|

Related Topics |

|

We take a look at the quarterly results of Albemarle the chemicals firm listed on the New York Stock Exchange (NYSE) for the period ending September 2018.

Readers might be wondering why we covering US listed stocks? Well South Africans can invest offshore so we have decided to broaden our scope beyond just South African listed firms |

|

About Albemarle

With a history that extends back to 1887, today’s Albemarle is a leading global producer of catalyst solutions and performance chemicals. Our products are used as additives to, or intermediates for, a wide range of products manufactured by pharmaceutical companies, cleaning product manufacturers, water treatment companies, agricultural companies, electronics goods manufacturers, refineries, and paper and photographic companies. We operate on a global scale, serving customers around the world.

Lithium:

Albemarle is the industry leader in lithium and lithium derivatives, one of the highest growth markets in the specialty chemicals industry. Our unique natural resource position, derivatization capabilities and technology leadership allow Albemarle to execute an aggressive growth strategy for this business. We control a diverse and high quality network of natural resources that are geographically situated in low-risk environments with good infrastructure. The scale of our operations promotes attractive economies of scale. We maintain the strongest vertical position in the industry, from raw material extraction to specialty product manufacturing. We possess a deep and broad process technology expertise that has grown in scale with our recent acquisitions. Our unmatched global footprint and extensive production capacity, that is currently expanding, allow us to be the most reliable and sustainable supply network in the industry. We have the lowest cost position for lithium carbonate and lithium hydroxide, while providing the highest quality products. We can sustain the Albemarle advantage because our unique position is difficult to replicate and has taken a century to establish.

Catalysts:

Growing global demand for fuel and advanced materials —and the requirement that tomorrow’s products be created in an efficient, yet environmentally responsible manner—plays directly to our chemistry expertise and innovative technologies. Albemarle provides top-performance catalysts, technologies and related services to the refining, petrochemical and electronics industries. Through a variety of applications, our global network of industry-leading professionals can tackle the toughest challenges. Together with our partners, we continue to drive innovation and deliver value to our customers through our two primary divisions: Heavy Oil Upgrading (FCC catalysts) and Clean Fuel Technologies (HPC catalysts).

Albemarle also combines a robust portfolio of polyolefin catalysts, catalyst components, and synthesis tools for the polymers, electronics, agrochemicals, pharmaceuticals, and other specialty markets. We also offer a line of curative chain extenders and cure promoters to further broaden the reach of our diversified portfolio.

Bromine specialities:

Albemarle’s bromine chemistry plays a leading role in providing performance products for fire safety, oilfield drilling, pharmaceutical manufacturing, high-tech cleaning, water treatment and food safety for a growing world. Our leading portfolio of brominated fire safety solutions used in consumer electronics, construction and automotive applications help keep people and property safe. We are continually developing technologies that will help keep our environment clean by reducing mercury emissions. For decades, our people have combined innovation and speed-to-market to deliver custom chemistry solutions to the world’s leading producers of pharmaceuticals, agricultural products and electronic chemicals.

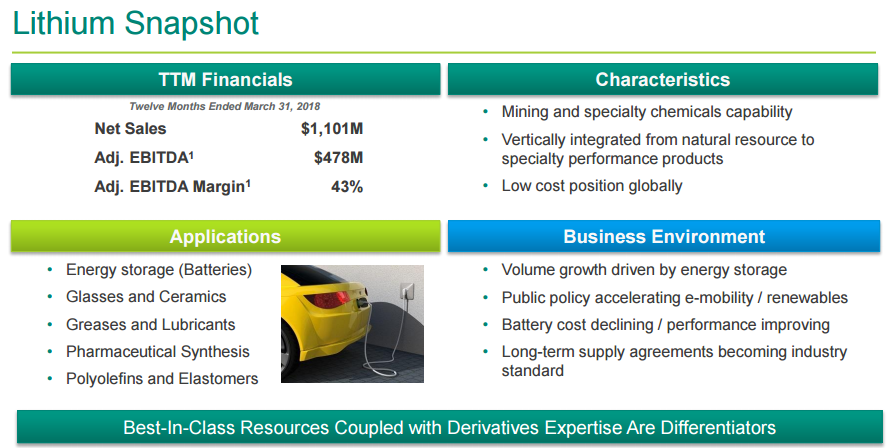

The image below shows one of Albemarle's core focuses right now, which is Lithium, largely due to its application in electric vehicle batteries. So of you bullish on the prospects of E-vehicles, you should be bullish on Albemarles prospects.

