|

Related Topics |

|

We take a look at the latest interim financial results of Mr Price Group for the period ending September 2019. Revenue for the period increased slightly. However profit after taxes were down by just over 10%

|

|

Background and overview of Mr Price Group (MRP)

Mr Price group is a retailer active in the fashion and clothing segment of the market. The retail in apparel, homeware and sportswear and is one of the fastest growing retailers in South Africa. Mr Price's cash sales constitute 82.6% of total sales and the group is focused on remaining a cash-driven retailer. This will continue to differentiate the group from its competitors and produce cash flows that will fund our continued growth and enable an attractive dividend cover.

Their brands include:

Mr Price

Mr Price Sports

Mr Price Home

Sheet Street

Milady's

Mr Price has a very strong foothold in the South African retail clothing market, and this offers a strong value investing proposition for us.

Their brands include:

Mr Price

Mr Price Sports

Mr Price Home

Sheet Street

Milady's

Mr Price has a very strong foothold in the South African retail clothing market, and this offers a strong value investing proposition for us.

Advertisement (and yes South Africans can buy from Amazon as they ship to SA)

Interim financial results commentary as released on 21 November 2019

For the 26 weeks ended 28 September 2019, normalised diluted headline earnings per share (based on the previous IAS 17 basis for accounting for leases) declined 7.2% to 447.5c. After accounting for leases on the new IFRS 16 basis, which did not require a restatement of comparative results, statutory diluted HEPS was 9.6% lower at 435.9c. Normalised basic earnings per share were down 7.9% to 455.4c (statutory -10.3% to 443.6c) and normalised headline earnings per share down 7.9% to 455.0c (statutory -10.3% to 443.2c). The group’s Australian operations have been presented as discontinued operations post trade ceasing on 30 April 2019 and the commentary below refers to the group’s continuing operations.

Shareholders were advised at the presentation of the annual results in May and in the 18-week trading update issued in August, that group results for the first half would be impacted by the under-performance in the Mr Price Apparel division. This is reflected in the results below. Despite this, five of the group’s trading divisions grew sales, gross margins and operating profits, with three increasing operating profits by double digits. The group’s balance sheet is strong, with cash and cash equivalents increasing to R4.2bn, which has enabled the interim dividend to be maintained at 311.4c per share. Total revenue grew 2.6% to R10.8bn. Retail sales grew 1.7% (comparable stores -1.5%) to R9.9bn.

Shareholders were advised at the presentation of the annual results in May and in the 18-week trading update issued in August, that group results for the first half would be impacted by the under-performance in the Mr Price Apparel division. This is reflected in the results below. Despite this, five of the group’s trading divisions grew sales, gross margins and operating profits, with three increasing operating profits by double digits. The group’s balance sheet is strong, with cash and cash equivalents increasing to R4.2bn, which has enabled the interim dividend to be maintained at 311.4c per share. Total revenue grew 2.6% to R10.8bn. Retail sales grew 1.7% (comparable stores -1.5%) to R9.9bn.

Mr Price store interior

Excluding Mr Price Apparel, revenue and retail sales grew 7.3% and 6.1% respectively. Group store sales were up 1.3% and online 28.3%. Retail selling price inflation was 2.2% and 99.4m units were sold, a decline of 0.6%. By opening 27 new stores and expanding 8, weighted average new space grew 3.9%. After closing 12 stores and reducing the size of 16, total weighted average space was up 1.9%, advancing the total number of corporate owned store locations by 4.0% to 1 338. Other income grew 10.2% to R770m due to financial services and cellular growth of 10.3% to R743m. Interest earned on cash balances increased 31.8% to R135m. The group’s GP% contracted 260 bps to 40.0%, but grew by 20 bps excluding Mr Price Apparel. Selling and administration expenses declined 5.0%, impacted by the transition to IFRS 16. Including lease liability interest in expenses, total overheads increased 2.5% on last year. Excluding the impact of the new accounting statement completely, ‘normalised’ overheads only increased by 1.0%.

Profit from operating activities was down 1.6% to R1.7bn and the operating margin was 15.8% of retail sales and other income (RSOI). The Apparel segment increased RSOI by 1.0% to R7.4bn. Operating profit declined by 13.6% with operating margin reducing 240 bps to 14.6%. Miladys delivered strong sales growth of 8.1% (comparable 3.3%) and gained market share in 5 out of 6 months per RLC data. Mr Price Sport delivered an outstanding performance, growing sales by 12.2% (comparable 6.1%), with online sales growing at 34.9%. Miladys and Mr Price Sport both reported double digit growth in operating profit. Sales in Mr Price Apparel declined 1.3% (comparable -4.3%) to R5.8bn. The issues causing the imbalance in the shape of the assortment in the second half of the prior financial period continued into the first half of FY2020, resulting in excess stock which required markdowns to clear. In contrast, online sales grew by 19.7%, highlighting the impact of an imbalanced assortment on the physical store shopping experience.

