9 million of lease liabilities recognised in terms of the new lease accounting standard adopted on 1 July 2018.

OUTLOOK

The trading environment is expected to remain difficult, with constrained consumer spending. Our expectation is that many of our categories will continue to have low, or even negative, growth rates until there is a meaningful improvement in the economy.

Notwithstanding this, all of AVI’s businesses are targeting profit growth in the next financial year, underpinned by:

• Strong brands, supported by relevant innovation, that remain appealing to many consumers;

• Foreign currency and key raw materials for the majority of the year’s requirements secured at levels that support sound levels of profitability, including lower rooibos and butter prices than achieved in the 2019 financial year;

• Good price levels secured for key raw materials for the majority of the year’s requirements, including lower rooibos and butter prices than achieved in the 2019 financial year.

Acceptable demand and sales volumes are key to achieving growth and we will continue to react quickly to market changes as we pursue the most appropriate balance of price, sales volumes and profit margins for each of our brands. This will be supported by ongoing focus on factory efficiency, procurement opportunities and review of fixed overheads. Capital projects that underpin our manufacturing capacity, product quality and service levels will continue to be supported. AVI International, supported by our South African manufacturing capabilities, remains focused on steadily building our brands’ shares in export markets whilst sustaining strong profit margins. I&J’s prospects remain materially dependent on fishing performance and exchange rates.

We remain of the view that the performance of the hake resource is set to improve over the next few years, while export exchange rates are largely secured at levels that support sound profitability, and the more recent Rand weakness provides some upside potential. The hake long-term rights application process, to allocate rights from 2021, is not expected to impact operations in the financial year ahead. The Board is confident that AVI remains well positioned to compete effectively; prudently manage fixed and variable costs; and recognising the challenging environment, be alert for appropriate acquisition opportunities both domestically and regionally.

Group revenue for the year was 1,2% higher than last year on a like-for-like basis. The trading environment remained difficult with continued pressure on consumer spending resulting in sales volume weakness in many of our businesses, exacerbated by aggressive competitor discounting in some categories. December’s sales volumes were lower than last year particularly in Spitz, which was unable to repeat record December 2017 sales volumes. Selling prices were maintained throughout the year in most categories and were only increased where there was a need to ameliorate accumulated cost pressures.

Gross profit margins were well protected reflecting generally low raw material cost inflation and good cost control, with the consolidated gross profit margin decreasing slightly from 44,2% to 43,5% on a like-for-like basis. Despite tight management of selling and administrative costs, which increased by 1,7% on a like-for-like basis, like-for-like operating profit was 3,0% lower due to the impact of lower sales volumes in some categories, restructuring costs of R27 million at Green Cross, and an unfavourable movement of R29 million in the mark-to-market adjustment on I&J’s fuel hedges as a result of the low oil price at the end of the period.

The new accounting standards had a negligible impact on headline earnings. Headline earnings declined by 4,4% from R1,77 billion to R1,70 billion due to the decrease in operating profit and higher finance costs in line with higher debt levels. Headline earnings per share decreased 4,9% from 543,1 cents to 516,6 cents with a 0,5% increase in the weighted average number of shares in issue due to the vesting of employee share options, including the AVI Black Staff Empowerment Scheme. Cash generated by operations decreased by 1,8% to R2,64 billion on a like-for-like basis.

Working capital rose R266,8 million due mostly to higher stock levels at year-end while capital expenditure amounted to R472,6 million, reflecting continued investment across the group to sustain and improve our businesses. Other material cash outflows during the period were ordinary dividends of R1,40 billion, a special dividend of R822,9 million and taxation of R604,0 million. Net debt at the end of June 2019 was R2,44 billion compared to R1,27 billion at the end of June 2018, including R408,9 million of lease liabilities recognised in terms of the new lease accounting standard adopted on 1 July 2018.

OUTLOOK

The trading environment is expected to remain difficult, with constrained consumer spending. Our expectation is that many of our categories will continue to have low, or even negative, growth rates until there is a meaningful improvement in the economy.