Lithium:

Albemarle is the industry leader in lithium and lithium derivatives, one of the highest growth markets in the specialty chemicals industry. Our unique natural resource position, derivatization capabilities and technology leadership allow Albemarle to execute an aggressive growth strategy for this business. We control a diverse and high quality network of natural resources that are geographically situated in low-risk environments with good infrastructure. The scale of our operations promotes attractive economies of scale. We maintain the strongest vertical position in the industry, from raw material extraction to specialty product manufacturing. We possess a deep and broad process technology expertise that has grown in scale with our recent acquisitions. Our unmatched global footprint and extensive production capacity, that is currently expanding, allow us to be the most reliable and sustainable supply network in the industry. We have the lowest cost position for lithium carbonate and lithium hydroxide, while providing the highest quality products. We can sustain the Albemarle advantage because our unique position is difficult to replicate and has taken a century to establish.

Catalysts:

Growing global demand for fuel and advanced materials —and the requirement that tomorrow’s products be created in an efficient, yet environmentally responsible manner—plays directly to our chemistry expertise and innovative technologies. Albemarle provides top-performance catalysts, technologies and related services to the refining, petrochemical and electronics industries. Through a variety of applications, our global network of industry-leading professionals can tackle the toughest challenges. Together with our partners, we continue to drive innovation and deliver value to our customers through our two primary divisions: Heavy Oil Upgrading (FCC catalysts) and Clean Fuel Technologies (HPC catalysts).

Albemarle also combines a robust portfolio of polyolefin catalysts, catalyst components, and synthesis tools for the polymers, electronics, agrochemicals, pharmaceuticals, and other specialty markets. We also offer a line of curative chain extenders and cure promoters to further broaden the reach of our diversified portfolio.

Bromine specialities:

Albemarle’s bromine chemistry plays a leading role in providing performance products for fire safety, oilfield drilling, pharmaceutical manufacturing, high-tech cleaning, water treatment and food safety for a growing world. Our leading portfolio of brominated fire safety solutions used in consumer electronics, construction and automotive applications help keep people and property safe. We are continually developing technologies that will help keep our environment clean by reducing mercury emissions. For decades, our people have combined innovation and speed-to-market to deliver custom chemistry solutions to the world’s leading producers of pharmaceuticals, agricultural products and electronic chemicals.

The image below shows one of Albemarle's core focuses right now, which is Lithium, largely due to its application in electric vehicle batteries. So of you bullish on the prospects of E-vehicles, you should be bullish on Albemarles prospects.

Fine chemistry services:

Albemarle provides custom synthesis manufacturing of APIs, agricultural actives and advanced intermediates for customers in the API pharmaceutical, agrichemicals and specialty chemicals industries. With world-class facilities, exceptional process development and scale-up capabilities, and 40 years of exemplary customer service, we are the perfect production partner for your custom project. We offer a complete range of manufacturing services backed by highly skilled R&D teams to assist with synthesis route selection, process development and analytical support. At every point, we offer seamless service and hands-on assistance. Albemarle implements cGMPs at our API manufacturing facility in South Haven, MI and offers ISO and FIFRA manufacturing services at Tyrone PA. Albemarle also custom manufactures high volume products at its Pasadena TX plant and R&D and scale-up activities at its Process Development Center in Baton Rouge, LA.

Albemarle provides custom synthesis manufacturing of APIs, agricultural actives and advanced intermediates for customers in the API pharmaceutical, agrichemicals and specialty chemicals industries. With world-class facilities, exceptional process development and scale-up capabilities, and 40 years of exemplary customer service, we are the perfect production partner for your custom project. We offer a complete range of manufacturing services backed by highly skilled R&D teams to assist with synthesis route selection, process development and analytical support. At every point, we offer seamless service and hands-on assistance. Albemarle implements cGMPs at our API manufacturing facility in South Haven, MI and offers ISO and FIFRA manufacturing services at Tyrone PA. Albemarle also custom manufactures high volume products at its Pasadena TX plant and R&D and scale-up activities at its Process Development Center in Baton Rouge, LA.