The new executive team, which was appointed in January and the divisional management team, headed by a new managing director from April, undertook a thorough performance review and identified several significant improvements in operating practices. Due to retail cycle times, action taken is expected to positively impact trading from the high summer period. Research undertaken by the Broadcast Research Council shows that customers are highly engaged, with the chain securing the number one position in ‘clothing stores shopped at most often’. The division also placed first in the Sunday Times/Sowetan Shopper Survey 2019, highlighting brand presence, awareness and customer experience which shows the potential for recovery. Unfortunately, customers were not given the merchandise they desired in a highly competitive market. The Home segment increased RSOI by 4.1% to R2.5bn.

Operating profit grew 17.8% and the operating margin increased. Both divisions reported a solid performance despite household discretionary spend declining, as consumers respond to value in this climate. Sales in Mr Price Home were up 3.2% (comparable 1.8%) with online sales increasing 36.0%. Sheet Street grew sales by 5.0% (comparable 2.5%). The Financial Services & Cellular segment reported revenue growth of 10.3% to R743m and an operating profit growth of 20.7%. Financial services grew revenue 2.2% to R385m (interest and charges +5.9%, insurance -4.8%), while cellular and mobile revenue grew 20.7% to R358m. Cellular products are now sold through a call centre and 242 store kiosks across the group, with further rollout planned.

Retail sales outside of South Africa, which constitute 7.9% of group sales, declined by 2.2%, partly explained by the performance of Mr Price Apparel (which constitutes 69.7% of non-South African sales) and struggling economies. The group has elected to focus on areas of significant potential and accordingly exited Australia. Likewise, the Mr Price Home Polish test store will be closed in December. Efforts will be channelled into improving the performance of the largest apparel division and maximising several local opportunities. Net asset value per share increased 10.3% to 3 273c from September 2018. Capital expenditure of R231m was incurred, primarily in store development activities. Inventory levels were up 14.9%, with markdown units as a percentage of total units lower than the prior period and a good stock freshness ratio. The debtors book remains well managed, with a retail net bad debt to book ratio of 7.2% matched by an impairment provision at the same level. The group has concluded its internal investigation into the suspected non-compliance with its Code of Conduct as advised in the SENS announcements of 12 September and 19 September 2019.

The group’s previously expressed views on materiality have not changed, and appropriate action has been taken in support of its zero-tolerance policy to such matters. A short-term recovery in the consumer environment seems unlikely. Meaningful GDP growth will only return when broad-based structural economic reforms gain traction. The group is focused on winning market share, particularly in Mr Price Apparel. A shift in momentum was seen in the last two months of H1 FY2020, with the group’s retail sales growth outperforming Type D retailers in both August and September 2019. Whilst trade has been challenging, the energy across the business is high and the team is clear on what is needed to return the group to its winning ways

Profit from operating activities was down 1.6% to R1.7bn and the operating margin was 15.8% of retail sales and other income (RSOI). The Apparel segment increased RSOI by 1.0% to R7.4bn. Operating profit declined by 13.6% with operating margin reducing 240 bps to 14.6%. Miladys delivered strong sales growth of 8.1% (comparable 3.3%) and gained market share in 5 out of 6 months per RLC data. Mr Price Sport delivered an outstanding performance, growing sales by 12.2% (comparable 6.1%), with online sales growing at 34.9%. Miladys and Mr Price Sport both reported double digit growth in operating profit. Sales in Mr Price Apparel declined 1.3% (comparable -4.3%) to R5.8bn. The issues causing the imbalance in the shape of the assortment in the second half of the prior financial period continued into the first half of FY2020, resulting in excess stock which required markdowns to clear. In contrast, online sales grew by 19.7%, highlighting the impact of an imbalanced assortment on the physical store shopping experience.

The new executive team, which was appointed in January and the divisional management team, headed by a new managing director from April, undertook a thorough performance review and identified several significant improvements in operating practices. Due to retail cycle times, action taken is expected to positively impact trading from the high summer period. Research undertaken by the Broadcast Research Council shows that customers are highly engaged, with the chain securing the number one position in ‘clothing stores shopped at most often’. The division also placed first in the Sunday Times/Sowetan Shopper Survey 2019, highlighting brand presence, awareness and customer experience which shows the potential for recovery. Unfortunately, customers were not given the merchandise they desired in a highly competitive market. The Home segment increased RSOI by 4.1% to R2.5bn.

Operating profit grew 17.8% and the operating margin increased. Both divisions reported a solid performance despite household discretionary spend declining, as consumers respond to value in this climate. Sales in Mr Price Home were up 3.2% (comparable 1.8%) with online sales increasing 36.0%. Sheet Street grew sales by 5.0% (comparable 2.5%). The Financial Services & Cellular segment reported revenue growth of 10.3% to R743m and an operating profit growth of 20.7%. Financial services grew revenue 2.2% to R385m (interest and charges +5.9%, insurance -4.8%), while cellular and mobile revenue grew 20.7% to R358m. Cellular products are now sold through a call centre and 242 store kiosks across the group, with further rollout planned.