Notwithstanding this, all of AVI’s businesses are targeting profit growth in the next financial year, underpinned by:

• Strong brands, supported by relevant innovation, that remain appealing to many consumers;

• Foreign currency and key raw materials for the majority of the year’s requirements secured at levels that support sound levels of profitability, including lower rooibos and butter prices than achieved in the 2019 financial year;

• Good price levels secured for key raw materials for the majority of the year’s requirements, including lower rooibos and butter prices than achieved in the 2019 financial year.

Acceptable demand and sales volumes are key to achieving growth and we will continue to react quickly to market changes as we pursue the most appropriate balance of price, sales volumes and profit margins for each of our brands. This will be supported by ongoing focus on factory efficiency, procurement opportunities and review of fixed overheads. Capital projects that underpin our manufacturing capacity, product quality and service levels will continue to be supported. AVI International, supported by our South African manufacturing capabilities, remains focused on steadily building our brands’ shares in export markets whilst sustaining strong profit margins. I&J’s prospects remain materially dependent on fishing performance and exchange rates.

We remain of the view that the performance of the hake resource is set to improve over the next few years, while export exchange rates are largely secured at levels that support sound profitability, and the more recent Rand weakness provides some upside potential. The hake long-term rights application process, to allocate rights from 2021, is not expected to impact operations in the financial year ahead. The Board is confident that AVI remains well positioned to compete effectively; prudently manage fixed and variable costs; and recognising the challenging environment, be alert for appropriate acquisition opportunities both domestically and regionally.

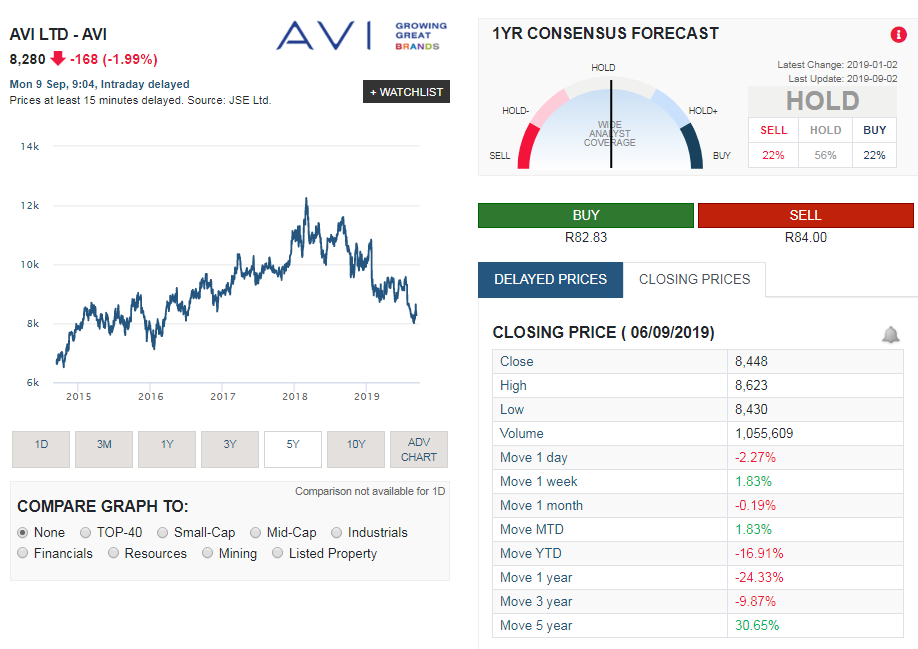

Share price performance of AVI over time

The image below, obtained from Sharenet shows the share price history of AVI over the last 5 years. And its been a pretty volatile ride for AVI shareholders over this time period. The summary below shows the share price movements of AVI over various time periods:

- 1 week: 1.83%

- 1 month: -0.19%

- Year to date (YTD): -16.91

- 1 year: -24.33%

- 3 years: -9.87%

- 5 years: 30.65%

AVI (AVI) share valuation

Based on the latest financial results from AVI, our valuation model gives a full value price for AVI shares at R77.20. We therefore believe that AVI stock is overvalued at its current price and we would not recommend long term fundamental or value investors buy into the share at its current price. But rather buy into it at at least 10% below our target price. So a good entry point into AVI would be below R70 a share