So to the numbers we go

- Net sales $777,748,000 up 3% from $754,866,000 for last year for the same time period

- Adjusted EBITDA $235 082 000 up 12.2% from $209,383,000 for last year for the same time period

- Adjusted earnings per share $1.31 up 21.3% from $1.08 last year for the same time period (This puts Albemarle on a forward PE ratio of 20.4, which is relatively steep. But we suspect the market is pricing in substantial gains in the Lithium side of the business in future.

So any comments or guidance from management on the results?

The following extracts were taken from their quarterly results as published on 7 November 2018

Third quarter 2018 earnings were $129.7 million, or $1.20 per diluted share, compared to $118.7 million, or $1.06 per diluted share in the third quarter 2017. The increase in 2018 was primarily driven by earnings growth in our Bromine Specialties and Catalysts reportable segments and lower costs in Corporate, in addition to strong performance in our fine chemistry solutions business. Third quarter 2018 adjusted EBITDA increased by $25.7 million, or 12.3%, compared to the prior year. Third quarter 2018 adjusted net income was $141.5 million, or $1.31 per diluted share, compared to $120.6 million, or $1.08 per diluted share, for third quarter 2017, an increase of 21.3%.

See Non-GAAP Reconciliations for further details. The Company reported net sales of $777.7 million in third quarter 2018, up 3.0% from net sales of $754.9 million in the third quarter of 2017, driven by the impact of sales pricing in each of our reportable segments and increased sales volumes in our Bromine Specialties and Catalysts segments, partially offset by lower lithium volumes due to unexpected shut downs at three of our manufacturing sites and the impact of the divestiture of the polyolefin catalysts and components portion of the Performance Catalyst Solutions ("PCS") business ("Polyolefin Catalysts Divestiture").

For the nine months ended September 30, 2018, earnings were $564.0 million, or $5.11 per diluted share, compared to $273.2 million, or $2.43 per diluted share for the nine months ended September 30, 2017. The increase in 2018 was primarily driven by the $1.60 per diluted share gain on sale of the Polyolefin Catalysts Divestiture, earnings growth in each of our reportable segments, and a loss on early extinguishment of debt of $0.34 per diluted share recorded in 2017. For the nine months ended September 30, 2018, adjusted EBITDA increased by $102.7 million, or 16.0%, compared to the same period in 2017. For the nine months ended September 30, 2018, adjusted net income was $436.6 million, or $3.96 per diluted share, compared to $366.0 million, or $3.26 per diluted share, for the same period 2017, an increase of 21.5%. See Non-GAAP Reconciliations for further details. The Company reported net sales for the nine months ended September 30, 2018 of $2.45 billion, up from net sales of $2.21 billion for the nine months ended September 30, 2017, driven by the favorable impact of higher sales volumes, favorable pricing and currency exchange impacts in each of our reportable segments, partially offset by the impact of the Polyolefin Catalysts Divestiture.

On April 3, 2018, we closed the Polyolefin Catalysts Divestiture to W.R. Grace & Co. for net cash proceeds of approximately $413.5 million and recorded an after-tax gain of $176.7 million related to the sale of this business. The transaction includes Albemarle's Product Development Center located in Baton Rouge, Louisiana, and operations at the Yeosu, South Korea site. The transaction does not include the organometallics or curatives portion of the PCS business. The assets and liabilities of this business are included in Assets held for sale and Liabilities held for sale in the consolidated balance sheets as of December 31, 2017.