Retail sales outside of South Africa, which constitute 7.9% of group sales, declined by 2.2%, partly explained by the performance of Mr Price Apparel (which constitutes 69.7% of non-South African sales) and struggling economies. The group has elected to focus on areas of significant potential and accordingly exited Australia. Likewise, the Mr Price Home Polish test store will be closed in December. Efforts will be channelled into improving the performance of the largest apparel division and maximising several local opportunities. Net asset value per share increased 10.3% to 3 273c from September 2018. Capital expenditure of R231m was incurred, primarily in store development activities. Inventory levels were up 14.9%, with markdown units as a percentage of total units lower than the prior period and a good stock freshness ratio. The debtors book remains well managed, with a retail net bad debt to book ratio of 7.2% matched by an impairment provision at the same level. The group has concluded its internal investigation into the suspected non-compliance with its Code of Conduct as advised in the SENS announcements of 12 September and 19 September 2019.

The group’s previously expressed views on materiality have not changed, and appropriate action has been taken in support of its zero-tolerance policy to such matters. A short-term recovery in the consumer environment seems unlikely. Meaningful GDP growth will only return when broad-based structural economic reforms gain traction. The group is focused on winning market share, particularly in Mr Price Apparel. A shift in momentum was seen in the last two months of H1 FY2020, with the group’s retail sales growth outperforming Type D retailers in both August and September 2019. Whilst trade has been challenging, the energy across the business is high and the team is clear on what is needed to return the group to its winning ways

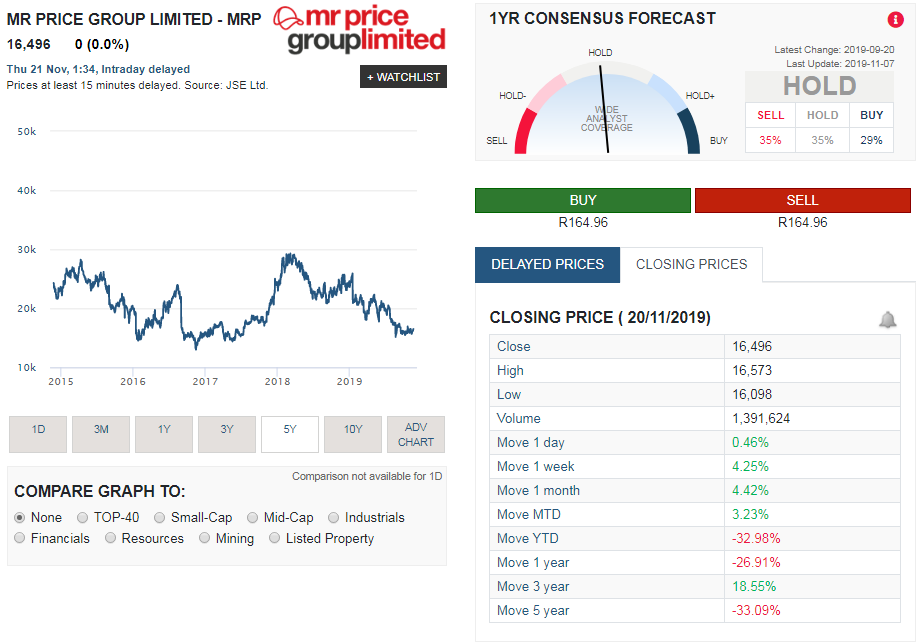

Mr Price Share Price history

The image below, taken from Sharenet shows the MRP share price history for the last 5 years, and as the chart shows, MRP has been moving largely sideways and down over the period in question. This is largely driven by a weak economic and operating environment that they operate in. And as consumers struggle more and more they tend to hold back on their spending, especially on goods such as clothing and home accessories.

MRP share price history

The summary below shows the share price performance of the group over different periods of time:

- 1 week: 4.25%

- 1 month: 4.42%

- Year to date (YTD): -32.98%

- 1 year: -26.91%

- 3 years: 18.55%

- 5 years: -33.09%

Mr Price (MRP) share valuation as at 21 November 2019

Based on Mr Price's latest interim financial results released our valuation model provides a full value price for Mr Price shares at R180.70, this is down from our Mr Price stock valuation in June 2019, and this is largely due to the group's deteriorating financial position as shown by a 9.6% decline in their headline earnings per share compared to the same period of the previous year. Below a summary of our June 219 share valuation of Mr Price Group (MRP)

Mr Price (MRP) share valuation as at June 2019

So based on MRP's latest financial results, is it a good time to buy there shares? Or did the massive jump in the share price on Friday take away any potential gains for investors looking to buy undervalued quality stocks? While the numbers reported were good, one has to remember it is coming off a lower base, and that the South African economy is growing very slowly and the competition in the sectors they operate in is very tough. The group's inventories increased sharply, possibly due to new stock coming in before change of seasons, or the more sinister answer could be the group is struggling to move stock so inventories are building up?

Based on their current financial results, their profit margins, their revenue growth, their strong balance sheet and cash generating capacity we value the group's shares at R203.60 a share. So at their current price we feel that Mr Price shares are close to being fully valued

Based on their current financial results, their profit margins, their revenue growth, their strong balance sheet and cash generating capacity we value the group's shares at R203.60 a share. So at their current price we feel that Mr Price shares are close to being fully valued