Third quarter 2018 earnings were $129.7 million, or $1.20 per diluted share, compared to $118.7 million, or $1.06 per diluted share in the third quarter 2017. The increase in 2018 was primarily driven by earnings growth in our Bromine Specialties and Catalysts reportable segments and lower costs in Corporate, in addition to strong performance in our fine chemistry solutions business. Third quarter 2018 adjusted EBITDA increased by $25.7 million, or 12.3%, compared to the prior year. Third quarter 2018 adjusted net income was $141.5 million, or $1.31 per diluted share, compared to $120.6 million, or $1.08 per diluted share, for third quarter 2017, an increase of 21.3%.

See Non-GAAP Reconciliations for further details. The Company reported net sales of $777.7 million in third quarter 2018, up 3.0% from net sales of $754.9 million in the third quarter of 2017, driven by the impact of sales pricing in each of our reportable segments and increased sales volumes in our Bromine Specialties and Catalysts segments, partially offset by lower lithium volumes due to unexpected shut downs at three of our manufacturing sites and the impact of the divestiture of the polyolefin catalysts and components portion of the Performance Catalyst Solutions ("PCS") business ("Polyolefin Catalysts Divestiture").

For the nine months ended September 30, 2018, earnings were $564.0 million, or $5.11 per diluted share, compared to $273.2 million, or $2.43 per diluted share for the nine months ended September 30, 2017. The increase in 2018 was primarily driven by the $1.60 per diluted share gain on sale of the Polyolefin Catalysts Divestiture, earnings growth in each of our reportable segments, and a loss on early extinguishment of debt of $0.34 per diluted share recorded in 2017. For the nine months ended September 30, 2018, adjusted EBITDA increased by $102.7 million, or 16.0%, compared to the same period in 2017. For the nine months ended September 30, 2018, adjusted net income was $436.6 million, or $3.96 per diluted share, compared to $366.0 million, or $3.26 per diluted share, for the same period 2017, an increase of 21.5%. See Non-GAAP Reconciliations for further details. The Company reported net sales for the nine months ended September 30, 2018 of $2.45 billion, up from net sales of $2.21 billion for the nine months ended September 30, 2017, driven by the favorable impact of higher sales volumes, favorable pricing and currency exchange impacts in each of our reportable segments, partially offset by the impact of the Polyolefin Catalysts Divestiture.

On April 3, 2018, we closed the Polyolefin Catalysts Divestiture to W.R. Grace & Co. for net cash proceeds of approximately $413.5 million and recorded an after-tax gain of $176.7 million related to the sale of this business. The transaction includes Albemarle's Product Development Center located in Baton Rouge, Louisiana, and operations at the Yeosu, South Korea site. The transaction does not include the organometallics or curatives portion of the PCS business. The assets and liabilities of this business are included in Assets held for sale and Liabilities held for sale in the consolidated balance sheets as of December 31, 2017.

During 2018, the PCS product category merged with the Refining Solutions reportable segment to form a global business focused on catalysts. As a result, our three reportable segments include: (1) Lithium; (2) Bromine Specialties; and (3) Catalysts. For comparison purposes, prior year periods have been reclassified to conform to the current presentation.

Lithium reported net sales of $270.9 million in the third quarter of 2018, an increase of 0.6% from third quarter 2017 net sales of $269.2 million. The $1.7 million increase in net sales as compared to prior year was primarily due to approximately $16.2 million in pricing increases, partially offset by lower sales volumes due to temporary operational issues. Adjusted EBITDA for Lithium was $113.6 million, an increase of 0.6% from third quarter 2017 results of $112.9 million. The $0.7 million increase in adjusted EBITDA as compared to the prior year was primarily due to favorable pricing impacts, partially offset by higher royalty payments and decreased sales volumes.

Bromine Specialties reported net sales of $232.6 million in the third quarter of 2018, an increase of 9.2% from third quarter 2017 net sales of $212.9 million. The $19.7 million increase in net sales as compared to the prior year was primarily due to favorable pricing impacts and increased sales volumes. Adjusted EBITDA for Bromine Specialties was $78.6 million, an increase of 22.9% from third quarter 2017 results of $63.9 million. The $14.6 million increase in adjusted EBITDA as compared to the prior year was primarily due to favorable pricing impacts and increased sales volumes, partially offset by higher raw material pricing.

Catalysts reported net sales of $251.1 million in the third quarter of 2018, an increase of 2.7% from net sales of $244.6 million in the third quarter of 2017. The $6.5 million increase in net sales as compared to the prior year was primarily due to increased sales volume and favorable pricing impacts, which more than offset the $27.0 million impact of the Polyolefin Catalysts Divestiture. Adjusted EBITDA for Catalysts was $62.6 million in the third quarter of 2018, an increase of 3.7% from third quarter 2017 results of $60.4 million. The $2.2 million increase in adjusted EBITDA as compared to the prior year was primarily due to increased sales volumes and favorable pricing, partially offset by higher material costs and $1.9 million of unfavorable currency exchange impacts. Additionally, the impact of the Polyolefin Catalysts Divestiture of $10.5 million was more than offset by the $10.9 million year over year impact of Hurricane Harvey, which affected the Company in the third quarter of 2017. This includes a partial insurance claim reimbursement of $2.2 million received in the third quarter of 2018. All Other net sales were $23.1 million in the third quarter of 2018, a decrease of 17.7% from net sales of $28.0 million in the third quarter of 2017. The $5.0 million decrease in net sales as compared to the prior year was primarily due to decreased sales volumes and unfavorable pricing impacts in our fine chemistry services business.

The improvement in Corporate adjusted EBITDA was primarily due to lower selling, general and administrative spend, partially offset by $3.5 million of unfavorable currency exchange impacts. Income Taxes In December 2017, the Tax Cuts and Jobs Act ("TCJA") was enacted, requiring companies, among other things, to pay a one-time transition tax on earnings of certain foreign subsidiaries that were previously tax deferred and reducing the U.S. federal corporate income tax rate from 35% to 21%.

Our effective income tax rates for the nine months ended September 30, 2018 and 2017 were 20.1% and 17.6%, respectively, and our adjusted effective income tax rates for the nine months ended September 30, 2018 and 2017 were 22.2% and 19.5%, respectively.

Cash Flow

Our cash from operations was approximately $376.9 million for the nine months ended September 30, 2018, an increase of $302.1 million versus the same period in 2017, primarily due to changes in working capital, including the payment of approximately $255 million in taxes related to the sale of the Chemetall Surface Treatment business in 2017, as well as increased earnings in each of our reportable segments and increased dividends received from unconsolidated investments in 2018.

Capital expenditures were $471.7 million as compared to $187.5 million in the first nine months of 2017, with the increase driven largely by expansion investment in our Lithium business. We had $641.2 million in cash and cash equivalents at September 30, 2018, as compared to $1.14 billion at December 31, 2017. During the first nine months of 2018, cash on hand, cash provided by operations and net proceeds from divestitures funded $135.8 million of commercial paper note repayments, net of borrowings, $471.7 million of capital expenditures for plant, machinery and equipment, and mining resource development, dividends to shareholders of $108.9 million and $500.0 million of accelerated share repurchase programs.

Lithium reported net sales of $270.9 million in the third quarter of 2018, an increase of 0.6% from third quarter 2017 net sales of $269.2 million. The $1.7 million increase in net sales as compared to prior year was primarily due to approximately $16.2 million in pricing increases, partially offset by lower sales volumes due to temporary operational issues. Adjusted EBITDA for Lithium was $113.6 million, an increase of 0.6% from third quarter 2017 results of $112.9 million. The $0.7 million increase in adjusted EBITDA as compared to the prior year was primarily due to favorable pricing impacts, partially offset by higher royalty payments and decreased sales volumes.

Bromine Specialties reported net sales of $232.6 million in the third quarter of 2018, an increase of 9.2% from third quarter 2017 net sales of $212.9 million. The $19.7 million increase in net sales as compared to the prior year was primarily due to favorable pricing impacts and increased sales volumes. Adjusted EBITDA for Bromine Specialties was $78.6 million, an increase of 22.9% from third quarter 2017 results of $63.9 million. The $14.6 million increase in adjusted EBITDA as compared to the prior year was primarily due to favorable pricing impacts and increased sales volumes, partially offset by higher raw material pricing.

Catalysts reported net sales of $251.1 million in the third quarter of 2018, an increase of 2.7% from net sales of $244.6 million in the third quarter of 2017. The $6.5 million increase in net sales as compared to the prior year was primarily due to increased sales volume and favorable pricing impacts, which more than offset the $27.0 million impact of the Polyolefin Catalysts Divestiture. Adjusted EBITDA for Catalysts was $62.6 million in the third quarter of 2018, an increase of 3.7% from third quarter 2017 results of $60.4 million. The $2.2 million increase in adjusted EBITDA as compared to the prior year was primarily due to increased sales volumes and favorable pricing, partially offset by higher material costs and $1.9 million of unfavorable currency exchange impacts. Additionally, the impact of the Polyolefin Catalysts Divestiture of $10.5 million was more than offset by the $10.9 million year over year impact of Hurricane Harvey, which affected the Company in the third quarter of 2017. This includes a partial insurance claim reimbursement of $2.2 million received in the third quarter of 2018. All Other net sales were $23.1 million in the third quarter of 2018, a decrease of 17.7% from net sales of $28.0 million in the third quarter of 2017. The $5.0 million decrease in net sales as compared to the prior year was primarily due to decreased sales volumes and unfavorable pricing impacts in our fine chemistry services business.

The improvement in Corporate adjusted EBITDA was primarily due to lower selling, general and administrative spend, partially offset by $3.5 million of unfavorable currency exchange impacts. Income Taxes In December 2017, the Tax Cuts and Jobs Act ("TCJA") was enacted, requiring companies, among other things, to pay a one-time transition tax on earnings of certain foreign subsidiaries that were previously tax deferred and reducing the U.S. federal corporate income tax rate from 35% to 21%.

Our effective income tax rates for the nine months ended September 30, 2018 and 2017 were 20.1% and 17.6%, respectively, and our adjusted effective income tax rates for the nine months ended September 30, 2018 and 2017 were 22.2% and 19.5%, respectively.

Cash Flow

Our cash from operations was approximately $376.9 million for the nine months ended September 30, 2018, an increase of $302.1 million versus the same period in 2017, primarily due to changes in working capital, including the payment of approximately $255 million in taxes related to the sale of the Chemetall Surface Treatment business in 2017, as well as increased earnings in each of our reportable segments and increased dividends received from unconsolidated investments in 2018.

Capital expenditures were $471.7 million as compared to $187.5 million in the first nine months of 2017, with the increase driven largely by expansion investment in our Lithium business. We had $641.2 million in cash and cash equivalents at September 30, 2018, as compared to $1.14 billion at December 31, 2017. During the first nine months of 2018, cash on hand, cash provided by operations and net proceeds from divestitures funded $135.8 million of commercial paper note repayments, net of borrowings, $471.7 million of capital expenditures for plant, machinery and equipment, and mining resource development, dividends to shareholders of $108.9 million and $500.0 million of accelerated share repurchase programs.

So should you buy their shares?

If you are optimistic about products such as Lithium and the potential growth it will experience due ti increased demand for it due to more electric vehicles hitting the road, then yes they will make a good share to hold. But remember a lot of the expected growth in Lithium is already baked into their share price. Their current cash and equivalents of $640million equates to about $6 a share, so 5.6% of the share price is made up by cash on their balance sheet. Net income generated was sitting at $593million for the 9 months ended September (which equates to roughly $7.33 a share). So strong cash generation from the company.

We are worried about the steep PE ratio, lack of quarterly dividend being paid to reward long term shareholders and the fact that with increased demand for Lithium via e-vehicles, more businesses will look to enter the market to get their slice of the pie. And this could lead to stronger competition for the group which could affect margins. We think its a good stock to hold, if it can be acquired at a PE ratio closer to 15 range. Or basically look to buy it at closer to $75 range.

We are worried about the steep PE ratio, lack of quarterly dividend being paid to reward long term shareholders and the fact that with increased demand for Lithium via e-vehicles, more businesses will look to enter the market to get their slice of the pie. And this could lead to stronger competition for the group which could affect margins. We think its a good stock to hold, if it can be acquired at a PE ratio closer to 15 range. Or basically look to buy it at closer to $75 range.